Dividend Powerhouses with 3%+ yields can be especially appealing when inflation, interest rates and growth signals are all pulling investors in different directions. With central banks weighing rate paths, energy prices affecting inflation expectations and export trends shaping global supply chains, many investors are looking for income that does not rely solely on market optimism. This Dividend Powerhouses screener focuses on companies offering more than a 5% dividend yield that is described as well covered, growing and stable. In this article, you will see three stocks from the screener that fit this income focused theme.

Tokio Marine Holdings (TSE:8766)

Overview: Tokio Marine Holdings is a global insurer based in Tokyo that offers a wide range of non life and life insurance products, reinsurance, asset management, and risk solutions for individuals, businesses, and institutions across Japan and international markets.

Operations: Tokio Marine Holdings generates revenue primarily from International Insurance Business at ¥4.6t, Domestic Non Life Insurance Business at ¥3.8t, Domestic Life Insurance at ¥796.2b, and Solution and Other Business at ¥285.6b, partly offset by unallocated adjustments of ¥599.7b.

Market Cap: ¥12.8t

Tokio Marine Holdings stands out in an income focused screen because it combines a 3.58% dividend with active capital return plans, including a sizeable share buyback authorization, while still investing to reshape the business through its Re New initiative in Japan and expansion of disaster resilience solutions. Analysts expect only modest earnings growth and recent results include a large one off loss of ¥501.5b, so the stock carries execution risk around divesting equity holdings, managing international credit exposures and paying up for acquisitions. Even so, strong external credit ratings on key subsidiaries, planned governance upgrades and a valuation framework that flags the shares as trading well below an estimated fair value give investors several factors to consider beyond the headline yield.

Tokio Marine’s combination of a 3.58% dividend, share buybacks and a large one off loss raises a bigger question. See how the 4 key rewards and 1 important warning sign could reshape how you view the next chapter.

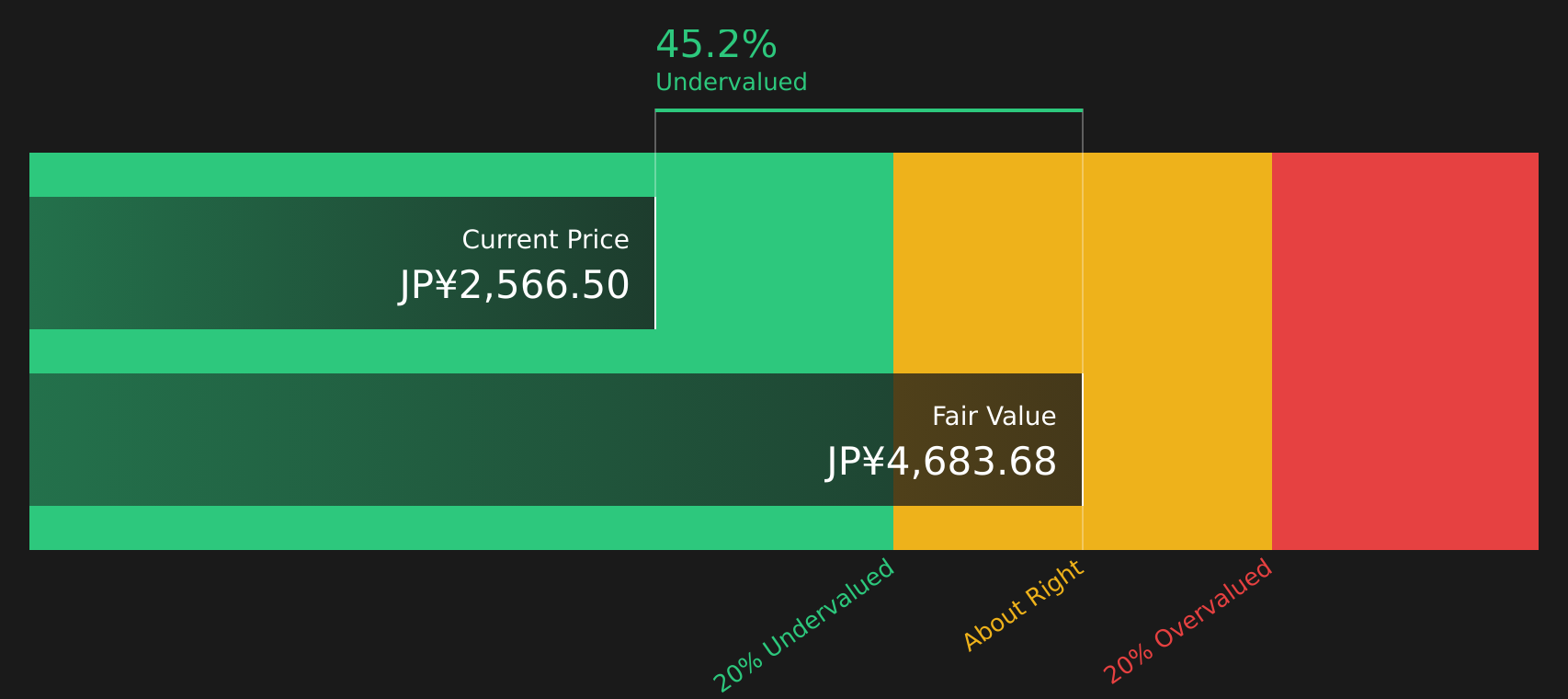

Daiichi Sankyo Company (TSE:4568)

Overview: Daiichi Sankyo Company is a Japan based pharmaceutical group focused on cancer and cardiovascular treatments, supplying prescription drugs such as Enhertu, Datroway, Lixiana and other specialty medicines across Japan, the US, Europe and other international markets.

Operations: Daiichi Sankyo Company generates all of its ¥2.1t revenue from Pharmaceutical Operations, with sales spread across Japan at ¥580.1b, the United States at ¥749.4b, Europe at ¥497.4b and other regions at ¥296.2b.

Market Cap: ¥4.7t

Daiichi Sankyo Company appears in a dividend screen because its 3.9% yield sits on top of a fast moving oncology and cardiometabolic franchise that is gaining fresh approvals, such as Vanflyta in China and new Datroway and Enhertu indications in the US and EU, plus a long list of AI and biomarker collaborations that could support its antibody drug conjugate pipeline. At the same time, earnings depend heavily on a few blockbuster cancer drugs, free cash flow is not yet comfortably covering dividends, and the company leans on external borrowing, so funding and payout risk are present. The stock is reported to be trading well below one estimated fair value and is supported by ongoing share buybacks, giving investors a combination of notable business drivers and areas of financial pressure to assess.

Cancer momentum at Daiichi Sankyo Company is accelerating, but the dividend and debt picture leaves key questions open. Put the analyst forecasts for Daiichi Sankyo Company in context and see what the current payout might be hiding.

Toyota Motor (TSE:7203)

Overview: Toyota Motor is a global auto manufacturer that designs, builds, and sells a full range of vehicles, from compact cars and SUVs to trucks and buses, as well as hybrid and battery electric models under the Toyota and Lexus brands, and also offers auto focused financial services and related businesses worldwide.

Operations: Toyota Motor generates most of its revenue from Automotive at ¥45,417,703m, alongside Financial Services at ¥4,857,115m and All Other at ¥1,651,412m, partly offset by inter segment eliminations of ¥1,241,278m.

Market Cap: ¥31,976.8b

Toyota Motor catches the eye of income focused investors because it pairs a 3.7% dividend yield with a broad electrification push, including hybrids, battery EVs and solid state battery research. It is also trading on a P/E below the Japanese market and Asian auto peers. At the same time, earnings and revenue growth expectations are modest, funding leans heavily on external borrowing, and dividends are not comfortably covered by free cash flow. The balance between payout, debt and future investment therefore deserves close attention. Recent news on production cuts linked to shipping routes, fresh capital spending in Texas and growing electrified lineups shows how much is in motion for this global manufacturer, but the full picture of what this could mean for future income and valuation is more complex than the headline yield suggests.

Toyota Motor’s 3.7% yield, electrification push and below market P/E suggest the story is not fully priced in, but the real twist may sit inside the analysis report for Toyota Motor

The three stocks covered here are only the starting point, with the full Dividend Powerhouses screen surfacing 478 more companies that combine 3%+ yields with equally compelling income stories through the Dividend Powerhouses (3%+ Yield) screener. Use Simply Wall St to identify and analyze the specific catalysts, dividend coverage, growth profiles and risk narratives that matter most to you so you can focus on the highest conviction ideas from that wider list.

Take Control of Your Investment Journey

If Tokio Marine Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Some of the sharpest breakouts start quietly, while momentum is still building and the best entries are slipping away under the radar for now. Consider getting in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Toyota Motor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment