CoreWeave(NASDAQ: CRWV) is one of the fastest-growing stocks on the market. Wall Street analysts expect huge revenue growth over the next two years, with 2026’s revenue expected to rise 147% year over year and 97% in 2027.

Those are incredible growth rates, and will result in CoreWeave’s revenue rising from $5.1 billion at the end of 2025 to nearly $25 billion by the end of 2027 (if projections pan out).

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

That’s a major business expansion in a short time frame, and that kind of growth gets investors excited. But is the stock worth buying?

Image source: Getty Images.

CoreWeave isn’t guaranteed to win

CoreWeave is known as a neocloud company, meaning it operates as a cloud computing business with an artificial intelligence focus. In CoreWeaves’s case, it fills its data centers with cutting-edge GPUs from Nvidia(NASDAQ: NVDA), then rents those back to clients for excess AI computing power. Nvidia is so confident in CoreWeave that it owns more than 47 million shares — or about 9% of the company. A company like Nvidia, with a huge growth rate and countless opportunities, doesn’t invest in outside businesses for no reason; it sees huge potential that could lead to outsize returns.

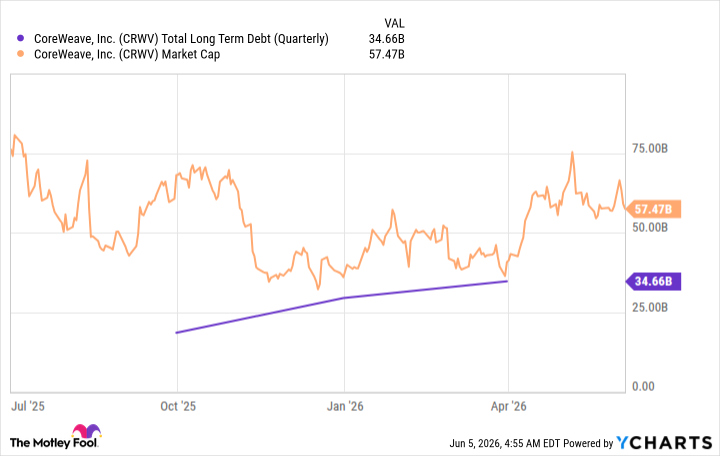

Nvidia has invested heavily in CoreWeave, but it needs it. Unlike the major cloud computing providers, CoreWeave doesn’t have a base business to fund its operations. So, it needs to seek external investors or take on debt to build out its data center footprint. This isn’t cheap, which leads to major execution risk for CoreWeave.

CRWV Total Long Term Debt (Quarterly) data by YCharts

However, the upside is immense if CoreWeave can form a profitable business. It’s not uncommon to see operating margins of 30% or higher in fully mature cloud computing businesses. Add in taxes and other depreciation costs, and it’s not out of the question for CoreWeave to achieve a 15% profit margin. Should CoreWeave do that on a revenue base of $25 billion (what Wall Street projects in 2027), that could lead to the company generating nearly $4 billion in profits, valuing it at 15 times hypothetical forward earnings. That’s actually a pretty reasonable price.

But CoreWeave must produce real profits before that’s even feasible. The economics of the business are there, as is the growth. We’ll see how the execution plays out, as the industry is a long way from the AI build-out wrapping up, so investors should expect big losses and continued massive spending. But with a $100 billion backlog to churn through, I think CoreWeave makes for a solid investment with major upside.

Should you buy stock in CoreWeave right now?

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $442,220!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,230,114!*

Now, it’s worth noting Stock Advisor’s total average return is 926% — a market-crushing outperformance compared to 203% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of June 12, 2026.

Keithen Drury has positions in Nvidia. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment