Literature review of corporate digital transformation

Corporate digital transformation and economic outcomes

CDT has become an essential strategy for global enterprises aiming to bolster competitiveness, foster innovation, and enhance operational efficiency. CDT entails a holistic refinement of business processes, operational frameworks, products, and services through the integration of advanced technologies, including cloud computing, big data, artificial intelligence (AI), and the Internet of Things (IoT) (Annarelli et al., 2021; Verhoef et al., 2021; Chen et al., 2023; Babina et al., 2024; Jiang et al., 2025a). As digitalization increasingly becomes the norm for companies navigating the digital economy’s landscape, it has also garnered considerable attention in academic circles. A review of existing literature traces the evolution of the concept of DT, shifting from mere ‘investment in Information and Communication Technology (ICT)’ to broader ‘digitization’ and ultimately to ‘digital transformation’ (Verhoef et al., 2021). ICT is defined as systems utilized for transmitting, storing, processing, displaying, creating, and automating the dissemination of information, typically including technology such as television, landline and mobile phones, radio, satellite systems, and computer software and hardware (Du and Jiang, 2022).

Verhoef et al. (2021) delineate three evolutionary stages of DT: the initial stage focuses on converting analog signals into digital formats, essentially the ICT investment phase; the second stage enhances business processes via digital technologies (digitization); and the third stage involves strategic overhauls of business models and organizational cultures (digital transformation), building on the technological foundations established in the earlier stages. Vial (2019) argues that DT represents the convergence of the tangible and technological realms, profoundly altering the functionality of the tangible and enhancing its characteristics. Baskerville et al. (2020) describe digitization as an outcome of the convergence of digital tools such as 5G mobile networks, sensors, 3D printing, and blockchain, technologies that have emerged from advancements in ICT and that integrate the digital and physical worlds.

DT signifies a pivotal process enabled by digital technology, exerting profound impacts on companies. Empirical studies have validated the positive effects of digitization across various domains, including profitability (Oh et al., 2012; Liu et al., 2023a; Liu et al., 2023b; Peng and Tao, 2022; Babina et al., 2024; Chen and Srinivasan, 2024;), cost management (Du et al., 2024; Li et al., 2024), productivity (Du and Jiang, 2022; Guo et al., 2023), technological innovation (Mikalef et al., 2019; Usai et al., 2021; Radicic and Petkovic, 2023; Rubio-Andrés et al., 2024; Wu and Li, 2024), sustainable performance (Zhou et al., 2023; Shang et al., 2023; Bendig et al., 2023; Xiao et al., 2024), external financing (Sun et al., 2024; Jiang et al., 2025a), and supply chain relationships (Geng et al., 2024; Dubey et al., 2024). This body of research underscores the transformative potential of digital technologies in reshaping corporate landscapes and driving forward economic progress.

Numerous studies have affirmed the advantages of DT, yet the relationship between such transformation and economic outcomes is multifaceted. Babina et al. (2024) utilized recruitment data from American companies to demonstrate that firms making substantial investments in AI technology tend to experience enhanced growth, larger employment scales, and increased corporate value. Similarly, Du et al. (2024) found that innovations rooted in digital technology can increase operational flexibility and reduce cost stickiness. Through a textual analysis of digitization in corporate reporting, Chen and Srinivasan (2024) empirically established a positive correlation between the frequency of digital-related keywords and elevated corporate value levels. Zhou et al. (2023) also employed textual analysis but focused on a sample of Chinese firms, finding significant improvements in environmental public sentiment as a result of company digitization. Jiang et al. (2025a) identified an enhancement in external financing capabilities linked to increased corporate digital awareness, reflected by improved bond credit ratings.

However, the narrative of universally positive outcomes from DT is challenged by some researchers. Oludapo et al. (2024) and Kempeneer and Heylen (2023) argue that DT, while fundamentally an investment activity, can lead to significant resource displacement effects if pursued too rapidly or extensively. Sun et al. (2024) suggest that an accelerated pace of digitization could exacerbate a company’s financial constraints. Furthermore, Usai et al. (2021) analyzed data from companies within the European Union and observed that commonly implemented digital technologies exert a minimal impact on corporate innovation performance. This minimal impact suggests that innovation stems more from creativity and sustained research and development efforts than from mere technological adoption. Excessive reliance on digital technologies might even erode a firm’s long-term innovative capacity, as indicated by Guo et al. (2023), who found that while DT indicators increase a company’s TFP, they may concurrently lower performance metrics.

In conclusion, while DT presents significant benefits, it epitomizes a technological investment that can also encounter the paradox of “too much of a good thing.” As highlighted by Oludapo et al. (2024) and Kempeneer and Heylen (2023), despite its potential advantages, corporate digitization may culminate in “failure,” illustrating the complex dynamics between DT and corporate performance.

Corporate digital transformation and corporate risk

The ambiguous relationship between DT and economic outcomes underscores the necessity of examining the risk effects associated with digitization. Recent studies delve into the complex interplay between corporate digitization and various forms of risk or risk-bearing capacities. Regarding financial risk, research by Chen et al. (2024a) reveals that CDT substantially alleviates firms’ default risk, thereby enhancing financial stability and reducing uncertainties associated with external financing. Concerning market risk, empirical analyses indicate that CDT significantly curtails the risk of stock price crashes (Jiang et al., 2022) and systemic risks (Jiang et al., 2024), particularly by bolstering firms’ capacity to counteract information asymmetry amid market volatility. In the realm of governance risk, Xu et al. (2024) have discovered that the effectiveness of CDT on enterprise risk management is contingent upon the firm’s governance capabilities. Their findings suggest that board-level IT governance exerts a negative moderating influence on the outcomes of CDT, underscoring the necessity of robust governance frameworks to navigate the complexities associated with DT. Luo (2021) examines the governance risks specific to multinational enterprises, highlighting the critical role of geographic diversity and international strategic planning in managing risks related to information security and regulatory challenges, especially in the context of intricate cross-border data flows and global regulatory frameworks. Regarding supply chain risk, Ivanov et al. (2019) developed a framework to analyze how Industry 4.0 technologies mitigate risks associated with supply chain disruptions and their consequent ripple effects. This study accentuates CDT’s vital role in the strategic management of supply chain risks. Additionally, research by Chen et al. (2025) focuses on the spillover effects of delayed digitization within supply chains, noting that such delays can escalate financial risks for suppliers and intensify revenue volatility. This body of work collectively emphasizes the transformative impact of CDT across various dimensions of corporate risk, advocating for strategic implementations to harness its full potential while mitigating associated vulnerabilities.

Some research discusses the risk-bearing capacity of companies following digitization (Liu and Liu, 2024; Luo et al., 2024; Wu and Wang, 2024; Feng and Yu, 2025). For instance, Luo et al. (2024) observed in A-share listed companies that CDT correlates with an increase in firms’ propensity for risk-taking, potentially due to enhanced capabilities to identify and exploit new market opportunities. This suggests that CDT equips firms to more effectively adapt to market shifts and discover novel business prospects. Other research employing textual indicators of digitization also confirms that CDT raises risk-taking levels.

To summarize, significant advancements have been made in examining the potential linkages between DT and corporate risk, characterized by uncertainties in economic output. However, several areas remain underexplored. First, while there is considerable discussion on firms’ increased propensity to assume risk post-digitization, there is limited research addressing operational risks and the valuation of real options following digitalization. Second, while existing studies extensively assess the impact of digitalization on key financial metrics, there is a notable deficiency in the exploration of non-operational financial conditions. Moreover, as sustainable growth achieves global consensus and ESG performance becomes critically important for securing stakeholder trust (Zhou et al., 2023; Singhania and Gupta, 2024), these aspects demand further scholarly attention. Third, although the literature frequently underscores the advantages of corporate digitalization, it is equally important to acknowledge that DT can fail, as noted by Oludapo et al. (2024) and Kempeneer and Heylen (2023). A too-rapid digital transition can necessitate significant investments in new technologies and infrastructures, imposing considerable strains on firms. Fourth, the prevalent use of textual indicators to gauge digitalization levels within firms, while indicative of executive awareness toward a digital economy, fails to capture the actual economic impact. This paper proposes a novel digitalization index based on asset conditions to analyze its influence on operational risks, substantiating the findings via both financial and non-financial channels, and documents instances of digitalization failures.

Determinants of corporate digital transformation

In Chinese mainland, CDT is driven by distinct motivations and contextual factors. Research indicates that the Chinese government has been a pivotal force in promoting CDT through both policy support and the enhancement of infrastructure (Wang et al., 2023a; Wang et al., 2023b; Wu et al., 2023; Zhao et al., 2024; Zhu et al., 2023). For instance, Wu et al. (2023) analyze the impact of “Broadband China” initiative on CDT in Chinese mainland, and Wang et al. (2023b) investigate the influence of governmental digital initiatives on corporate digital innovation. Despite these advancements facilitated by state support, Chinese enterprises continue to encounter unique challenges such as the funding requirements for technological innovation and shortages of skilled talent (Bai et al., 2024).

Moreover, the existing literature has seldom addressed the heterogeneous impacts of CDT across diverse enterprise types. Factors like firm size, capital intensity, and governance structure contribute to varying outcomes in CDT implementation. For example, Jia et al. (2024) observe that small enterprises, constrained by limited resources, often struggle more with DT compared to larger organizations, which typically possess more technological resources and capital for such endeavors. Capital-intensive enterprises, while facing heightened financial pressures and risks during transformation, stand to gain substantial efficiency improvements and reductions in carbon emissions due to their high energy consumption and resource usage. Over time, these benefits can translate into significant cost savings and competitive advantages (Shang et al., 2023). Additionally, enterprises with centralized governance structures, such as state-owned enterprises or those controlled by a few shareholders, may experience slower decision-making processes, particularly when cross-departmental collaboration is required. This can lead to bureaucratic impediments and internal conflicts, thus undermining the efficiency and effectiveness of CDT (Zhang, 2024; Zhu, 2024).

The literature reviewed underscores that factors like intellectual property, market demand, and robust cash flow are critical in determining a company’s propensity to undertake DT. In light of these insights, our study will conduct heterogeneous analyses from multiple perspectives to explore protective measures for digitalization initiatives and strategies to enhance digitalization efforts effectively.

Theoretical considerations and research hypotheses

The characteristic of corporate digital transformation

Utilizing advanced technologies, CDT seeks to overhaul production processes, business paradigms, and organizational ethos. This transformative initiative endows firms with four pivotal attributes:

Dataization

Traditional business operations, previously compartmentalized, now generate extensive datasets. Modern intelligent hardware and software systems streamline the aggregation and visualization of this data, thus dismantling intra-organizational information silos.

Intelligence

The integration of digital technologies fosters intelligent operations across manufacturing, decision-making, and management spheres. The deployment of industrial robots, IoT devices, and AI algorithms advances automation and enhances monitoring capabilities, significantly reducing operational errors and optimizing resource allocation. For instance, Tencent leverages big data analytics to fortify internal controls and diminish fraud risks.

Networking

Transforming conventional supply chain frameworks into dynamic, network-based models facilitates direct engagement with consumers and supports the customization of services. Digital platforms foster robust cooperative relationships, amplifying service delivery and enabling value co-creation with customers.

Collaboration

Digital tools streamline inter-firm collaboration, reducing transaction costs and fostering seamless online partnerships. The exchange of real-time data and collaborative innovation across sectors propels the growth of digital ecosystems and enhances supply chain cohesion.

Corporate digital transformation and operating risk: a perspective on negative impacts

Scholarly investigations into the operational risks of firms have deeply explored the influences of corporate governance, business behavior, and adjustments to external environments. Central to these discussions is the role of corporate governance-encompassing board composition, equity structure, and internal controls-in modulating risks through enhanced oversight and strategic decision-making. For instance, research suggests that gender diversity within executive teams bolsters monitoring effectiveness and diminishes risk exposure (Perryman et al., 2016). Similarly, specific business behaviors, such as Corporate Social Responsibility (CSR) (Jo and Na, 2012; Albuquerque et al., 2019), social performance (Bouslah et al., 2013), derivative hedging (Bartram et al., 2011), tax avoidance practices (Guenther et al., 2017), and customer concentration (Kim et al., 2023), significantly impact operational risk profiles. Notably, proactive CSR engagement is linked to reduced risk via improved stakeholder relationships and the acquisition of competitive advantages (Jo and Na, 2012; Albuquerque et al., 2019). Collectively, these elements underscore the pivotal role of both financial and non-financial performance in curtailing operational risks and fostering sustainable corporate growth.

In the context of CDT, emerging literature posits that this paradigm introduces distinct risk dimensions in technology, organizational management, and business processes (Dewan and Ren, 2011; Oludapo et al., 2024). Initially, while CDT fosters efficiency and innovation, it simultaneously escalates technological risks. Firms increasingly reliant on digital infrastructures may face significant disruptions from system failures or cyber threats, severely impacting operations (Martínez-Caro et al., 2020). Moreover, the misalignment of digital technologies with corporate needs can precipitate project failures, squander resources, and diminish operational efficacy. The rapid obsolescence of digital tools further complicates maintenance and escalates costs, thereby amplifying operational uncertainty (Dewan and Ren, 2011).

Second, CDT can catalyze risks associated with organizational management (Xu et al., 2024). The transition often necessitates structural adjustments away from traditional hierarchies to accommodate digital-centric workflows. This shift may result in role ambiguities and misaligned authority distribution, reducing managerial efficiency. The integration of cross-departmental digital initiatives might provoke internal conflicts due to unclear roles and responsibilities, obstructing project execution. Additionally, the heightened demand for digitally proficient personnel, such as data analysts and AI engineers, confronts firms with potential talent deficits, impairing the quality and execution of digital projects (Guerra et al., 2023). This mismatch between technological needs and available expertise heightens the complexity and unpredictability of operational frameworks.

Third, CDT may introduce business process-related operational risks (Ivanov et al., 2019). The reorganization or optimization of business processes necessitated by CDT (Baiyere et al., 2020) can engender complications such as inherent design flaws, resulting in overly complex procedures or inadequate integration between process stages. These deficiencies can extend processing times and elevate error rates, undermining operational efficiency (Wong et al., 2020). For example, a poorly configured Customer Relationship Management (CRM) system might delay the resolution of customer complaints, adversely affecting customer satisfaction and tarnishing the firm’s reputation. Additionally, CDT’s impact on external partnerships, such as those with suppliers and distributors, introduces further complications. Implementing a digital procurement system, for instance, might lead to compatibility issues with suppliers’ systems, causing delays in order processing and subsequently affecting production schedules and delivery capabilities. The varying degrees of digital adaptability among partners can significantly augment operational uncertainty, particularly in highly digitized supply chains (Rauniyar et al., 2023).

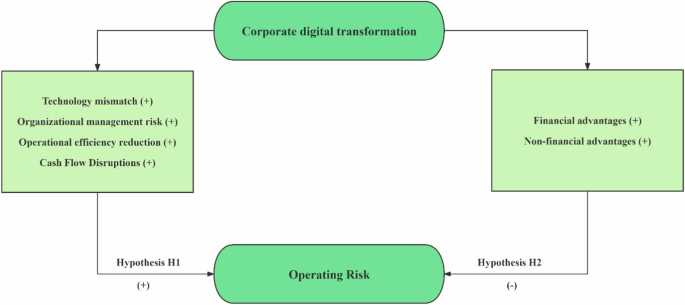

Fourth, CDT may precipitate cash flow disruptions. DT demands substantial investments in advanced hardware, such as high-performance servers, data storage devices, and smart terminals, as well as in sophisticated software solutions like Enterprise Resource Planning (ERP) and CRM systems (Kempeneer and Heylen, 2023). These expenditures can immobilize considerable capital, exerting pressure on the firm’s cash flows. DT projects are typically intricate and protracted, often requiring years from conceptualization to full operational deployment. The construction of digital factories or the overhaul of digital supply chains in large enterprises is an example, where significant capital is continuously invested over an extended period without immediate financial returns, potentially straining cash flows. Furthermore, DT frequently necessitates investments in technology research and development, the assembly of specialized R&D teams, or collaboration with external research institutes to pioneer new technological applications in business. The uncertainty and prolonged nature of these R&D investments can substantially increase short-term cash outflows, thus exacerbating financial constraints. Given these considerations, CDT may represent a case of “too much of a good thing,” where the pursuit of technological advancement intensifies cash flow challenges and elevates operational risks (Oludapo et al., 2024). Based on this analysis, we propose the following research hypothesis (H1):

H1: CDT may exacerbate operating risks for enterprises.

Corporate digital transformation and operating risk: a perspective on positive impacts

However, CDT can also bring efficiency improvements, cost reductions, and competitive advantages (Du and Jiang, 2022; Du et al., 2024), which may endow companies with competitive advantages in the product market and mitigate operational risks through both financial and non-financial channels.

The financial channel refers that CDT entails enhancing core business advantages and mitigating non-business operating risks for companies. With CDT, firms are able to collect and analyze vast quantities of data and adjust their strategies to competitive trends promptly (Chen et al., 2012; Mikalef et al., 2020; Babina et al., 2024). This agility enables companies to identify industry risks and opportunities swiftly, gaining incremental competitive edges (Erevelles et al., 2016; Kiron, 2017).

First, intelligent analysis and networked interactions facilitate the creation of products and services aligned with consumer preferences, driving innovation in product, service, and design (Babina et al., 2024; Blichfeldt and Faullant, 2021). Second, emerging digital technologies reduce customer tracking costs, enabling companies to authenticate customers more affordably and implement new forms of price discrimination based on past behaviors (Bhargava and Choudhary, 2008; Goldfarb and Tucker, 2019). Third, by refining customer tracking and behavior analysis, companies can send personalized advertisements to target customers, reducing ineffective advertising expenses and expanding market share (Goldfarb and Tucker, 2019). Lastly, big data and AI-driven cost management streamline business processes, reducing production and management costs (Kusiak, 2017). This cost reduction improves pricing advantages and market share, bolstering resilience against market competition and reducing performance fluctuations. In conclusion, CDT enhances product pricing abilities and market share, providing a shield against market risks and stabilizing performance.

Additionally, CDT may counteract the financialization trend within companies, thereby mitigating non-business operating risks. Financial asset allocation, while potentially boosting short-term performance, can erode long-term competitiveness by diverting funds away from crucial areas like R&D investment. Moreover, the volatility of financial asset prices can exacerbate overall performance fluctuations, amplifying operating risks. However, existing literature highlights the positive impact of CDT on various aspects of firm operations, including internal control quality (Jiang et al., 2022), operating and innovation performance (Chen and Srinivasan, 2024; Peng and Tao, 2022; Wu and Li, 2024; Zhai et al., 2022), cash holdings (Sun et al., 2022), and financing advantages (Liu et al., 2023a; Liu et al., 2023b). In this regard, there is less incentive for investors to allocate financial assets in accordance with motivations such as investment substitution, agency, and preventive measures. Consequently, as firms prioritize DT, the mitigation effect on operating risks is likely to strengthen further, as financialization motivations wane.

Product pricing capabilities enable firms to maintain profit levels amid rising costs by appropriately increasing prices. Should the price of raw materials rise, a company can pass on the increased costs to the product price. Furthermore, in the face of market demand fluctuations, companies can also adjust prices to balance supply and demand, thereby reducing risks associated with inventory backlogs. A larger market share often accompanies economies of scale, allowing firms to reduce unit costs in procurement, production, and sales. Moreover, companies with significant market shares are better equipped to withstand competitive pressures. When new competitors enter the market, established firms, leveraging their substantial customer bases, can retain customers through loyalty programs, thereby maintaining stable sales performance and reducing operational risks. Reducing financialization allows a company to focus more on its core business. By curtailing speculative activities in financial markets, firms lower the risks associated with financial market volatility. Decreasing the use of financial leverage can reduce a company’s debt risk. Excessive financial leverage may expose firms to significant debt repayment pressures during economic downturns, potentially leading to bankruptcy. By minimizing financialization, companies can allocate resources to core activities such as product development, production, and market expansion, thereby enhancing the competitiveness of their primary business and strengthening their ability to adapt to market changes and manage operational risks. Thus, it can be inferred that CDT, by bolstering financial performance through enhanced product pricing capabilities, market share, and avoidance of financialization, consequently reduces operational risks.

Non-financial channels of CDT include improvements in corporate governance and environmental, social, and governance (ESG) performance, contributing to lower firm operating risks. First, CDT elevates internal control quality and corporate governance standards by facilitating the presentation of all company operations in data form, thus mitigating information asymmetry among departments. This improvement in information circulation efficiency strengthens internal supervision, aids in the timely detection of control deficiencies, reduces unnecessary costs and facilitates efficient performance appraisal systems. By reducing managerial autonomy, digital technologies also enhance the independence of internal control systems, which in turn curbs irrational executive behavior. Big data analysis and artificial intelligence algorithms, for instance, enable the identification and analysis of potential risks in a timely manner, resulting in proactive risk prevention measures. Moreover, CDT enhances audit quality, augments auditor efficiency, bolsters asset review effectiveness and lowers internal personnel fraud risks (Fedyk et al., 2022).

Second, CDT fosters a stronger focus on social responsibility as internet technology streamlines internal information transmission, enabling more efficient and timely content dissemination and effective external communication. This, coupled with the popularity boost generated by CSR initiatives, amplifies firms’ commitment to social responsibility. Furthermore, the cash flow benefits of CDT provide a financial impetus for companies to fulfill their social responsibilities.

Lastly, CDT enhances corporate environmental performance by accelerating the integration of operations with digital technologies, thereby achieving intelligence and digitization in energy and sewage systems (Bendig et al., 2023; Xu et al., 2022; Zhou et al., 2023). It enables firms to integrate internal and external information to guide sustainable development strategies, fostering increased investment in green innovation. Research indicates that CDT reduces carbon emission intensity in manufacturing firms (Shang et al., 2023), electricity consumption, and intensity (Wang et al., 2022), enhances capacity efficiency (Du and Jiang, 2022), and drives green innovation (Tang et al., 2021). By improving corporate ESG performance, CDT mitigates agency, social, and environmental risks.

The mitigating effect of ESG performance on corporate operational risks manifests in several key areas: First, robust ESG performance can enhance the stability of a company’s cash flows by improving internal operational efficiency, reducing costs, increasing employee satisfaction, and optimizing governance structures. Stable cash flows help companies maintain routine operations and respond to unforeseen events amid market volatility and uncertainty, thus reducing operational risks associated with cash shortages. Companies with strong ESG performance often attract more analyst attention. Second, this attention can enhance a company’s transparency and market recognition, reducing problems associated with information asymmetry. When corporate information is more transparent, investors and other stakeholders can more accurately assess the company’s operational status and risk levels, thereby lowering the company’s financing costs and operational risks. Third, an improvement in ESG performance can help alleviate internal agency conflicts—discrepancies between the interests of owners and managers, which can lead managers to make decisions detrimental to owners’ interests. Good ESG performance can enhance transparency and governance levels, prompting managers to focus more on the long-term development and stakeholders’ interests, thus reducing agency conflicts and the associated operational risks. Fourth, companies with strong ESG performance often secure financing at lower costs. On one hand, good ESG performance can improve a company’s credit rating and reduce default risks, thus lowering debt financing costs. On the other hand, as investors increasingly value ESG performance, they are more willing to provide financial support to companies demonstrating strong ESG credentials, allowing these companies to obtain more favorable financing terms. Therefore, it is believed that by enhancing non-financial performance (ESG), CDT subsequently reduces operational risks.

Based on this, we propose the following alternative hypothesis:

H2: CDT may reduce operating risks for enterprises.

The theoretical framework of this paper is presented in (Fig. 1).

Theoretical framework diagram.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment