As global markets navigate a complex landscape marked by monetary policy shifts and geopolitical developments, Asia’s economic resilience continues to capture investor attention. In this context, growth companies with high insider ownership present intriguing opportunities, as they often signal strong internal confidence and alignment with shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.9% | 31.5% |

| Shanghai Biren Technology (SEHK:6082) | 11% | 120.7% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 106.4% |

| Meitu (SEHK:1357) | 22.8% | 31.5% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.3% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.6% |

| Great Microwave Technology (SHSE:688270) | 21.1% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.2% | 38.2% |

| Fulin Precision (SZSE:300432) | 10.4% | 60.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

Let’s uncover some gems from our specialized screener.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Rigol Technologies Co., Ltd. is involved in the research, development, manufacturing, and sale of electronic testing and measuring instruments and accessories both in China and internationally, with a market cap of CN¥15.22 billion.

Operations: The company’s revenue is primarily derived from its electronic test and measurement instruments segment, which generated CN¥964 million.

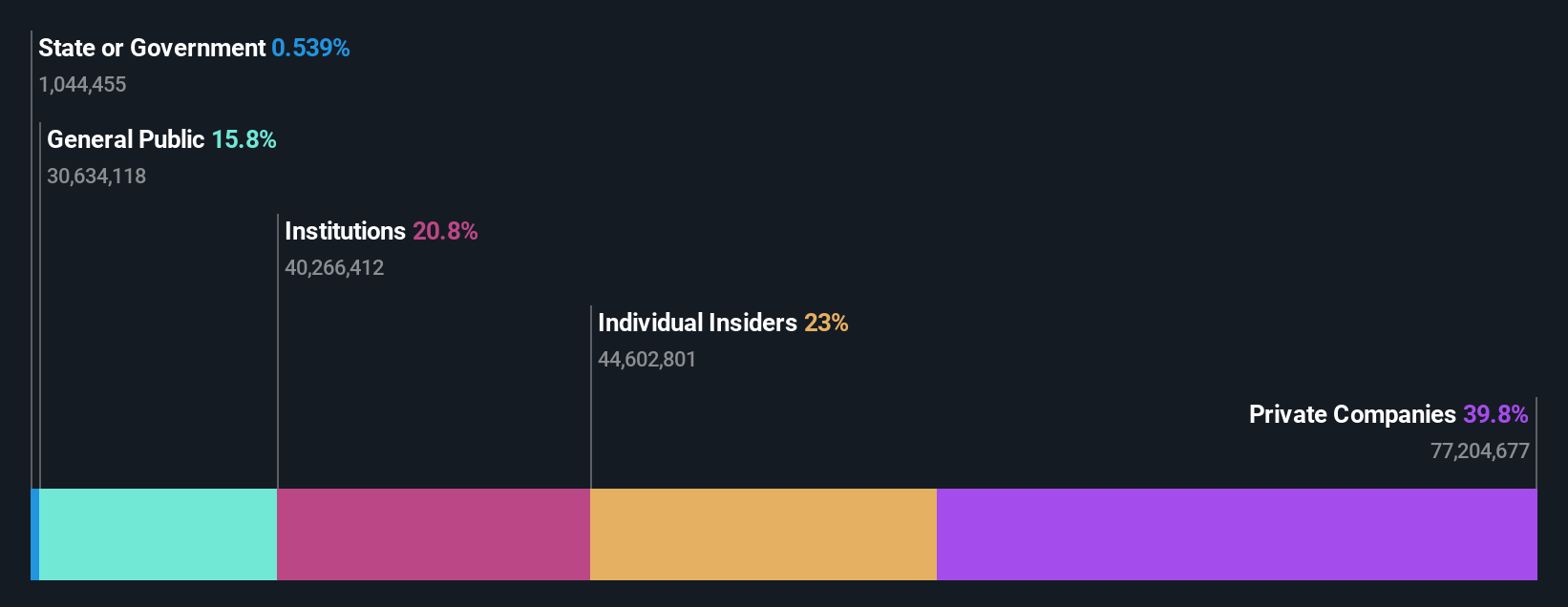

Insider Ownership: 23.8%

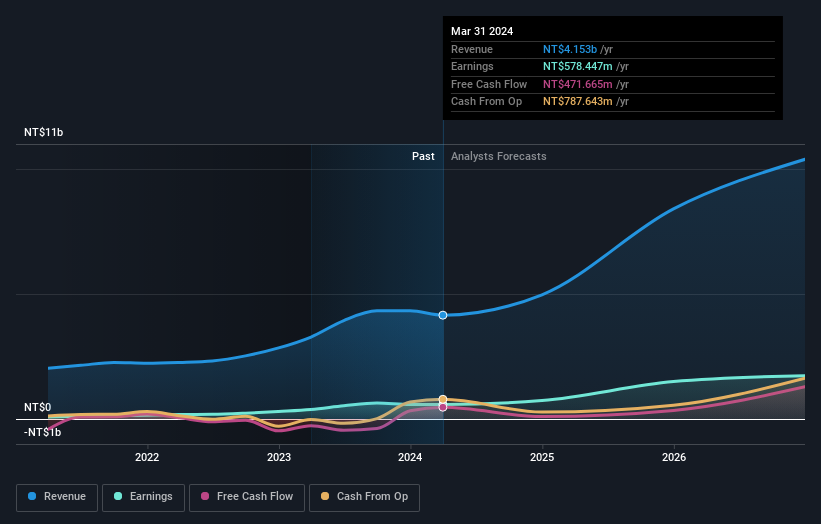

Rigol Technologies has demonstrated strong growth with Q1 2026 revenue reaching CNY 231.56 million, a significant increase from last year. Earnings are forecast to grow at an impressive 30% annually over the next three years, outpacing the Chinese market’s average. Despite high volatility in its share price and a low forecasted return on equity of 6.5%, insider ownership remains substantial, aligning management interests with shareholders and supporting long-term growth prospects in Asia.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Nantong Jianghai Capacitor Co. Ltd. engages in the research, development, production, and sale of capacitors and related materials and instruments both in China and internationally, with a market cap of CN¥90.99 billion.

Operations: Nantong Jianghai Capacitor’s revenue is derived from its activities in researching, developing, producing, and selling capacitors along with related materials and instruments across domestic and international markets.

Insider Ownership: 15.1%

Nantong Jianghai Capacitor’s earnings are projected to grow significantly at 24.8% annually, although slightly below the Chinese market’s 27.7%. Revenue growth is expected to outpace the market at 19.4% annually. Despite recent share price volatility, insider ownership remains high, aligning management with shareholders’ interests. Recent Q1 results showed an increase in sales and net income compared to last year, supporting its growth trajectory in Asia despite slower-than-market profit expansion forecasts.

Simply Wall St Growth Rating: ★★★★★★

Overview: Kaori Heat Treatment Co., Ltd. specializes in the research, development, manufacture, and sale of heat exchanger and thermal energy products across Taiwan, Asia, the United States, Europe, and internationally with a market cap of NT$147.69 billion.

Operations: The company’s revenue segments include NT$1.82 billion from Plate Heat Exchangers and NT$7.17 billion from fuel, electricity, and thermal energy products.

Insider Ownership: 10.7%

Kaori Heat Treatment exhibits strong growth potential with earnings projected to rise significantly at 56.5% annually, outpacing the Taiwanese market’s 26.3%. Revenue is also expected to grow robustly at 50.4% per year. Recent Q1 results highlighted substantial sales and net income increases, suggesting a positive trajectory despite share price volatility. High insider ownership may align management interests with shareholders, although recent insider trading data is unavailable, indicating stable internal confidence in its growth prospects.

Turning Ideas Into Actions

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we’re here to simplify it.

Discover if Kaori Heat Treatment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment