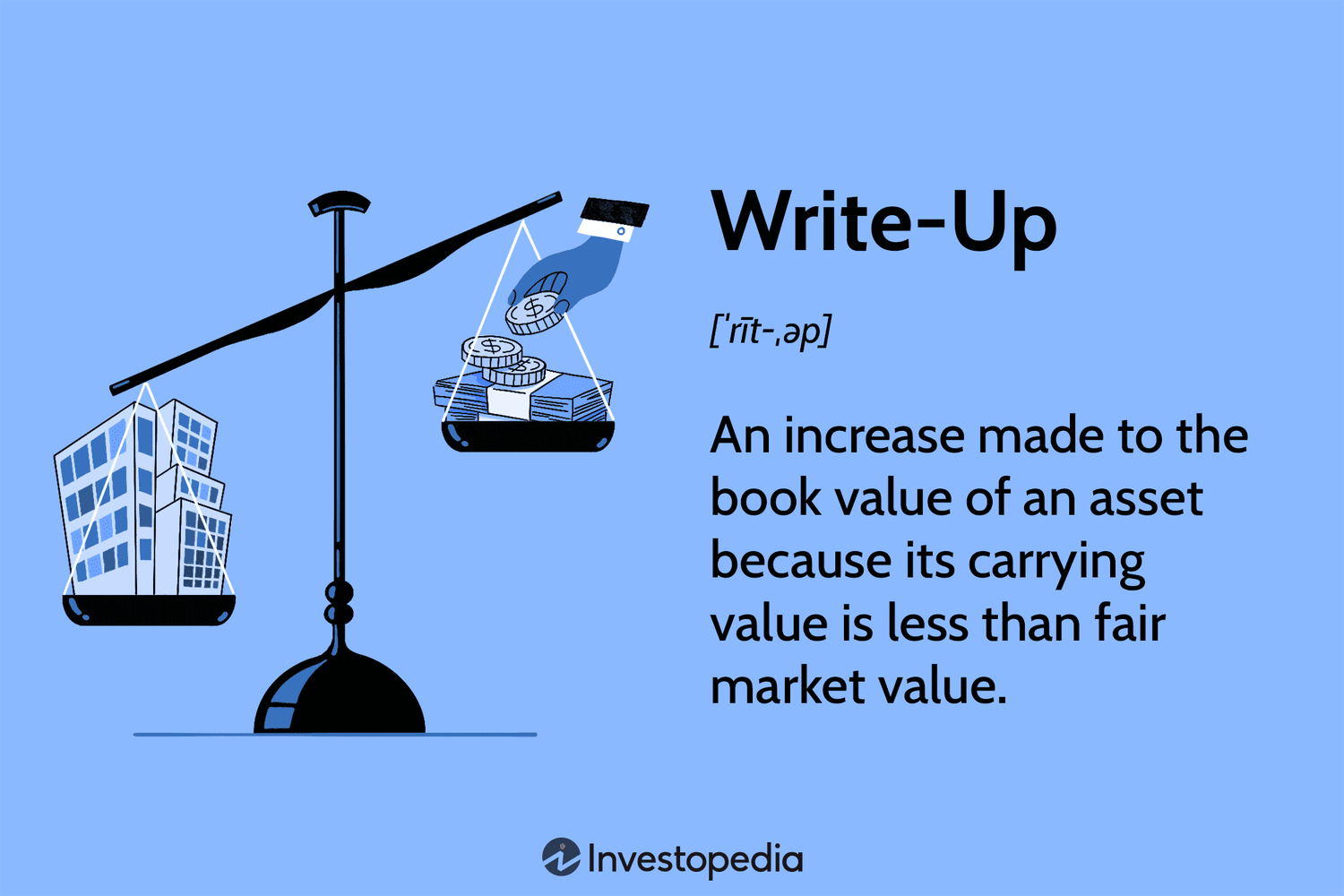

What Is a Write-Up?

A write-up is an increase made to the book value of an asset because its carrying value is less than fair market value. A write-up generally occurs if a company is being acquired and its assets and liabilities are restated to fair market value, under the purchase method of M&A accounting. It may also occur if the initial value of the asset was not recorded properly, or if an earlier write-down in its value was too large. An asset write-up is the opposite of a write-down, and both are non-cash items.

Understanding Write-Ups

Because a write-up impacts the balance sheet, the financial press does not report on more mundane instances of businesses initiating a write-up of asset values. In contrast, sizable write-downs do spark investor interest and make for better news cycles.

Whereas a write-down is generally considered a red flag; a write-up is not considered a positive harbinger of future business prospects — since they’re generally a one-time event.

During an asset write-up, special treatment for intangible assets and tax effects are considered. With an asset write-up, the deferred tax liability is generated from additional (future) depreciation expense.

Example of a Write-Up

For example, assume Company A is acquiring Company B for $100 million, at which point the book value of Company B’s net assets was $60 million. Before the acquisition can be completed, Company B’s assets and liabilities have to be marked-to-market to determine their fair market value (FMV).

If the FMV of Company B’s assets is determined to be $85 million, the increase in their book value of $25 million represents a write-up. The difference of $15 million between the FMV of Company B’s assets and the purchase price of $100 million, is booked as goodwill on Company A’s balance sheet.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment