Why a recent sell call has put JB Hi-Fi (ASX:JBH) back in focus

A recent analyst call from Fairmont Equities, flagging rising interest rates, higher fuel costs and softer consumer discretionary spending as risks, has put JB Hi-Fi (ASX:JBH) back on many investors’ watchlists.

See our latest analysis for JB Hi-Fi.

Despite the recent sell call, JB Hi-Fi’s share price has A$77.87 as the latest close, with a 30-day share price return of 8.08% contrasting with a 19.10% decline year to date and a 21.59% decline in 1-year total shareholder return. The 3 and 5-year total shareholder returns of 92.65% and 117.82% reflect a much stronger longer term picture, suggesting momentum has recently stabilised after earlier weakness.

If this shift in sentiment has you reassessing your watchlist, it can be useful to see which other companies are catching investors’ attention through 4 top founder-led companies

With JB Hi-Fi trading below some analyst targets and showing both recent share price weakness and strong longer term returns, you need to ask: is the stock undervalued here, or is the market already pricing in future growth?

Most Popular Narrative: 12% Overvalued

According to XiaoheGong, the current A$77.87 share price sits above a narrative fair value of A$69.54, which is built on JB Hi-Fi’s role as a mature, cycle driven retailer rather than a high growth stock.

Over the long term, JB Hi-Fi is not a high growth technology company but rather a mature retailer that moves with the consumer cycle. If consumer electronics demand returns toward normal levels, sales volumes would likely recover and operating leverage could lift profits faster than revenue; if demand remains weak, growth would likely stay subdued. The company’s value therefore depends largely on the pace of consumer demand recovery: if spending normalises, the current share price could be supported by earnings recovery; if discretionary demand remains depressed, the share price may face downside pressure.

Curious what sits behind that A$69.54 fair value. The narrative leans on specific revenue growth, margin resilience and a future earnings multiple that may surprise you.

Result: Fair Value of A$69.54 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, that story can quickly change if cost of living pressures keep discretionary budgets tight or if competitor discounting pressures margins more than expected.

Find out about the key risks to this JB Hi-Fi narrative.

Another angle on value: multiples vs fair ratio

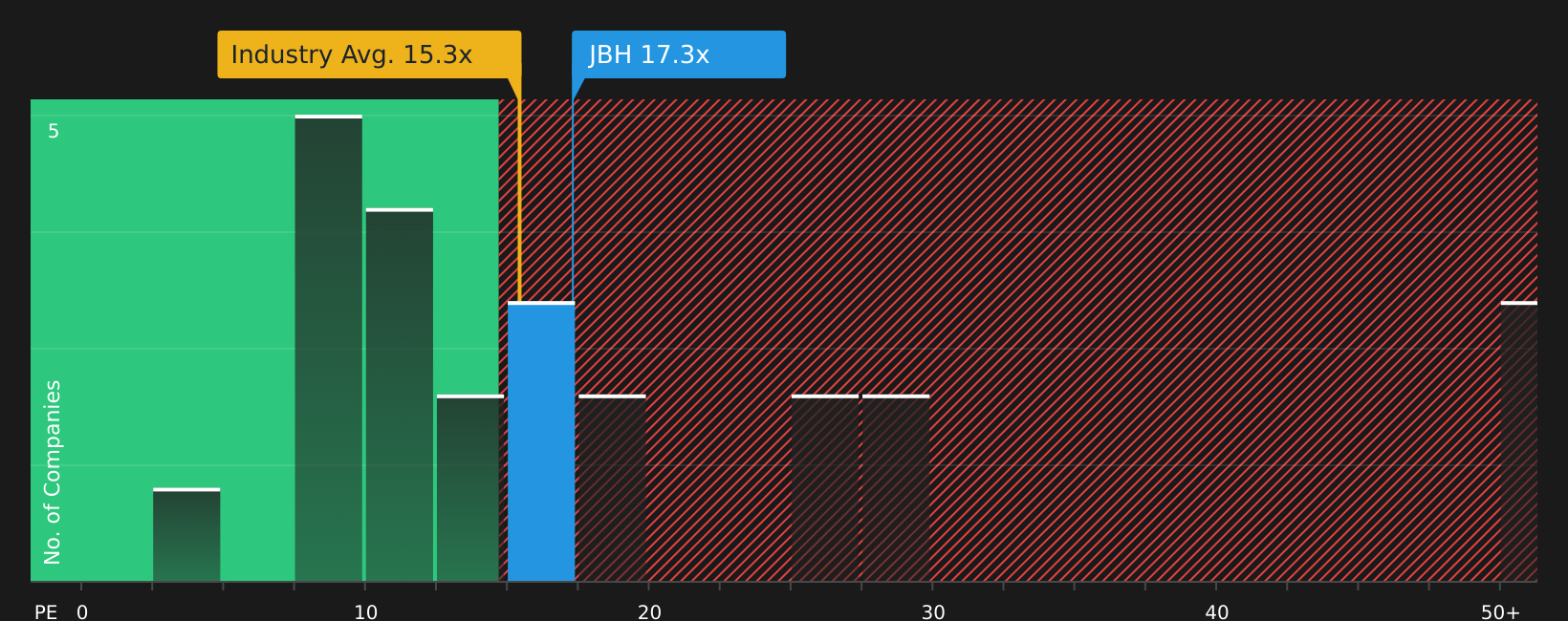

While the narrative pegs fair value at A$69.54, the market is sending mixed signals. JB Hi-Fi trades on a 17.6x P/E, above the Australian Specialty Retail average of 13.7x and the 16.2x fair ratio that the market could move toward, yet below the peer average of 20.3x. This raises the question of whether that represents a safety margin or a potential value trap.

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out JB Hi-Fi for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 8 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

The mix of concern and optimism around JB Hi-Fi is clear. Move quickly, review the data in full and weigh both 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If JB Hi-Fi has sharpened your thinking, do not stop here. Broaden your watchlist now and give yourself more options before the next big move.

- Target potential value opportunities by scanning 8 high quality undervalued stocks that combine quality fundamentals with pricing that may leave room for upside.

- Strengthen your income focus by reviewing 8 dividend fortresses built around companies offering higher yields with payments that may appeal to dividend investors.

- Prioritise resilience by filtering for 6 resilient stocks with low risk scores so your portfolio is not solely exposed to higher volatility stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment