Dividend Powerhouses with 3%+ yields can be appealing when inflation, interest rates and growth signals are pulling in different directions. With central banks weighing mixed price data and energy and food costs still volatile, many investors are looking for income streams that do not rely solely on fast economic growth. This Dividend Powerhouses screener focuses on companies paying more than a 5% dividend yield that appears covered, growing and relatively stable. In this article, you will see three of the strongest stocks from the screener and how they might fit into a long term income-focused portfolio.

CSL (ASX:CSL)

Overview: CSL is a Melbourne based biopharmaceutical company that turns human plasma into therapies for serious immune, blood and kidney conditions, and also supplies governments with influenza vaccines and treatments for iron deficiency and kidney disease through its CSL Behring, CSL Seqirus and CSL Vifor segments.

Operations: CSL generates most of its revenue from CSL Behring at about US$10.9b, with CSL Vifor at around US$2.4b and CSL Seqirus at roughly US$2.2b. Its largest markets are the United States at about US$7.3b in revenue and the Rest of World at roughly US$4.6b.

Market Cap: A$55.7b

CSL stands out in a dividend focused shortlist because it combines an essential plasma and vaccine business with a 3.58% yield, even as current earnings and margins are under pressure from one off restructuring costs and a large recent loss. The company’s extensive plasma collection network and gene therapy pipeline support interest in its long term earnings power, but funding those assets has left CSL with high debt and a profit margin currently at 9.1%. Leadership changes across CSL Behring and CSL Vifor, plus guidance for a modest revenue decline in FY2026, add execution risk. For income investors, the key question is whether cash flows and future earnings growth can comfortably support that dividend as the restructuring plays out.

CSL’s 3.58% yield, high debt and restructuring costs suggest the real story is in its resilience. Get the full picture with the 2 key rewards and 4 important warning signs

Evolution Mining (ASX:EVN)

Overview: Evolution Mining is an Australian based gold producer that explores for, develops and operates gold and gold copper mines in Australia and Canada, and sells gold as well as gold copper concentrates, with some exposure to silver.

Operations: Evolution Mining generates most of its revenue from Cowal at about A$1.7b and Ernest Henry at roughly A$1.1b, with additional contributions from Mungari at around A$780m, Red Lake at about A$670m, Northparkes at roughly A$580m, and smaller inputs from Corporate and Mt Rawdon.

Market Cap: A$25.5b

Evolution Mining appears in a dividend focused shortlist because it combines a high margin gold portfolio, Return on Equity around 23.6% and copper exposure that can help cushion swings in gold prices. Earnings growth has been strong compared with both its own history and the broader Metals & Mining industry, while revenue growth has been more modest and the dividend track record has been unstable, which matters if you rely on predictable income. The Nevada North Lithium joint venture adds another commodity angle that could influence future cash flows but also brings project execution risk. For income investors, the balance between solid profitability, higher risk external funding and an uneven dividend history may make Evolution Mining a candidate for further research.

Evolution Mining’s high margin gold assets and 23.6% Return on Equity hint that the real story is how efficiently those mines are working for shareholders, but the twist shows up in the analysis report for Evolution Mining

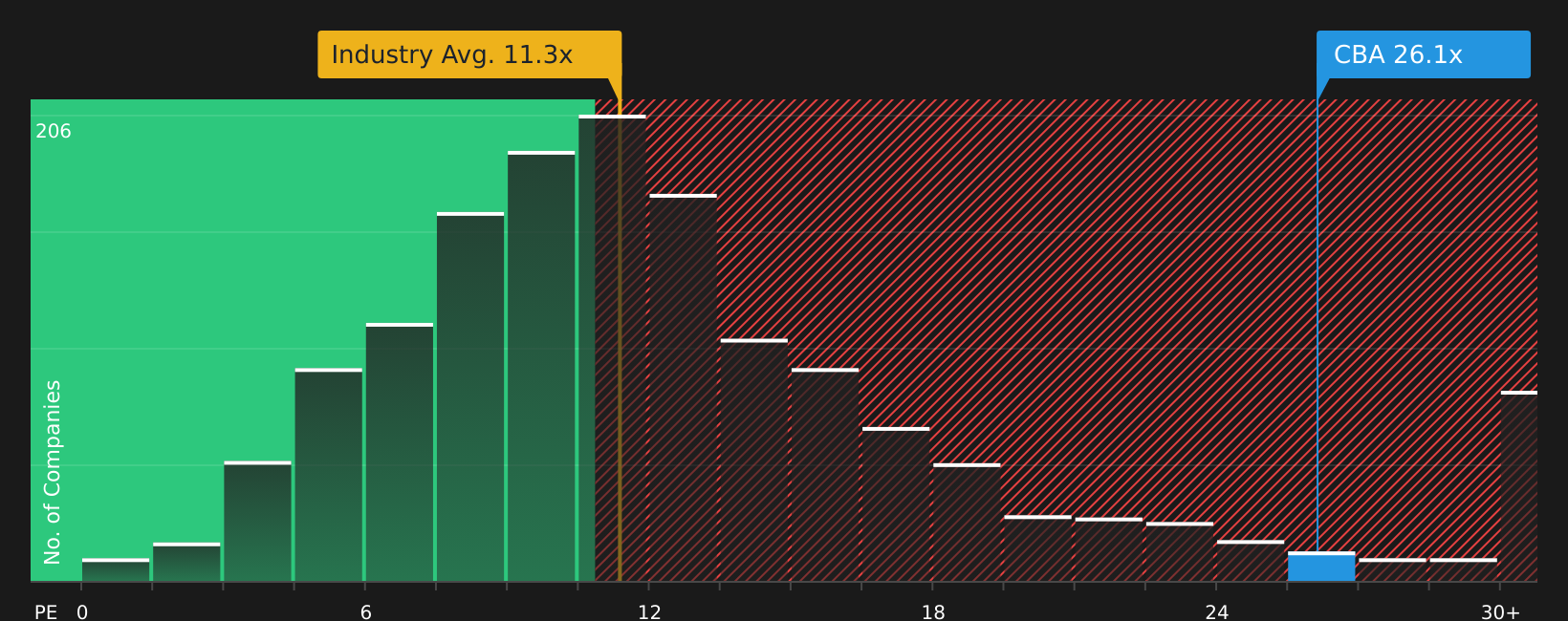

Commonwealth Bank of Australia (ASX:CBA)

Overview: Commonwealth Bank of Australia is a Sydney based bank that offers everyday and business banking, home loans, credit cards, deposits and wealth solutions across Australia, New Zealand and overseas, plus a wide range of insurance products and access to capital markets and trading services.

Operations: Commonwealth Bank of Australia generates most of its revenue from Retail Banking Services including Bankwest at about A$13.1b and Business Banking at roughly A$9.3b, with additional contributions from New Zealand at around A$3.0b and Institutional Banking and Markets at about A$2.9b.

Market Cap: A$271.6b

Income focused investors may be drawn to Commonwealth Bank of Australia because it combines high quality earnings, a 3%+ yield and a long established franchise that still reports positive earnings growth and net margins around 36.5%. This is occurring even as competition in digital banking and payments, plus heavy technology and AI investment, put pressure on costs and pricing. The bank’s conservative balance sheet, strong customer loyalty and push into AI talent indicate it is working to protect those profit streams. At the same time, the stock trades on a rich P/E compared with many global peers and carries an unstable dividend track record and modest growth forecasts. The tension between that premium valuation, its technology spend and future earnings and dividend support is a key consideration for dividend investors.

Commonwealth Bank of Australia’s rich P/E and sturdy margins suggest something in the story is decoupling price from risk, and the full 1 key reward and 2 important warning signs could reveal what many income investors are missing

The three dividend stocks in this article are only a starting point, as the full Dividend Powerhouses (3%+ Yield) screen on Simply Wall St has identified 28 more companies with similarly compelling income and risk narratives through the Dividend Powerhouses (3%+ Yield) screener. Use the platform to identify and analyze the specific catalysts, balance sheet strength and dividend stories that matter most to you so you can focus on the highest conviction opportunities in this income style.

Take Control of Your Investment Journey

If Evolution Mining or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Dividends?

Fresh opportunities can move from quiet to flying fast, and once momentum is obvious, the best entry points are often gone. Check curated ideas that are under the radar for now and consider acting before they become widely followed.

- Target resilient cash generators by reviewing a curated list of solid balance sheet and fundamentals (19 results) that highlights companies built to handle shocks while keeping fundamentals front and center.

- Spot potential breakout income plays through the hand picked 7 dividend fortresses that focuses on companies pairing higher yields with balance sheet strength.

- Chase early momentum in precious metals with a filtered 33 elite gold producer stocks that focuses on producers positioned to benefit if interest returns to gold miners.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment