We’re refreshing the Morningstar Medalist Rating’s methodology to provide a simpler, more transparent forward-looking assessment of mutual funds, exchange-traded funds, and other managed investments, including semiliquid funds and 529 college savings plans. Gold, Silver, and Bronze ratings will continue to identify funds that Morningstar expects to outperform the category average over a full market cycle.

First announced in December 2025, the updated methodology better illustrates how we evaluate a fund’s expenses, and it introduces a simplified rating structure, new quantitative calculations, and fixed thresholds for assigning ratings across more than 360,000 share classes globally.

These changes are designed to improve transparency, consistency, and comparability across funds, whether ratings are driven by analysts or produced algorithmically. What is not changing is the continued focus on the three fundamental pillars used to assess the likelihood of outperformance: People, Process, and Parent.

The new Medalist Rating framework began to be implemented on a rolling basis on Thursday, April 23. Global implementation will be completed by Sunday, May 3, at which time, every Medalist‑rated share class will reflect the updated methodology, giving investors a clearer view of Morningstar’s highest‑conviction opportunities under the simplified approach.

What Is the Morningstar Medalist Rating?

To arrive at a Medalist Rating, Morningstar analysts—or an algorithm, if an analyst isn’t assigned to cover the fund—assess three fundamental pillars to determine whether it can outperform its category peers: People, Process, and Parent. The People Pillar encompasses the managers and analysts making a fund’s key investment decisions. The Process Pillar considers the effectiveness and repeatability of its investment strategy, while the Parent Pillar analyzes the offering firm and whether it puts fund investors’ interests before its own. (As of March 31, 2026, funds domiciled in Australia and New Zealand are not eligible for Medalist Ratings with algorithmic components.)

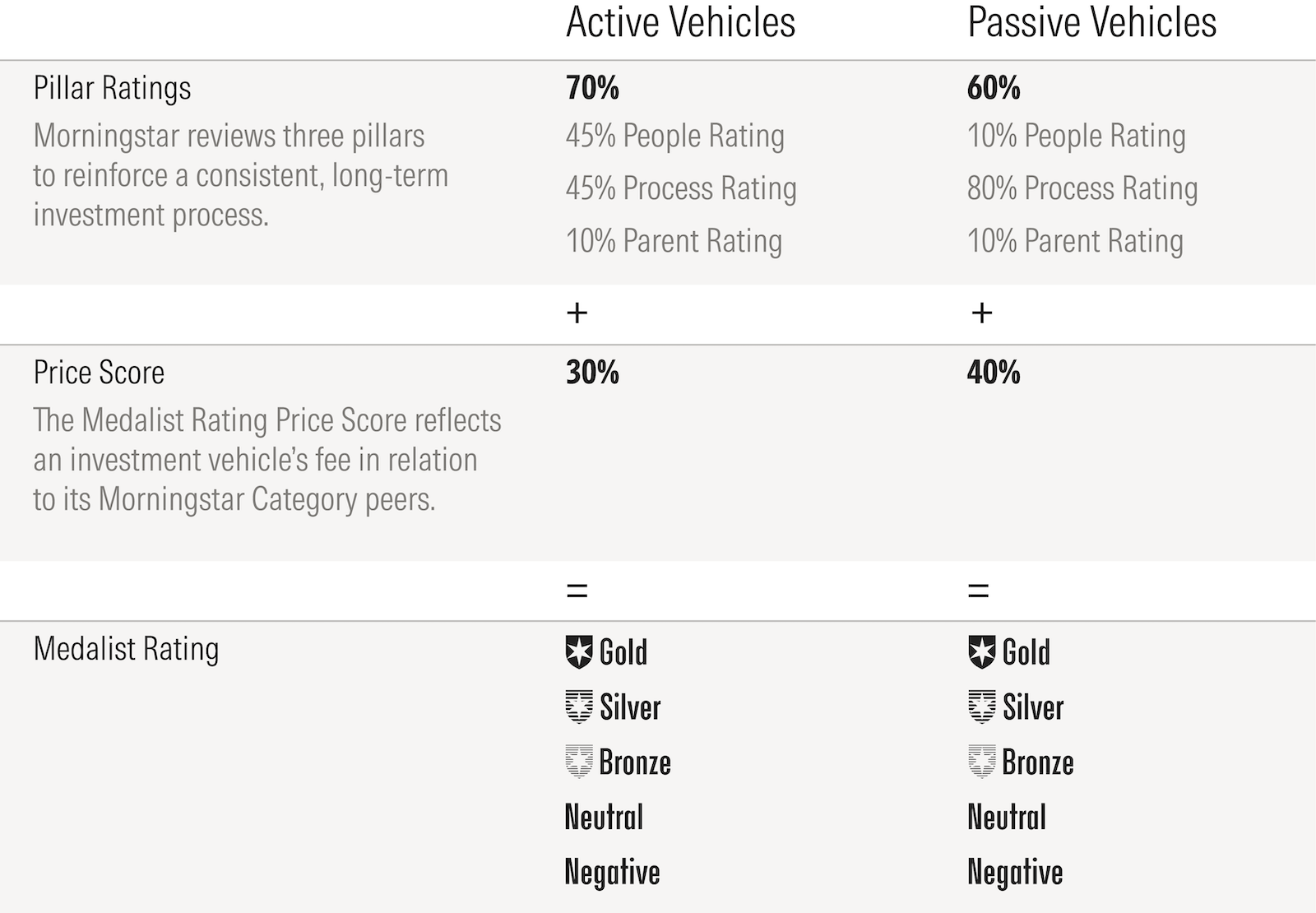

Morningstar combines a fund’s fundamental pillar assessments and, together with an assessment of the fund’s price and likelihood of outperforming its category peers, awards it a Gold, Silver, Bronze, Neutral, or Negative rating.

Distribution of New Medalist Ratings

The methodology update will not change most funds’ overall Medalist Rating, and those that do change will typically reflect a one-notch move on the rating’s unchanged scale of Gold, Silver, Bronze, Neutral, or Negative. Overall, there will be more Gold and Silver ratings and fewer Bronze, Neutral, and Negative ratings.

The Simplified Structure

Before we get into the changes’ details, here’s what’s staying the same: Morningstar’s 130 global researchers will continue to qualitatively rate more than 3,200 fund strategies’ fundamental pillars in the same transparent manner they have used for decades. The analysts’ structured, well-documented, and peer-reviewed process consistently assesses funds’ investment quality and distinguishes those with stronger characteristics and better odds of future outperformance.

The simplified Medalist Rating will make funds’ future performance drivers relative to their category peers clearer and highlight which funds Morningstar expects to outperform their peer group averages over a full market cycle.

We’ll continue to display People, Process, and Parent Pillar ratings as High, Above Average, Average, Below Average, and Low. We’re further enhancing the rating by displaying a Medalist Rating Price Score of negative 2.5 to 2.5 to illustrate whether a fund’s fee is a significant headwind or a competitive advantage, as fees are often the best predictor of future performance. The Medalist Rating Price Score will boost low-cost funds’ ratings, while reducing those of expensive funds.

The new approach applies straightforward weights to each rating component and sums them to determine the fund’s Medalist Rating. Component weights differ for actively managed funds and passively managed funds to reflect how those strategies are run.

Here’s an example of how the fundamental pillars and the Medalist Rating will be displayed for a few share classes of a US large-growth equity fund:

Taking a Category-Relative Approach

The updated methodology does not factor into the ratings calculation the degree to which a category’s funds had been able to generate alpha in the past relative to their category index. The outgoing methodology assumed every fund in a category aimed to beat the Morningstar-assigned benchmark.

Comparisons to the category benchmark created challenges for some funds. Many multi-asset allocation, noncore equity, and fixed-income funds have asset allocation and/or sector weights that differ significantly from the category benchmark, making that benchmark test less relevant than peer-to-peer comparisons. Instead, the new approach measures Medalists versus their category averages, rather than their category benchmarks.

More-Transparent Inputs

Of the 175,000 traditional fund and ETF share classes that received a Medalist Rating on March 31, 2026, about 130,000 relied on an algorithm to provide at least one pillar score where an analyst hadn’t rated it directly. Our previous approach used a machine-learning model to generate these ratings by mimicking how analysts set scores. While the model effectively identified funds likely to perform well, its adaptive nature made it difficult to pinpoint which data influenced a fund’s Medalist Rating.

The updated algorithmic pillar methodology uses clearer and more-transparent input data. We’ll now show simple calculated data points that reflect how a Morningstar analyst would assess each pillar. For example, analysts look at managers’ experience when evaluating the People Pillar. The model that helps determine the People Pillar rating now includes a new data point—Fund Manager Successful Experience—to measure which funds are run by managers with a proven ability to outperform across their career.

For active funds’ Process Pillar ratings, the algorithm now considers their information ratio, or their cumulative return divided by their tracking error relative to their index. The assessment also includes data that measures style drift and volatility, as well as the firm’s past success at delivering outperformance within the fund’s asset class.

The algorithmic Parent Pillar considers the fees, manager tenure and retention, performance, and survival and obsolete rates of an asset manager’s full fund lineup.

For passively managed funds, the Process Pillar carries the most weight in determining the Medalist Rating. The algorithmically generated pillar stresses the historical ability of passives to outperform actives in a category, volatility of their excess returns versus the category index (tracking error), and concentration risk among portfolios’ top holdings, among other measures.

This simplified quantitative methodology will make it easier to identify which data contributed to a fund’s Medalist Rating and how. We will continue to mark algorithmic pillars with a superscript Q in our data displays and reports.

For funds assessed through algorithmically generated pillars, we require that the fund has sufficient data coverage to fuel at least half of the pillar’s calculation. If the fund doesn’t meet the 50% data-calculation rate, it will not receive a Medalist Rating. This new requirement will limit the number of fully quantitative Medalist Ratings among newer funds, as well as funds in markets where public disclosure is less robust. Japan, for example, does not require funds to disclose who manages the portfolios, so many are ineligible for the People calculations driving the quantitative rating, such as Fund Manager Successful Experience.

Assigning Medals With Fixed Rating Thresholds

The updated methodology does away with the Medalist Rating’s existing forced distribution curve, which previously limited the number of Gold-, Silver-, and Bronze-rated funds in each category. The curve has been replaced by fixed thresholds. We expect the simplified approach, including the long-term nature of the data behind the algorithmic pillars, to create a more stable set of ratings.

We understand investors monitor their funds’ Medalist Ratings and have questions when ratings change. The simplified approach will increase stability by eliminating a forced distribution of ratings that caused ratings to change based on updates to other funds.

Implementing the Simplified Methodology

By rolling out the changes starting on April 23, we’re applying the new fixed-threshold scores to all funds at once, to make easy comparisons. When we applied the updated calculations to existing Medalist Ratings, we saw fewer Bronze, Neutral, and Negative ratings and more Gold and Silver ratings relative to the previous methodology. That doesn’t mean it’s easy to get a Gold, Silver, or Bronze rating: About a third of the updated ratings will translate to a better-than-Neutral medal under the updated methodology.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment