With inflation readings, bond yields and trade headlines pulling markets in different directions, many investors are looking for steadier income from dividends rather than relying only on price swings. The Dividend Powerhouses (3%+ Yield) screener focuses on companies with dividend yields above 5% that are described as well covered, growing and stable, which can be appealing if you want cash flow that does not solely depend on short term market moves. In this article you will see three stocks from that screener that stand out for their income potential and disciplined approach to paying shareholders.

Lloyds Banking Group (LSE:LLOY)

Overview: Lloyds Banking Group is a UK focused financial group that provides everyday banking, lending, insurance, pensions and investment services to individuals and businesses through brands such as Lloyds Bank, Halifax, Bank of Scotland and Scottish Widows.

Market Cap: £65.13b

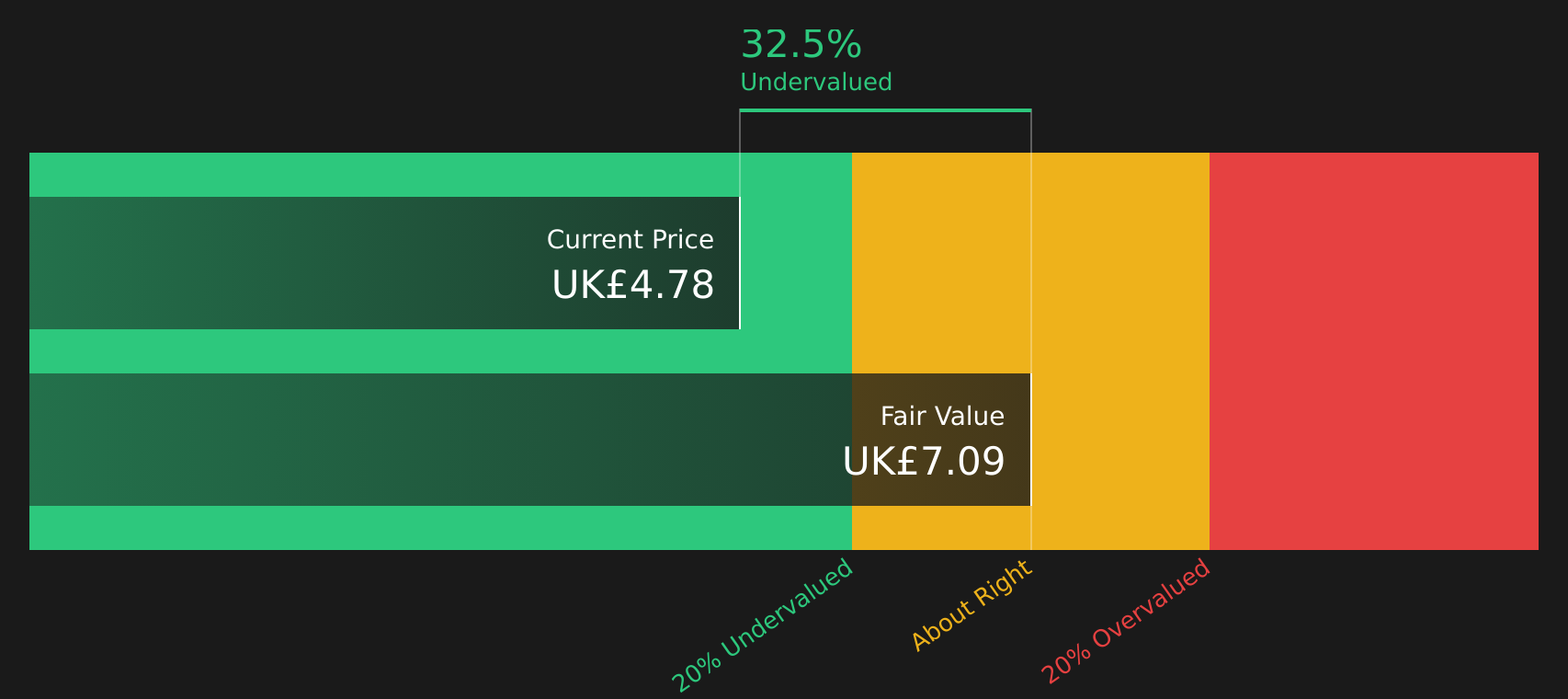

Lloyds Banking Group may interest income focused investors because it mixes a high dividend yield with a push into fee based areas like pensions and insurance. This is alongside heavy investment in digital banking and AI to keep costs in check. Earnings growth has recently been ahead of the wider UK market, net profit margins sit above 24%, and buybacks are shrinking the share count. Yet the stock trades at a deep discount to the Simply Wall St fair value estimate while analysts see only modest upside to their price target. The catch is the bank’s heavy exposure to the UK economy, an unstable dividend history and ongoing regulatory and credit risks, which means the real opportunity lies in how those strengths and vulnerabilities balance out over time.

Lloyds Banking Group’s mix of high yield, fee based growth and digital investment looks like a story the market has not fully joined the dots on yet. However, the real twist sits in the 3 key rewards and 2 important warning signs

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that runs infrastructure, renewable energy and private equity funds, giving institutional and retail investors access to real assets and sustainable investment strategies across the UK, Europe and Australia.

Operations: Foresight Group Holdings generates about £114.8 million from Real Assets and £50.1 million from Private Equity, with most revenue coming from the United Kingdom at £126.4 million and Australia at £25.7 million.

Market Cap: £519.10 million

Investors looking for dependable dividends backed by fee based cash flows may find Foresight Group Holdings interesting, because it combines earnings growth, high reported returns on equity and a focus on infrastructure and renewable assets where it currently has relatively low market shares. The company is expanding higher fee products, running share buybacks and reporting rising revenue and earnings. However, the stock trades below some estimates of fair value and analyst price targets. The other side of the story is its reliance on performance fees, external funding and policy support for renewables, which could make profits more sensitive to setbacks. The full picture sits in how those growth levers and risks stack up over time for income focused investors.

Foresight Group Holdings appears to be a pure play on fee based cash flows in real assets, yet the real story may be how future earnings could track those assets. Get the analyst forecasts for Foresight Group Holdings to see what might be missing.

3i Group (LSE:III)

Overview: 3i Group is a London based private equity and infrastructure investor that backs mature, cash generating businesses in sectors such as consumer, healthcare, industrials and software, and also finances long life assets like utilities and transport. It typically takes control or influential stakes, using both its own balance sheet and third party capital to drive returns and support dividends.

Operations: 3i Group generates most of its revenue from Private Equity at about £5.3b, with additional contributions from Infrastructure of £193m, Scandlines of £55m and £32m of unallocated IFRS adjustments.

Market Cap: £26.72b

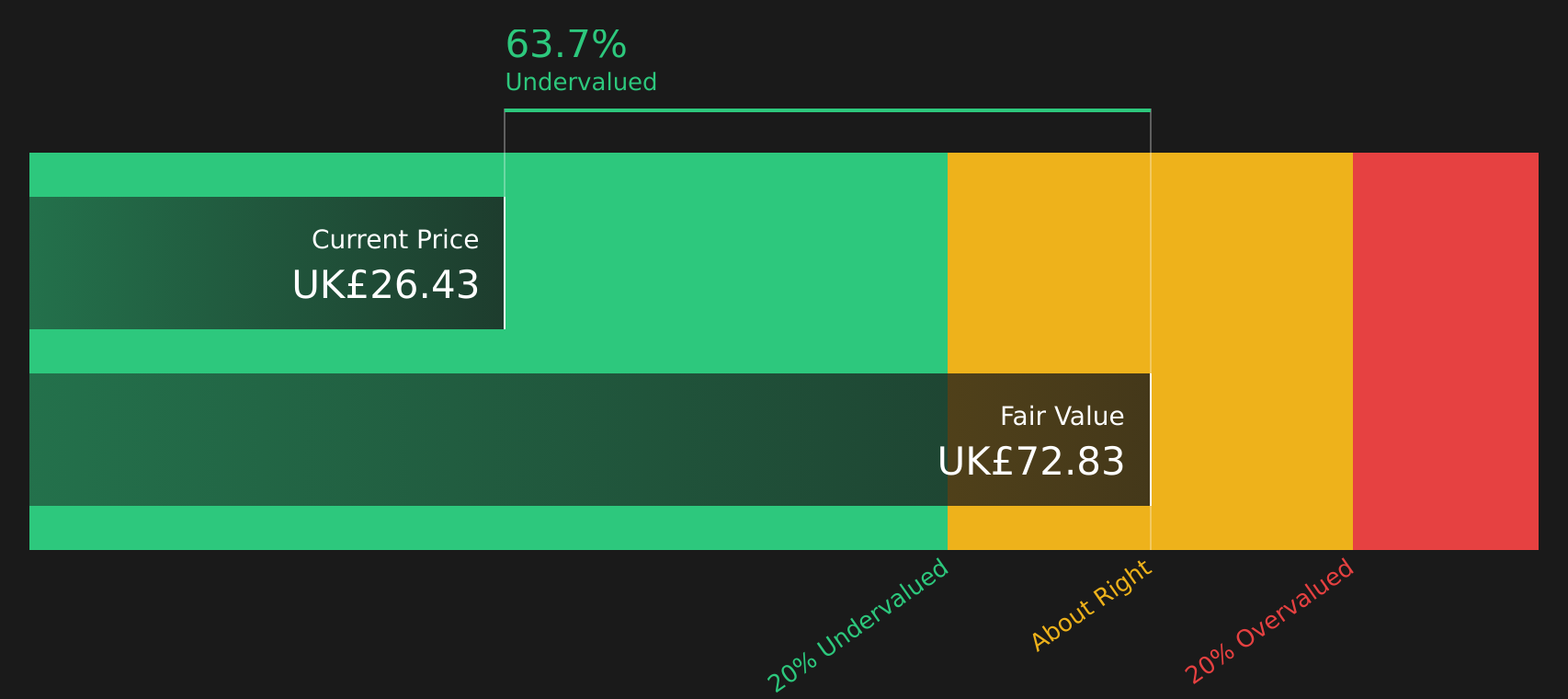

3i Group attracts attention in a dividend focused screen because it couples a 3.2% yield with exposure to private equity and infrastructure assets that have recently supported net income of £5,294m and very high profit margins. The stock trades on a low P/E and at a large discount to one fair value estimate, yet analysts still debate what its portfolio is worth. This can create opportunity for investors who do their homework on assets like Action and the infrastructure arm. At the same time, 100% reliance on external borrowing, currency swings and sector pressure in areas such as automotive mean the funding structure carries more risk than a traditional bank or insurer. Understanding where the real cushion sits is crucial for income seekers.

3i Group’s low P/E and hefty reported margins hint that its share price may not fully reflect the story behind assets like Action and infrastructure. Get the analysis report for 3i Group to see what might be hiding in plain sight.

The three dividend ideas in this article are only a starting point, and the full Dividend Powerhouses (3%+ Yield) screen has uncovered 43 more companies with income profiles and narratives that could be just as compelling as the ones you have seen. Identify your own highest conviction dividend plays by using Simply Wall St to analyze the Dividend Powerhouses (3%+ Yield) screener and filter for the exact catalysts, risk profiles and narrative angles that matter most to your portfolio.

Take Control of Your Investment Journey

If 3i Group or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves?

Fresh breakouts, fast shifting momentum and under the radar ideas rarely stay quiet for long, and the best entry points can pass quickly, so act now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment