As the Asian markets navigate a complex landscape of changing monetary policies and geopolitical developments, investors are closely watching the technology sector, which continues to show potential for high growth amidst these dynamics. In this environment, stocks that demonstrate strong fundamentals, innovative capabilities, and resilience to macroeconomic shifts may stand out as attractive opportunities in the tech space.

Top 10 High Growth Tech Companies In Asia

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Shengyi Electronics | 27.53% | 32.56% | ★★★★★★ |

| Gold Circuit Electronics | 36.81% | 38.20% | ★★★★★★ |

| Fositek | 29.08% | 37.44% | ★★★★★★ |

| Zhongji Innolight | 44.23% | 46.41% | ★★★★★★ |

| Mobvista | 22.88% | 41.07% | ★★★★★★ |

| Suzhou TFC Optical Communication | 39.49% | 37.87% | ★★★★★★ |

| Unimicron Technology | 29.19% | 56.13% | ★★★★★★ |

| Park Systems | 21.21% | 36.99% | ★★★★★★ |

| PharmaEssentia | 32.48% | 46.29% | ★★★★★★ |

| CARsgen Therapeutics Holdings | 63.94% | 80.57% | ★★★★★★ |

Here’s a peek at a few of the choices from the screener.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Siglent Technologies Ltd. engages in the research, development, production, sale, and servicing of electronic test and measurement equipment both in China and globally, with a market capitalization of CN¥11.80 billion.

Operations: Siglent Technologies focuses on the electronic test and measurement equipment sector, serving both domestic and international markets. The company leverages its expertise in research, development, production, sales, and servicing to generate revenue.

Siglent Technologies CO.,Ltd. has demonstrated robust growth dynamics, with its revenue climbing to CNY 161.92 million in Q1 2026 from CNY 131.81 million the previous year, marking a notable increase. Despite a slight dip in net income from CNY 40.69 million to CNY 38.34 million, the company’s earnings trajectory remains promising with an expected annual growth of approximately 23.93%. This performance outpaces the broader Chinese market’s forecasted earnings growth of 27.6% and is further complemented by a revenue surge projected at an annual rate of 22.1%, surpassing the market average of 17.1%. Siglent’s commitment to innovation and market expansion is evident in these figures, positioning it well within Asia’s high-growth tech landscape despite its highly volatile share price recently.

Simply Wall St Growth Rating: ★★★★☆☆

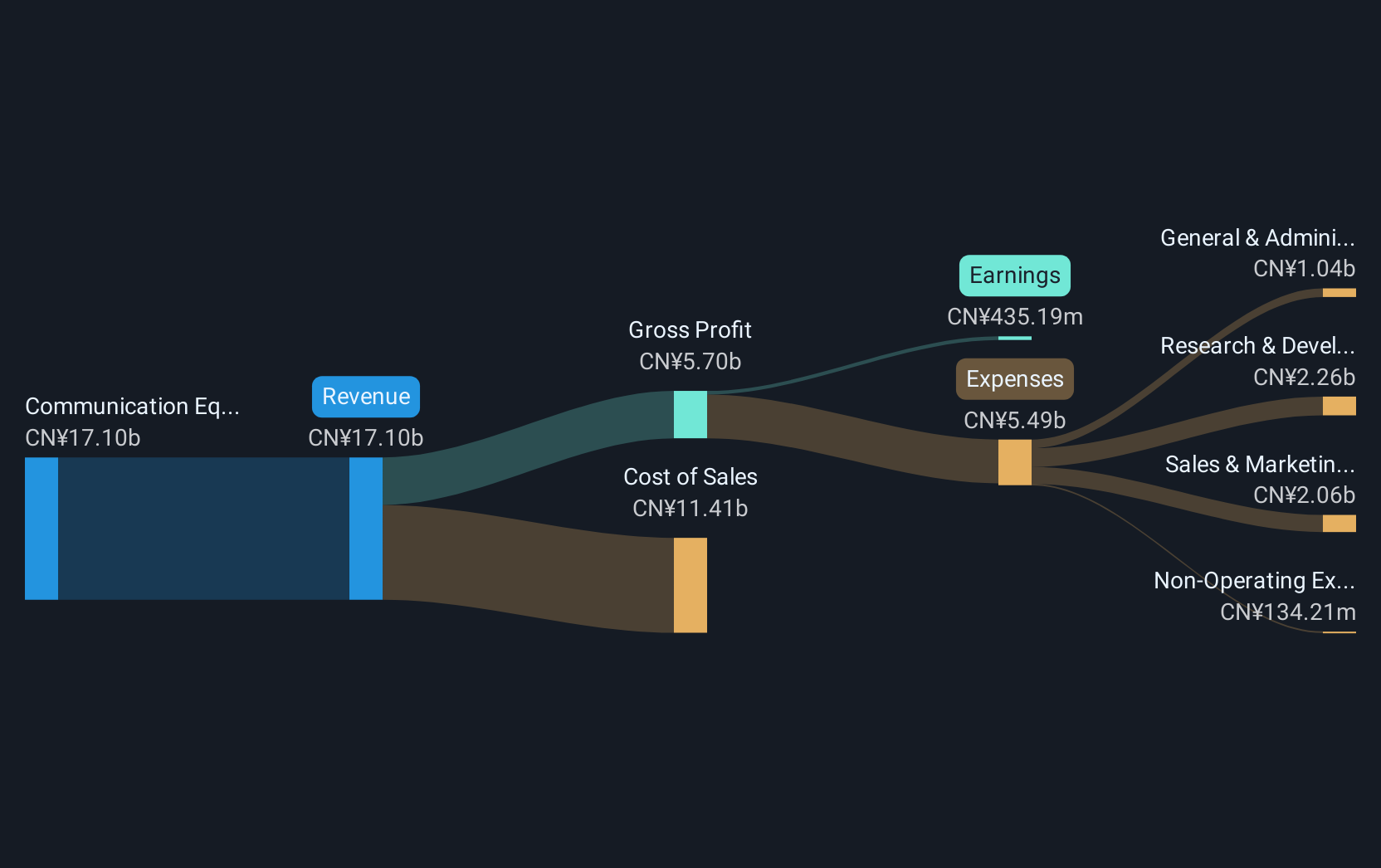

Overview: Fujian Star-net Communication Co., LTD. is involved in providing ICT infrastructure and AI application solutions within China, with a market cap of approximately CN¥14.15 billion.

Operations: The company generates revenue primarily from its Communication Equipment Manufacturing segment, which contributed CN¥19.58 billion.

Fujian Star-net Communication Co., LTD. has shown resilience and adaptability in a competitive market, with its revenue reaching CNY 3.9 billion in Q1 2026, up from CNY 3.5 billion the previous year. Despite a slight decrease in net income from CNY 42.12 million to CNY 37.23 million, the firm’s commitment to innovation is evident through its robust R&D spending which aligns with its strategic focus on enhancing technological capabilities and expanding market reach. The company also sustains shareholder value through consistent dividends, as evidenced by the recent payout of CNY 2.50 per 10 shares and an annual dividend of CNY 0.25 per share, reinforcing its financial stability amidst evolving industry dynamics.

Simply Wall St Growth Rating: ★★★★★☆

Overview: SanBio Company Limited focuses on developing, producing, and selling regenerative cell medicines for the central nervous system with a market cap of ¥77.36 billion.

Operations: The company specializes in regenerative cell medicines targeting the central nervous system. The market cap stands at ¥77.36 billion, reflecting its position in the biotechnology sector.

SanBio’s recent advancements underscore its potential in the biotech sector, particularly with the NHI-listed AKUUGO for traumatic brain injury, priced at JPY 72.7 million. Despite a net loss reduction to JPY 836.04 million from JPY 1.53 billion year-over-year and an earnings forecast indicating a shift towards profitability within three years, challenges remain due to its highly volatile share price and minimal revenue generation under USD$1m annually. The firm’s commitment is evident in its strategic R&D focus, which is crucial for transitioning from current losses towards future profitability and expanding into new medical markets like ischemic stroke treatment.

Turning Ideas Into Actions

Curious About Other Options?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment