As the UK market contends with global economic uncertainties, particularly influenced by China’s sluggish recovery, the FTSE 100 and FTSE 250 indices have recently experienced downward pressure. In such a challenging environment, growth companies with high insider ownership can offer a unique perspective on potential resilience and confidence in their long-term prospects.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Quantum Base Holdings (AIM:QUBE) | 31.8% | 111.8% |

| Optima Health (AIM:OPT) | 28.0% | 56.3% |

| Mortgage Advice Bureau (Holdings) (LSE:MAB1) | 18.5% | 27.7% |

| Metals Exploration (AIM:MTL) | 10.2% | 87.4% |

| Manolete Partners (AIM:MANO) | 32.7% | 38.1% |

| Hochschild Mining (LSE:HOC) | 38.3% | 27.1% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.6% | 24.9% |

| EnSilica (AIM:ENSI) | 36% | 82% |

| Energean (LSE:ENOG) | 19% | 27.3% |

| Cambridge Cognition Holdings (AIM:COG) | 25.9% | 75.8% |

We’re going to check out a few of the best picks from our screener tool.

Simply Wall St Growth Rating: ★★★★☆☆

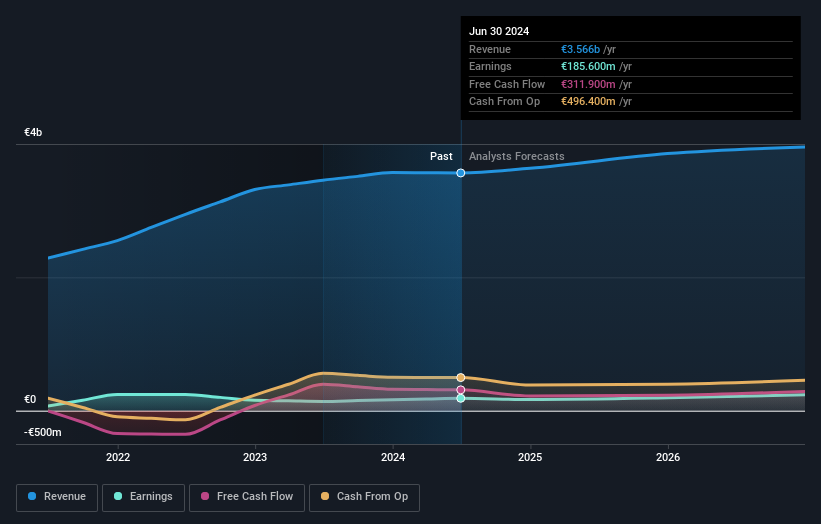

Overview: Griffin Mining Limited is a mining and investment company focused on the mining, exploration, and development of mineral properties with a market cap of £573.92 million.

Operations: The company’s revenue is primarily derived from the Caijiaying Zinc Gold Mine, which generated $137.50 million.

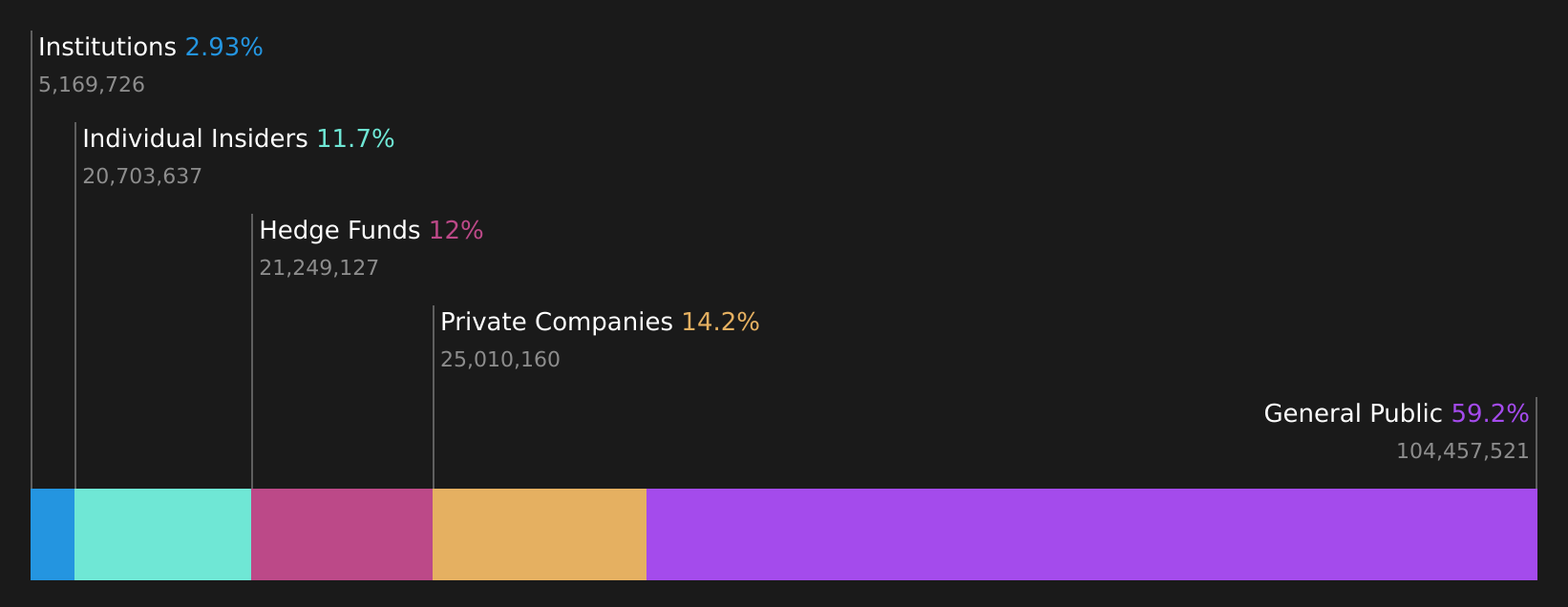

Insider Ownership: 11.7%

Griffin Mining’s earnings are expected to grow significantly at 30.8% annually, outpacing the UK market. Despite slower revenue growth at 11.3%, it surpasses the UK average and trades 20% below its estimated fair value, suggesting potential upside. Recent developments include a successful production blast in Zone II, enhancing operational capacity until 2054. The company reported net income of US$22.06 million for 2025, nearly doubling from the previous year, reflecting strong financial performance amidst strategic expansions.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Gulf Keystone Petroleum Limited, with a market cap of £395.75 million, explores, evaluates, develops, and produces oil and gas in the Kurdistan Region of Iraq.

Operations: The company’s revenue segment primarily consists of $193.09 million from the exploration and production of oil and gas in the Kurdistan Region of Iraq.

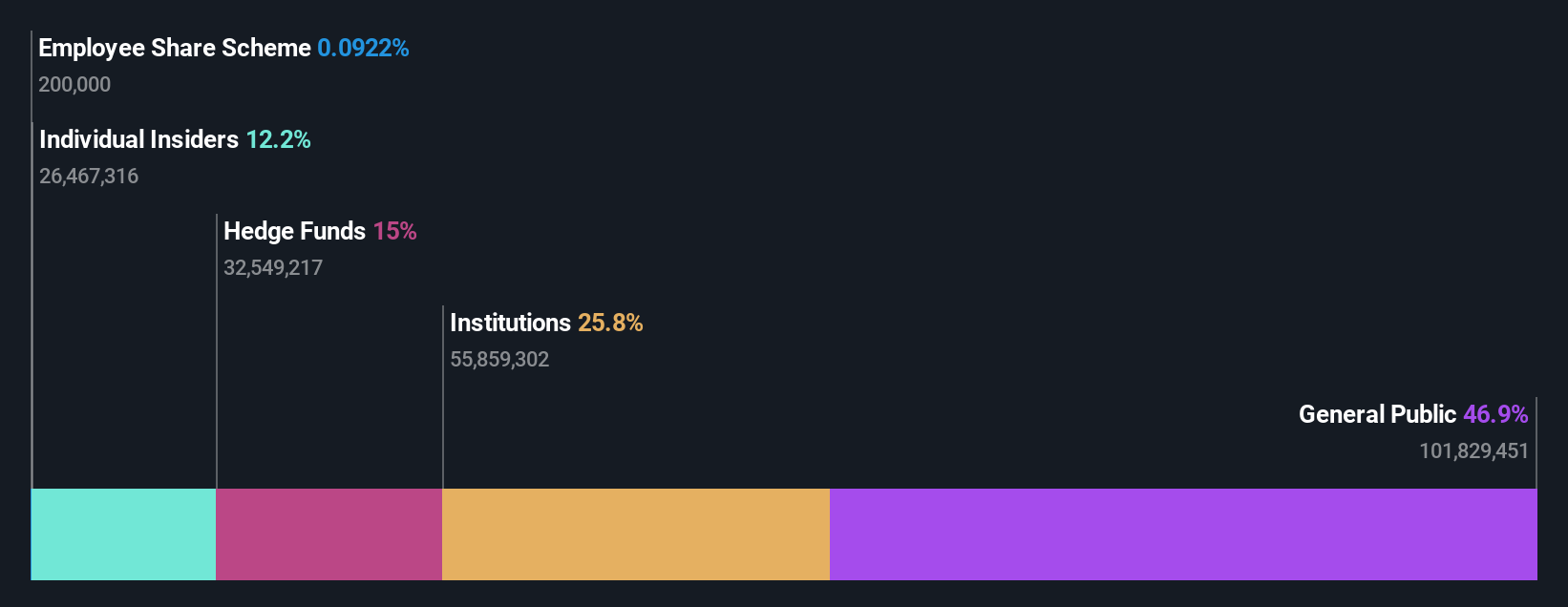

Insider Ownership: 12.6%

Gulf Keystone Petroleum’s earnings are expected to grow significantly at 24.92% annually, surpassing the UK market average of 11.4%. Trading at 88.2% below estimated fair value indicates potential upside, though recent insider activity shows substantial selling over the past quarter. Despite a forecasted high return on equity of 23.6%, earnings quality is impacted by large one-off items, and its dividend yield of 4.87% is not well-covered by earnings.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: RHI Magnesita N.V., along with its subsidiaries, specializes in the development, production, sale, installation, and maintenance of refractory products and systems for industrial high-temperature processes globally, with a market cap of £1.38 billion.

Operations: The company’s revenue is derived from several segments: €441 million from India, €80 million from Minerals, €727 million from Europe & CIS, €536 million from Latin America, €863 million from North America, €377 million from China & East Asia, and €342 million from the Middle East, Türkiye & Africa.

Insider Ownership: 11.8%

RHI Magnesita’s earnings are projected to grow significantly at 26.2% annually, outpacing the UK market average of 11.4%. Despite trading at 49.2% below its estimated fair value, the company faces challenges with high debt levels and a dividend yield of 5.42% that is not well-covered by earnings. Recent events include a final dividend declaration of €1.20 per share and appointing KPMG as their new auditor for 2026, reflecting ongoing corporate governance adjustments.

Where To Now?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment