Munis were weaker Thursday as U.S. Treasuries and equities rallied on the news that President Donald Trump canceled further strikes on Iran and announced a deal is near.

Processing Content

Muni yields were cut up to five basis points Thursday, depending on the scale, after yields rose up to two basis points the day prior.

The muni market has been “exceptionally resilient,” given the macro backdrop, said Ilya Perlovsky, fixed-income market strategist at Fidelity Investments.

“Munis face a crossroads at an unusual time in June — when strong reinvestments are supposed to drive steady distribution,” said Kim Olsan, senior fixed income portfolio manager at NewSquare Capital.

A clog in certain areas of the curve “speaks to stretched valuations … and potentially higher selling volume could complicate distribution,” she said.

Bids wanted reached $1.51 billion Wednesday on Bloomberg’s platform, the highest daily total since last December, Olsan said.

The level of secondary offerings also indicates caution, as the offerings rose to nearly $10 billion from recent daily totals closer to $7 billion, she said.

New-issue bonds saw select price bumps Wednesday but were less dramatic than in previous weeks, Olsan said.

“Massachusetts’ GO final pricing brought lower yields in the 5s due between 2044 and 2047 (a steep curve slope where SMA programs can operate), but the bonds due from 2032 to 2035 in the smaller series saw yields rise 3–5 basis points from retail order period levels (where richer ratios exist),” she said.

In the negotiated market next week, supply includes $673.865 million of aviation revenue refunding bonds from Miami-Dade County, Florida; $509.62 million of affordable housing revenue bonds from the New York State Housing Finance Agency; and $470 million of New York University revenue bonds from the Dormitory Authority of the State of New York.

Washington leads the competitive calendar next week with $1.524 billion of GOs from the state in four series.

Overall, 2026 has been another record year for issuance. Supply is at $261.092 billion year-to-date, up 2.3% year-over-year, according to LSEG.

Around one-quarter of the issuance year-to-date comes from nontraditional muni sectors, such as energy prepays, hospitals, higher education and housing, Perlovsky said.

This percentage of total supply has been rising over the past years, while issuance of GOs and essential service revenue bonds has declined, potentially explaining some of the richness in the market, he noted.

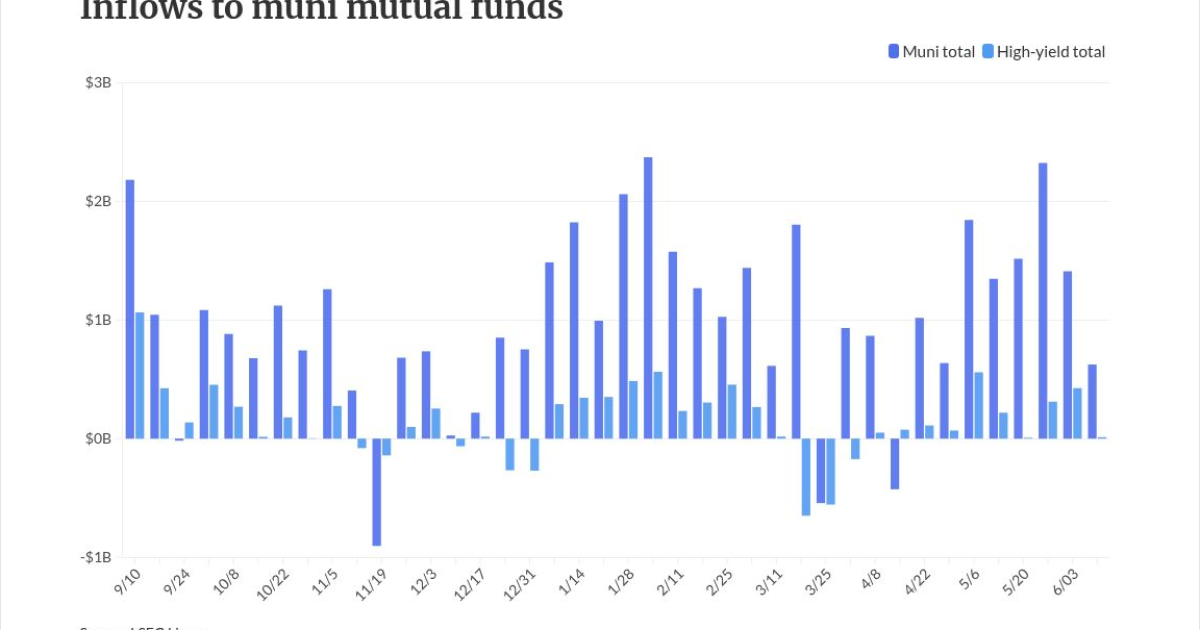

Investors added $624.6 million into municipal bond mutual funds in the week ended Wednesday, following $1.412 billion of inflows the prior week, according to LSEG Lipper data.

High-yield funds saw inflows of $11.8 million compared to inflows of $425.6 million the previous week.

Inflows into muni mutual funds have been sizable. Part of the reason is a strong equity market, potentially helped by a lot of the model portfolios rebalancing into fixed income, Perlovsky said.

Flows last year were not nearly as strong and were disrupted by the tariff rollout, which spooked the market, he noted.

However, fund flows have, for the most part, not been disrupted by the closure of the Strait of Hormuz and the Iran conflict, Perlovsky said.

New-issue market

In the primary market Thursday, BofA Securities priced for the New York City Housing Development Corp. (Aa2/AA+//) $438.415 million of sustainable development multi-family housing revenue bonds. The first tranche, $183.73 million of non-AMT 2026 Series G-1 bonds, saw all bond price at par: 3.1s of 5/2031, 3.75s of 5/2036, 3.8s of 11/2036, 4.3s of 11/2041, 4.7s of 11/2046, 4.85s of 11/2051 and 4.95s of 11/2056, callable 11/1/2033.

The second tranche, $254.685 million of non-AMT 2026 Series G-2 bonds, saw 3s of 5/2066 with a put/tender date of 1/2029 price at par.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment