Although there is no doubt that brands, IP and intangible assets are valuable, measuring and reporting the specific value of brand assets presents challenges and opportunities for both business executives and valuation analysts. While the difference between a company’s total market value and the value of assets reported on its balance sheet is easy to identify, identifying the value of the brand assets that contribute to the observable gap can be more challenging.

Understanding the value of brand assets can support and inform strategic decisions, resolve internal and legal disputes, guide restructuring and reorganisation efforts, and identify opportunities to optimise revenues and profits. However, reasonable valuation requires definition of the brand assets used by the company and quantification of the financial benefits and contributions that they provide to each revenue-generating activity undertaken by the company. While brand valuation analysis can appear daunting, the analytical process provides useful information beyond numerical value.

Brands contribute to value, but measuring their contribution can be challenging

For most businesses, their market value exceeds the value of their tangible assets. We reviewed 139 middle market, publicly traded companies in the United States to measure the gap between their total market value and the value of assets reported on their balance sheets. We calculated this ‘value gap ratio’ as total enterprise value minus book value of identified assets divided by enterprise value.

For the companies reviewed, the average value gap ratio was 66 per cent. Thus, 66 per cent of total enterprise value consists of unidentified assets, or assets not reported on the company’s balance sheet. While the observed value gap ratio is likely due to the value of internally developed brands, technology assets and other proprietary IP, financial reports do not typically identify or value the types of intangible assets or IP contributing to the difference between market value and the value of identified assets. Depending on the business, the value gap could comprise patents, trade secrets, brands, trade secrets, copyrights, proprietary data or a combination of these assets.

Brands are often developed internally and over time rather than acquired. The value of such internally developed proprietary assets is not typically identified or reported in company financial reports or public disclosures – leaving managers, executives and stakeholders with little information to understand what assets are contributing to the value gap. The International Trademark Association (INTA) recently issued a board resolution stating that ‘accounting standards should not require a blanket exclusion of trademarks and complementary IP that are developed in-house from recognition as assets on corporate balance sheets’. There is growing interest in the contribution of brand assets and other internally developed IP assets to a company’s market value.

Brand valuation can help quantify and address a portion of the value gap. Determining the value of brand assets separate from the market value of all intangible assets requires a brand valuation analysis. For companies wanting to understand the value of their brand assets relative to their market value and the value of other intangible assets, valuation should be determined based on the contribution to financial performance provided by the brand assets. Brand assets can contribute to financial performance through a combination of:

- the ability to achieve higher prices for their products and services;

- the achievement of greater volume of products sold or services provided;

- a reduction of advertising and marketing costs and the ability to introduce new products with lower market entry expenses; and

- in some cases, receipt of income from licensees or franchisees.

Companies that leverage their brand assets to achieve some or all of these benefits own valuable brands. Companies that are unable to leverage their brand assets to achieve observable financial benefits own undervalued brands. In other words, brands create value if they can be used to create financial benefits. While other valuation approaches (e.g., the cost approach or market approach) can provide useful valuation indications in some contexts, an income approach focused on measuring the portion of forecast financial benefits expected to be contributed by the company’s brands assets typically provides a more informative indication of brand value for companies using their brand assets to enhance financial performance. Measuring brand value using an income approach helps companies understand the portion of the value gap provided by their brand assets and quantifies how brand assets can be further leveraged to further enhance financial performance and overall company value.

However, using an income approach to measure brand value presents some analytical challenges. A company’s ‘brand’ will likely include a bundle of legal rights, IP and proprietary assets, and different companies may rely on different bundles of assets to obtain the benefits of using their brand. As companies constitute and use their brands in many ways and most brand assets are not bought or sold, each set of assets is unique, and valuation benchmarks for these are unlikely to exist. Further, standard accounting and financial reporting practices do not indicate the amount of profit earned from the use of IP or brand assets. Profits are reported for the entire business and not apportioned to the different types of assets and resources used by the business to generate its profits. Despite these challenges, reasonable brand valuation is possible, and completion of a brand valuation analysis is likely to inform key strategic decisions and uncover opportunities to improve financial performance and total company value. In other words, despite its inherent challenges, brand valuation is a valuable analytical tool.

Brand valuation analysis

For businesses achieving a contribution to financial performance from their brand assets, some portion of the value gap can be apportioned to the value of the company’s brand assets. However, determining a reasonable valuation of its specific bundle of assets requires:

- identifying and defining the brand assets owned and used by the company, as well as its other tangible and intangible asset groups;

- identifying and defining the revenue-generating business activities undertaken by the company;

- quantifying and forecasting the financial contribution provided by the brand assets to each defined revenue-generating business activity; and

- developing a valuation for the financial contribution provided by the brand assets to the company’s overall operations.

While brand valuation analysis appears relatively complex, the analytical process provides a lot of information that is useful to business managers, investors and stakeholders.

The first step requires identifying and defining the company’s brand assets. What constitutes brand assets will vary from business to business depending on the activities the organisation undertakes to establish and maintain its reputation. A company’s brand assets might include:

- registered marks and unregistered trade names, logos and slogans;

- copyrights for logos and website content, as well as marketing and promotional content;

- the corporate trade name and any product names, logos or slogans;

- website domain names and social media pages;

- business processes relating to marketing, customer relationships and loyalty programmes; and

- data relating to customer interactions and preferences.

Some of these assets are protected as IP and some are not. Some combination of these assets is used to maintain and build reputation and awareness with customers, suppliers, partners and stakeholders. By building reputation and awareness, the company can utilise its brand assets to achieve stronger financial results.

Benefits of undertaking the process of defining, identifying and grouping brands assets include identification and organisation of the company’s trademark registrations, matching of trademark registrations to other brand assets, identification of holes or gaps in IP protection strategies and identification of unused (and potentially saleable) brand assets.

The second and third steps in determining the value of a company’s brand assets are quantifying the financial contribution provided by the brand assets to each revenue-generating activity undertaken by the company. A business’s revenue-generating activities are those activities that provide revenue or income. This can include the sale of products, offering of services or licensing of proprietary assets. For a company that sells a portfolio of products or services, the brand assets may contribute differently to revenue, profit and cash flow for each different activity. Most organisations will measure and monitor revenue and some measures of profitability for each of their different business activities. Obtaining and analysing activity-specific performance data is a key step in brand valuation and often an informative exercise for business managers, executives and stakeholders. Review of data comparing financial performance across different business activities often uncovers strategic opportunities.

After analysing activity-specific performance data, the valuation analysis needs to quantify the contribution to revenues, profits and cash flows provided by the brand assets to each activity. This process is often referred to as profit apportionment and involves converting data and observations about the drivers of demand, marketing activities, company strategy and financial performance to a measure of the percentage of profit achieved at each of the company’s revenue-generating activities.

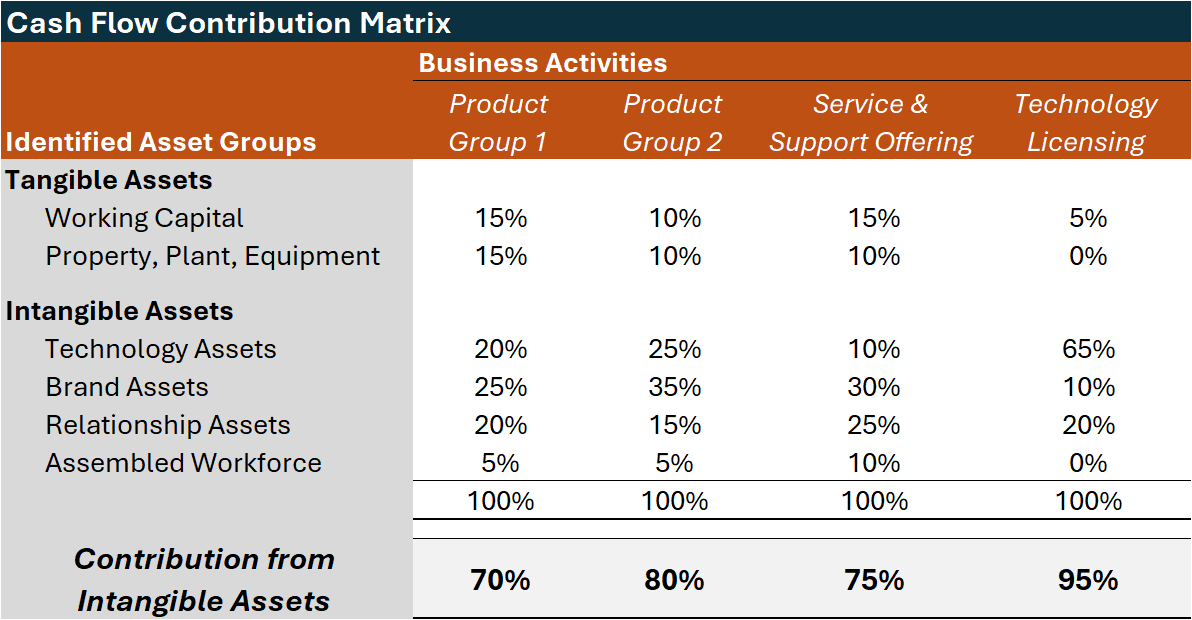

Completion of the profit apportionment analysis typically results in a matrix of the company’s asset groups and revenue-generating activities.

Figure 1. Cash flow contribution matrix

The percentages indicate the portion of cash flows from each activity contributed by each asset type. After determining the profit apportionment percentages, the value of any asset group, including the brand assets, is determined by applying the apportionment percentage to forecast cash flows from each business activity.

Brand valuation is not just a static measure of a bundle of brand assets’ contribution to financial performance as at a specific point in time; the valuation analysis and results should identify strategic opportunities, inform resource allocation and support opportunities to increase overall company cash flow, profitability and value. The brand valuation analysis creates a metric that can be reported to shareholders and stakeholders.

Returning to our review of public middle market companies, comparing the companies by industry group indicates that companies with larger value gap ratios often have stronger financial ratios.

Of the 139 companies that met our middle market screening criteria, we analysed:

- 10 companies developing and providing products or services focused on consumers;

- 34 companies developing and providing healthcare products or services;

- 21 companies developing and providing products for industrial customers; and

- 46 companies developing and providing information technology services.

Across the sector groups:

- companies in the consumer sector with the highest value gap ratios had higher revenue growth and a higher ratio of earnings before interest, taxes, depreciation and amortisation (EBITDA) to total assets;

- companies in the healthcare sector with the highest value gap ratios had higher revenue growth and a larger increase in gross profit;

- companies in the industrials sector with the highest value gap ratios had higher gross profit margins, a larger increase in gross profit and higher EBITDA margins; and

- companies in the IT sector with the highest value gap ratios had higher gross profit margins and higher ratios of EBITDA to total assets.

The ratio of EBITDA to total assets and EBITDA margin are indications of operating efficiency (i.e., these companies are earning more profit with fewer tangible assets). The gross profit margin, or the ratio of gross profit to revenue, is an indication of the company’s ability to charge higher prices for its products and services. Both of these ratios are often a result of leveraging strong brand assets to achieve greater financial performance.

As expected, organisations with larger value gap ratios had achieved more growth, and were more efficient and profitable. The correlation between stronger financial ratios and higher valuations is expected but not easy to achieve. Again, brand valuation analyses can provide a baseline to measure and compare the impact of performance-enhancing strategies and a tool to uncover opportunities to improve financial performance and overall company valuation. The act of identifying and measuring should be used to review, critique and improve business performance.

The value of internally generated brand assets is not often reported on company financial reports and public disclosures. Managers and stakeholders often have little visibility into the financial contribution and value of specific groups of intangible assets, including their brand assets. Current accounting, financial reporting standards and tax codes discourage capitalisation of marketing expenses and brand development investments. Therefore, internally developed brand assets are not reported as an asset on company balance sheets. Increasingly, brand owner organisations and financial reporting standards organisations are exploring mechanisms for companies to provide greater transparency regarding the financial contribution and value of internally developed IP, intangible assets and brand assets.

As brand assets can provide a large portion of the value gap ratio and companies may benefit from provision of more information about their more valuable assets, brand valuations may be beneficial for companies and their stakeholders. A supplementary disclosure of the metrics and analysis used to develop a valuation of the company’s brand assets could help close the gap between market value and the value of tangible assets, provide greater transparency into the company’s efforts to build valuable brand assets, and assist managers and executives in identifying and executing strategies to leverage their brand assets to increase financial performance and overall business valuations.

Brand valuation is not just a measurement; it creates a metric that can be reported to shareholders and stakeholders. The results could be reported on the balance sheet or in supplementary financial reports. Either way, transparent valuation of internally generated assets communicates the company’s ability to convert capital to assets that will generate financial returns in the future and differentiate it from comparable businesses unwilling or unable to share the same information about their intangible assets.

Therefore, a brand valuation analysis adds value in multiple ways. While the analysis incorporates some complex valuation concepts and typically requires collection, organisation and review of data from across the organisation, the exercise provides a strategic tool to identify valuable business opportunities and information to close the market value gap and differentiate those companies that can develop and leverage brand assets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment