Most people think of the State Pension as the foundation of their retirement income.

But what if it could be viewed as a target instead?

After all, if an investor could build a portfolio capable of generating the same level of income, they would effectively have created a second State Pension of their own.

Replacing the State Pension

The full new State Pension currently pays £12,547 a year.

While that may not sound especially large, replacing it from an investment portfolio is more demanding than it first appears.

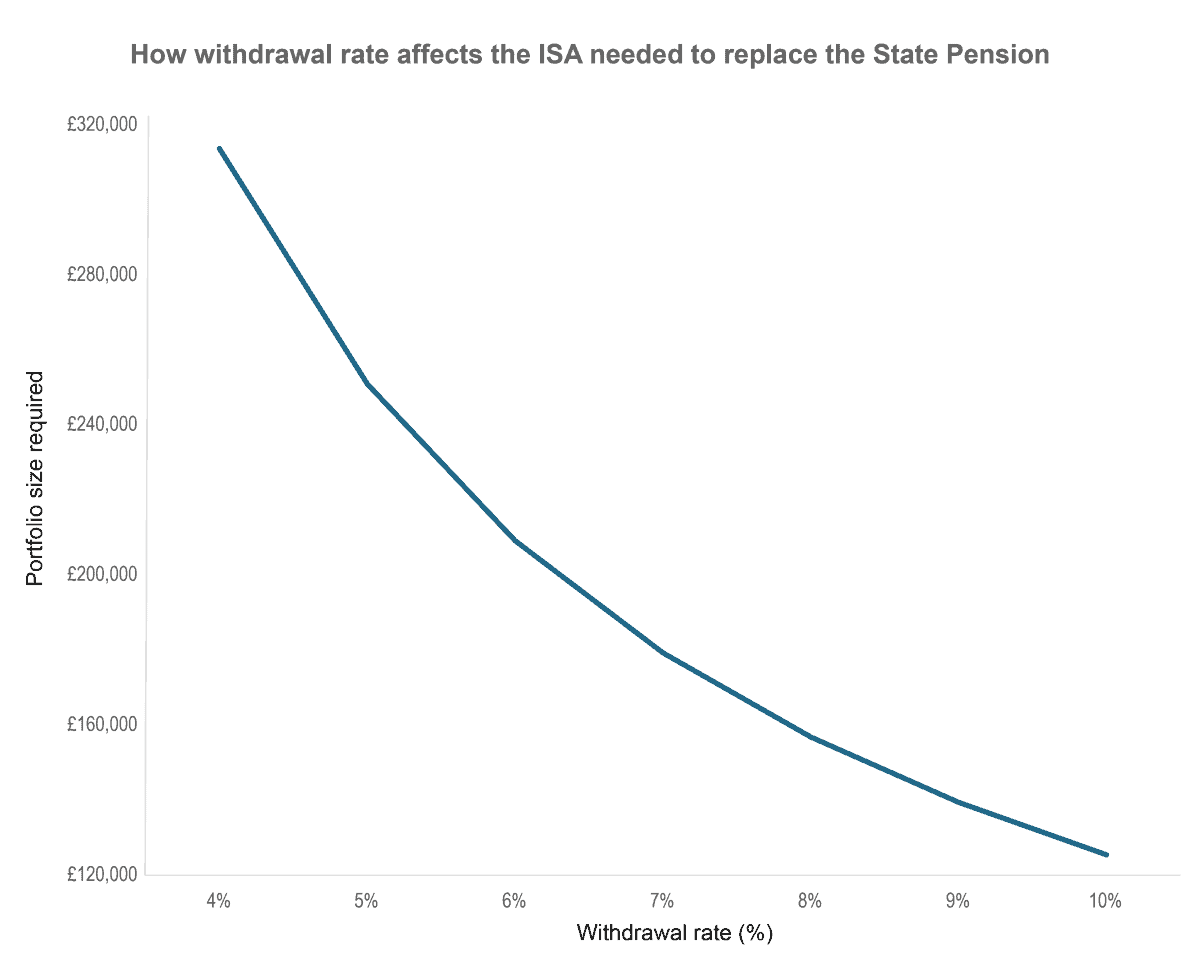

The chart below shows how much capital an investor would need in order to generate the same £12,547 of annual income, depending on the withdrawal rate applied in retirement. In other words, it assumes the portfolio is already built and then draws down income from it at different sustainable yield levels.

At a 4% withdrawal rate, which is often used as a conservative long-term benchmark, an investor would need just under £315,000. At 6%, the figure falls to just over £200,000.

The key point is that the required portfolio size is highly sensitive to the income rate assumed. A small change in withdrawal rate can significantly alter the level of capital needed to replicate the State Pension.

This highlights an important reality. While the State Pension is not a large income in absolute terms, it represents a guaranteed stream of income that would require a substantial portfolio to replace privately.

Chart generated by author

A real-world income building block

HSBC Holdings (LSE: HSBA) shows how an ISA income portfolio can be built in practice.

Over the past five years, the shares have delivered exceptional returns. A £5,000 investment would now be worth close to £18,000 once dividends are included, reflecting a total return of more than 200%. That level of performance has also translated into a very high effective yield based on the original purchase price.

Of course, the key question is whether that kind of return is repeatable. I doubt investors should assume it is.

What HSBC does illustrate, however, is how income portfolios are not built from a single perfect holding, but from businesses that generate strong cash flow over time.

The bank today is a more focused and efficient business than it was in the past. It has been simplifying operations, exiting lower-return areas, and improving capital efficiency. That has helped return on tangible equity rise and profits reach record levels.

Geography also matters. HSBC is increasingly exposed to faster-growing regions, particularly Asia and the Middle East, where wealth creation is supporting demand for savings and investment products. That has helped wealth revenues grow strongly in recent periods.

There are risks to consider. A slowdown in China or weaker global trade would impact earnings, and falling interest rates could pressure margins over time.

Even so, HSBC shows how an income-focused ISA portfolio might be constructed in practice. Not through a single high-yield solution, but through a mix of strong, cash-generative businesses capable of compounding returns over time.

It remains a core holding in my own ISA portfolio, though it’s not the only stock I see playing that role in the years ahead.

Should you invest £5,000 in HSBC Holdings right now?

When investing expert Mark Rogers and his team have a stock tip, it can pay to listen. After all, the flagship Twelfth Magpie Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if HSBC Holdings made the list?

Andrew Mackie owns shares in HSBC.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment