There’s always gonna be another mountain

I’m always gonna wanna make it move

Always gonna be an uphill battle

Sometimes I’m gonna have to lose

Ain’t about how fast I get there

Ain’t about what’s waiting on the other side

“The Climb” by Miley Cyrus

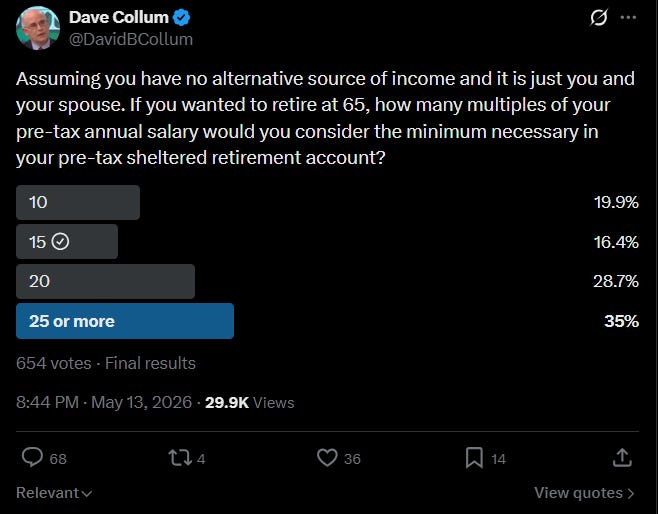

Dave Collum, a remarkably financially numerate Cornell chemistry professor, and someone I consider a “Twitter friend” who actively follows and promotes my work shared a poll on Twitter this past week:

I want to make clear a number of assumptions that Dave outlined later in his responses (but should have been clear from the language):

-

No Social Security or Medicare

-

No children (“just you and your spouse”) to take care of

-

Pre-tax sheltered retirement account (401K or IRA) [so no house, business, etc]

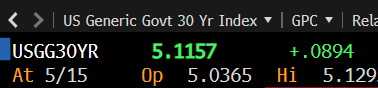

Simultaneously on my screen:

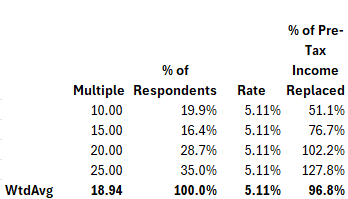

So let’s do some simple math:

At the “crowd weighted average” (ignoring the “or more” on the 25x), the opportunity exists to replace 100% of PRE-TAX income with 30yr nominal treasury bonds simply with interest on that bond. Never touching principal. And since it’s “just you and your spouse” there’s nobody to benefit from that principal, completely intact, at age 95 except (possibly) you and your spouse. Odds you’ll both make it that far? About 5% for affluent (ie 20x) households. 1% for the deplorables.

In the comments, Amy Nixon, a financial commentator, said she’d initially leaned toward 20 times salary and then rolled it back to 15 (where I voted) — her reasoning being that expenses fall off once the kids are through college and the household is two adults again, for meals, for travel, for the ordinary buying of things. You can disagree with the number. But notice what she’s doing: she’s reasoning about spending. Remember your pre-tax income includes money paid for taxes, FICA, etc. And saving to get to that 20x level. Your SPENDING runs about 65% of that pre-tax income. So 20x is 31x your spending.

Dave said 25x. And then he flagged what he called the interesting part: that Fidelity’s website, at one point, said 8x.

An 8x-versus-25x gap is not a curiosity. It is a threefold discrepancy with an important message. Fidelity’s number assumes you draw your principal down over retirement and that Social Security carries a large share of the load. A 25x-of-salary number quietly assumes something completely different: that you live off a withdrawal rate of roughly 3 percent, Social Security is untrustworthy, and never touch the principal at all. Those aren’t competing estimates of the same quantity. They are answers to two different questions. The question Dave is answering is “fear” — and we see it permeating our society:

The older generation’s saving is income NOT received by their children. Dave, admittedly, is saving more because he’s worried about the prospects for his children to adequately provide for THEIR retirement. As I noted to the younger generation in a recent (terrible btw) podcast, their behavior is part of the problem; but the older generation isn’t helping:

At 20x+ (64% of respondents obviously skewed by Dave’s follower orientation), you’re saving 31x your spending. At 65, you could earn 0% and cover spending until 96.

I know what the crowd is shouting — “Inflation! It’s coming, and it’s understated! You can’t buy nominal bonds, you fool!”

And maybe they’re right (I don’t think so). But I’d like you to consider something:

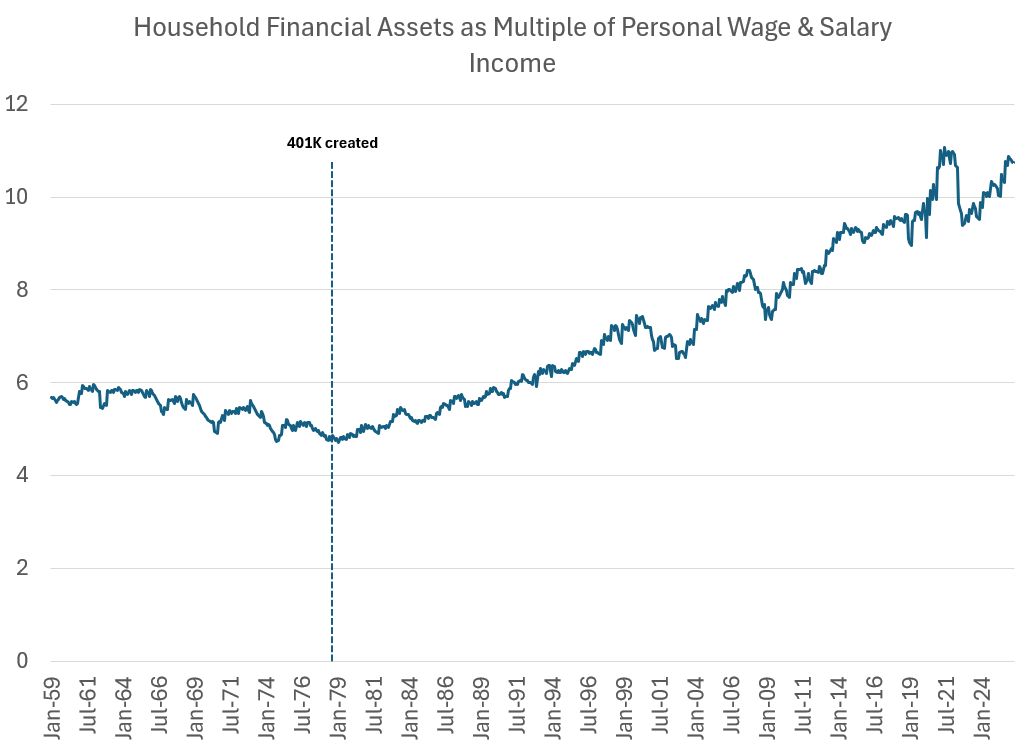

The shift from Defined Benefit to Defined Contribution, beginning in 1978, shifted the “fear” of providing retirement from the corporate (and public) sector to the household sector. As discussed in my analysis of the Coimbra paper, the shift from COLLECTIVE security to individual security drives an astonishing outward shift in aggregate demand for financial assets:

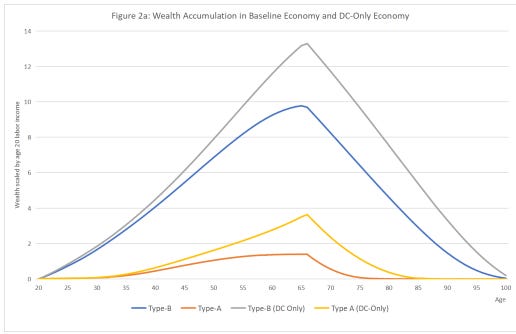

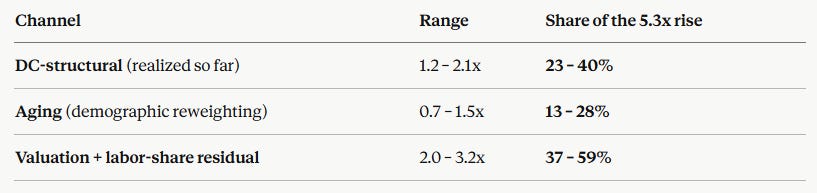

While Coimbra doesn’t specify the fraction of Type-A (spenders) and Type-B (savers), the aggregate results for the paper suggest roughly 50/50. If we reverse solve for the drivers of the increase in Financial Assets/Income, we get these rough ranges:

The aging of the society that has occurred since 1978 would have driven expected financial asset/income ratio higher by 0.7-1.5x — roughly 1/8 to 1/4 of the amount we’ve seen. Between 60% and 99% (conjoint lower and upper ranges) is due to the shift to DC and an increase in valuation (a combination of shift to passive and increased aggregate demand), or (and this is an important point) the decline in labor share of the economy. The NY Fed has recently written that labor share appears to play an important role in setting real rates:

And as my readers know, I believe the evidence strongly supports this conclusion:

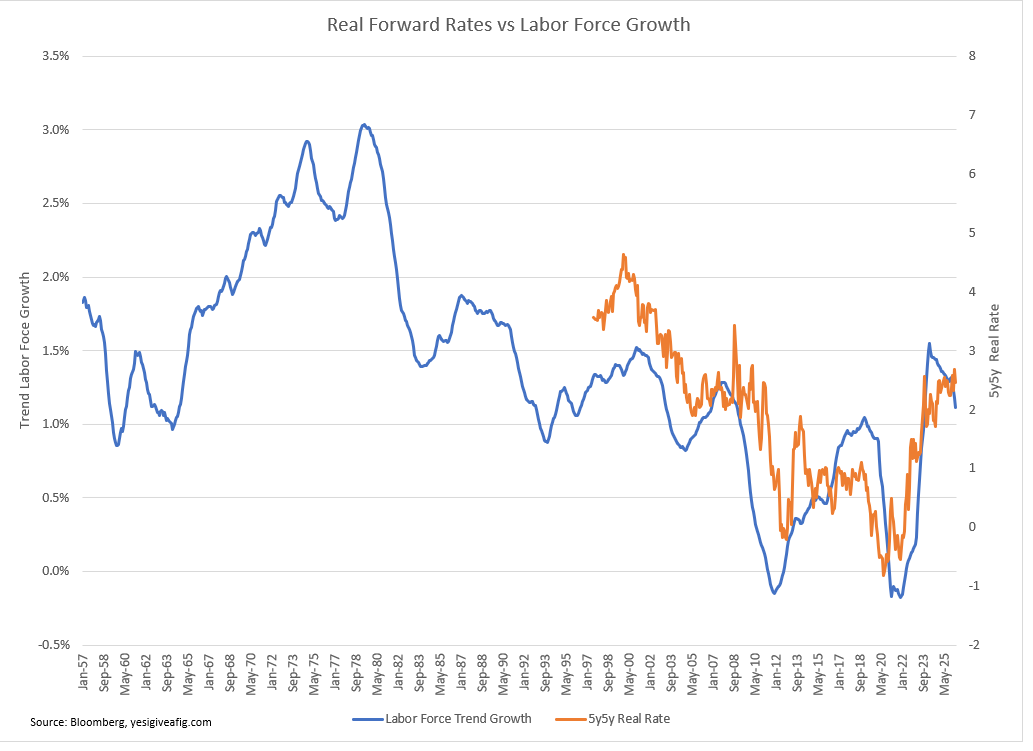

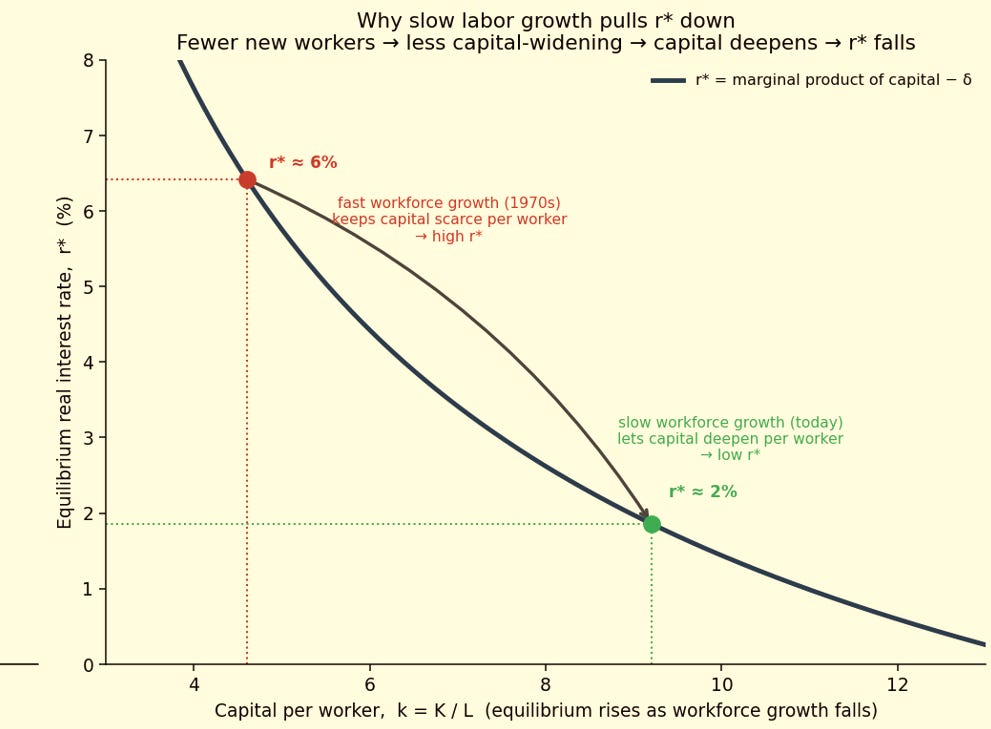

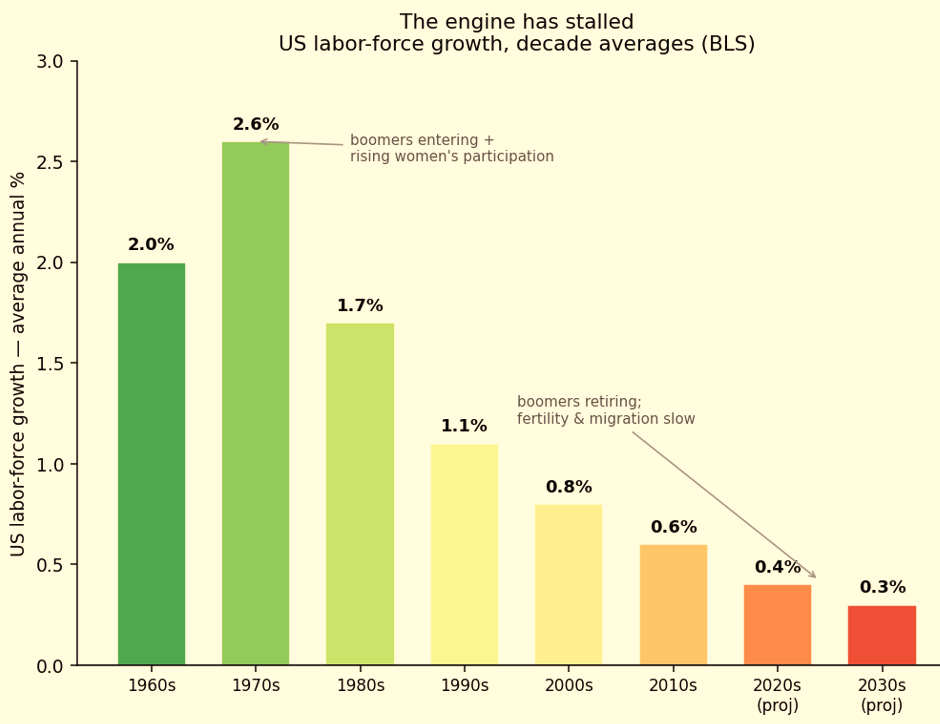

Why does this relationship exist? Because the production frontier in economics ASSUMES a capital/labor ratio. With fast labor force growth, the demand for capital must rise to maintain the capital/labor ratio, driving real rates higher. THIS was the story of the 1970s — an explosion of domestic labor created a large outward shift in aggregate demand both for consumption AND capital:

And so today, with labor force growth expected to be negligible, real rates SHOULD be lower.

But they’re not:

Now we have multiple solutions to this conundrum. Possible solutions:

-

The market is brilliantly telling us that the US government is lying about inflation

-

The market is stupid and real rates are going much higher because (pick A/B/C) — the theoretical models are stupid as well. It’s different this time.

-

The market is stupid because mechanical features are driving neglect of bonds in portfolios that mechanically buy in proportion to market capitalization of bonds and an age-based allocation to assets that ignores reasonable expected returns.

We can evaluate #1 and #3. #2 is simply expectations. Ewe have one. So does everyone else. I’d urge you to consider what’s special about yours.

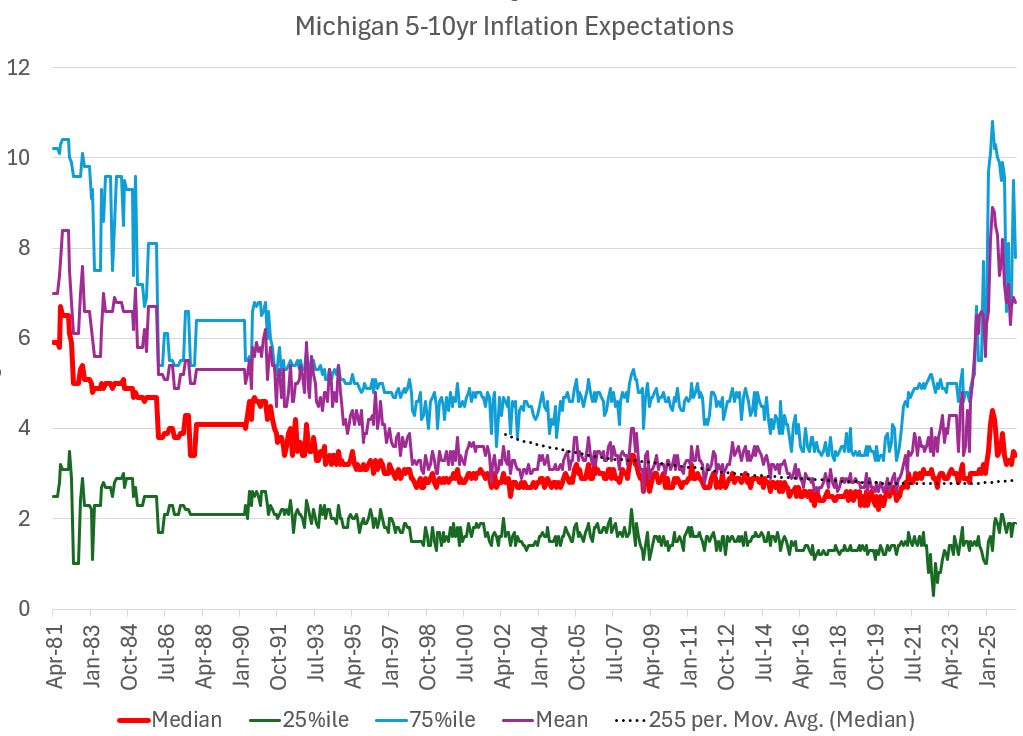

On #1, the “government is lying”, many like to roll out the chart on UMich inflation expectations where the “mean” has soared. Unfortunately, this is due to outliers amplified by the 2023 switch from phone to internet surveys. On the internet, nobody knows you’re a conspiracy theorist, dawg. The median expectation is 3.1% — slightly elevated, but far from 1981 levels:

We’ll always have ShadowStats, but legitimate PRIVATE sector peers to the CPI suggest the BLS is OVERSTATING inflation by about 1.5%. Please ask yourself, “What incentive does Truflation have to lie?” I can assure you, their business model is better served by suggesting the opposite:

You can also ask yourself, “What incentive does Mike Green have to lie to me?” Well, obviously, I’m just an active manager trying to hold on to my fiat power base as I type away on Sunday morning. (We are legion in case you’re wondering)

The data does not suggest the BLS is “lying to you” — and as many have noted, never assume conspiracy when incompetence will suffice. And there is plenty of evidence of incompetence (mostly from my barber, but also at the BLS):

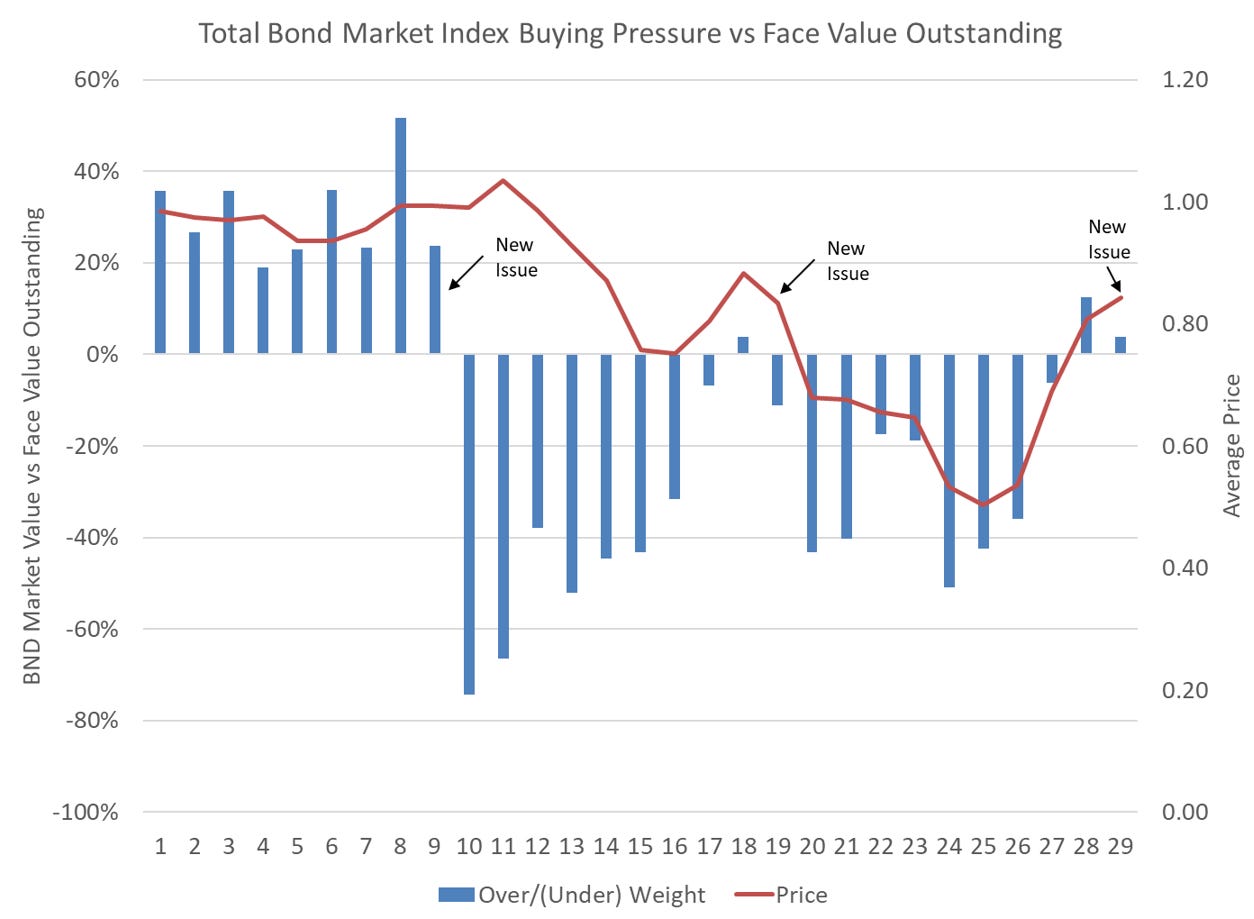

As I noted, #2 is “Like, just your opinion, man…” so let’s take a look at number three — mechanical:

I cannot emphasize this enough—we KNOW this is true. It’s been confirmed by passive bond funds to the US Treasury. We also know what happened to small cap value stocks in 1999 when improperly constructed market cap wtd indices ignored float and overweighted new IPOs vs depressed value stocks:

Do ewe see what I see?

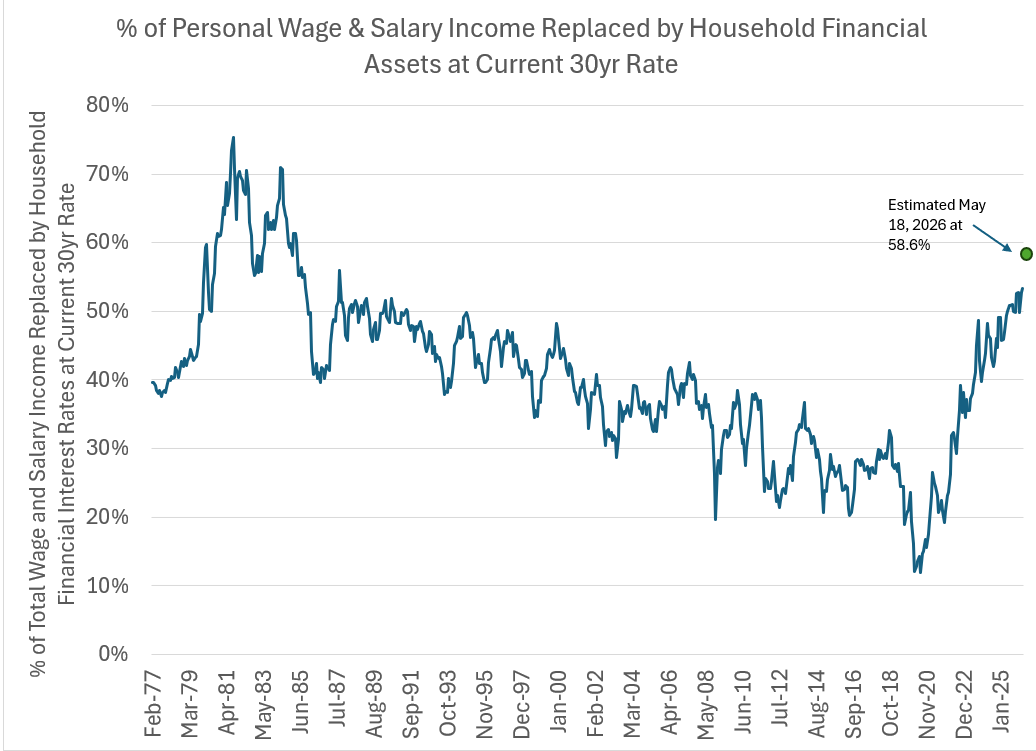

So I’ll leave you with this observation — as of May 18, 2026, you’ll have the opportunity to sell your other financial assets and buy 30yr US treasuries at a level of income replacement unmatched except for the four years of Volcker rates 1979-1982:

You don’t need to care about my “real rates argument” — you don’t need the capital gains, and your principal is protected in nominal terms. Again, at 5% and 20x you’re never touching principal. You’re starting out your retirement with income 1.5x your current spending. You’ll ADD to principal. At 10x (America’s average), even with Social Security cut by 25%, most will also never touch the principal. Will you do it? Almost certainly not. Because we’re sheep. And the lone sheep is prey for the wolf.

“Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.” — Keynes

But that’s not the question, really. The question is, when are OTHERS going to come to the conclusion that the future might not be driven by an overtly manipulated SpaceX IPO at 100x revenue, but rather by bonds? The “Keynesian Beauty Contest”:

. . . in which the competitors have to pick out the six prettiest faces from 100 photographs, the prize being awarded to the competitor whose choice most nearly corresponds to the average preferences of the competitors as a whole: so that each competitor has to pick, not those faces that he himself finds prettiest, but those that he thinks likeliest to catch the fancy of the other competitors, all of whom are looking at the problem from the same point of view . . . We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth, and higher degrees.

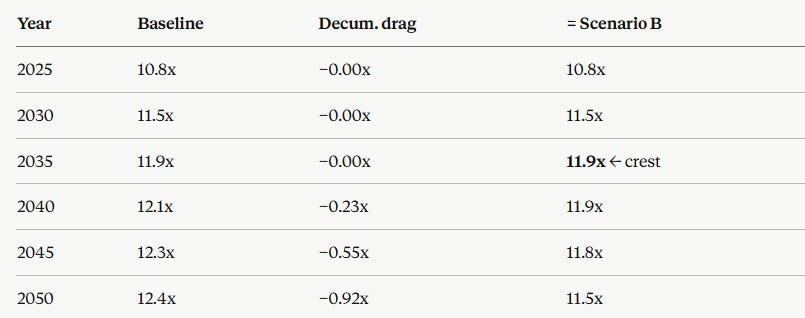

And just remember, that rising multiple of financial assets to income has an expiry date based on demographics. If equity valuations begin to retreat as Boomers decumulate, it will fall faster (note my work suggests somewhere between 2030 and 2035 is when passive makes this all moot):

Your call, America. My hunch is that you’ll go with the IPO and emerge shaken, not stirred.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment