As global markets navigate a complex landscape marked by steady interest rates in the U.S. and a significant rate hike by Japan’s central bank, investors are keenly observing the performance of Asian dividend stocks amid these shifting economic conditions. In such an environment, dividend stocks that demonstrate resilience and consistent payout histories can be attractive for those seeking income stability alongside potential capital appreciation.

Top 10 Dividend Stocks In Asia

| Name | Dividend Yield | Dividend Rating |

| Toukei Computer (TSE:4746) | 4.07% | ★★★★★★ |

| OUG Holdings (TSE:8041) | 4.13% | ★★★★★★ |

| NCD (TSE:4783) | 5.16% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 6.15% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 4.40% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.16% | ★★★★★★ |

| CREEK & RIVER (TSE:4763) | 3.92% | ★★★★★★ |

| Changjiang Publishing & MediaLtd (SHSE:600757) | 5.37% | ★★★★★★ |

| Business Brain Showa-Ota (TSE:9658) | 4.73% | ★★★★★★ |

| Binggrae (KOSE:A005180) | 5.02% | ★★★★★★ |

Click here to see the full list of 1058 stocks from our Top Asian Dividend Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Mitsubishi Steel Mfg. Co., Ltd. is a company involved in the manufacturing and sale of steel products, construction machinery parts, automotive parts, and machinery and equipment, with a market cap of approximately ¥35.25 billion.

Operations: Mitsubishi Steel Mfg. Co., Ltd.’s revenue segments include Spring at ¥76.20 billion, Special Steel at ¥64.91 billion, Machinery at ¥11.77 billion, and Formed & Fabricated Products at ¥9.83 billion.

Dividend Yield: 4.5%

Mitsubishi Steel Mfg. has shown a 29.3% earnings growth over the past year, supporting its dividend sustainability with a payout ratio of 40.1% and a cash payout ratio of 24.3%. Despite being in the top 25% for dividend yield in Japan at 4.46%, its dividends have been volatile and unreliable over the past decade, reflecting an unstable track record despite adequate earnings coverage. The company trades significantly below estimated fair value, though it carries high debt levels.

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Nikko Co., Ltd. manufactures and sells asphalt mixing and concrete batching plants in Asia, with a market cap of ¥35.22 billion.

Operations: Nikko Co., Ltd.’s revenue is primarily derived from its Asphalt Plant Related Business at ¥19.33 billion, Concrete Plant Related Business at ¥14.36 billion, Environment and Transportation Related Business at ¥4.38 billion, Manufacturing Contract Related Business at ¥3.34 billion, and Crusher-Related Business at ¥2.45 billion.

Dividend Yield: 3.7%

Nikko Co., Ltd.’s recent earnings report shows a net income increase to ¥2.54 billion, supporting its dividend payout with a reasonable 70.7% earnings coverage ratio, yet the high cash payout ratio of 222.8% raises concerns about sustainability from free cash flows. While dividends have been stable and reliable over the past decade, yielding 3.72%, they fall short of Japan’s top tier yields and are not well covered by cash flows despite solid profit growth and a competitive P/E ratio of 13.9x.

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Marubun Corporation distributes electronics products both in Japan and internationally, with a market cap of ¥45.72 billion.

Operations: Marubun Corporation’s revenue is primarily derived from its Electronic Device Business, which accounts for ¥152.33 billion, and its Electronic System Business, contributing ¥59.32 billion, with an additional ¥2.58 billion coming from the Entrepreneur Business segment.

Dividend Yield: 4.4%

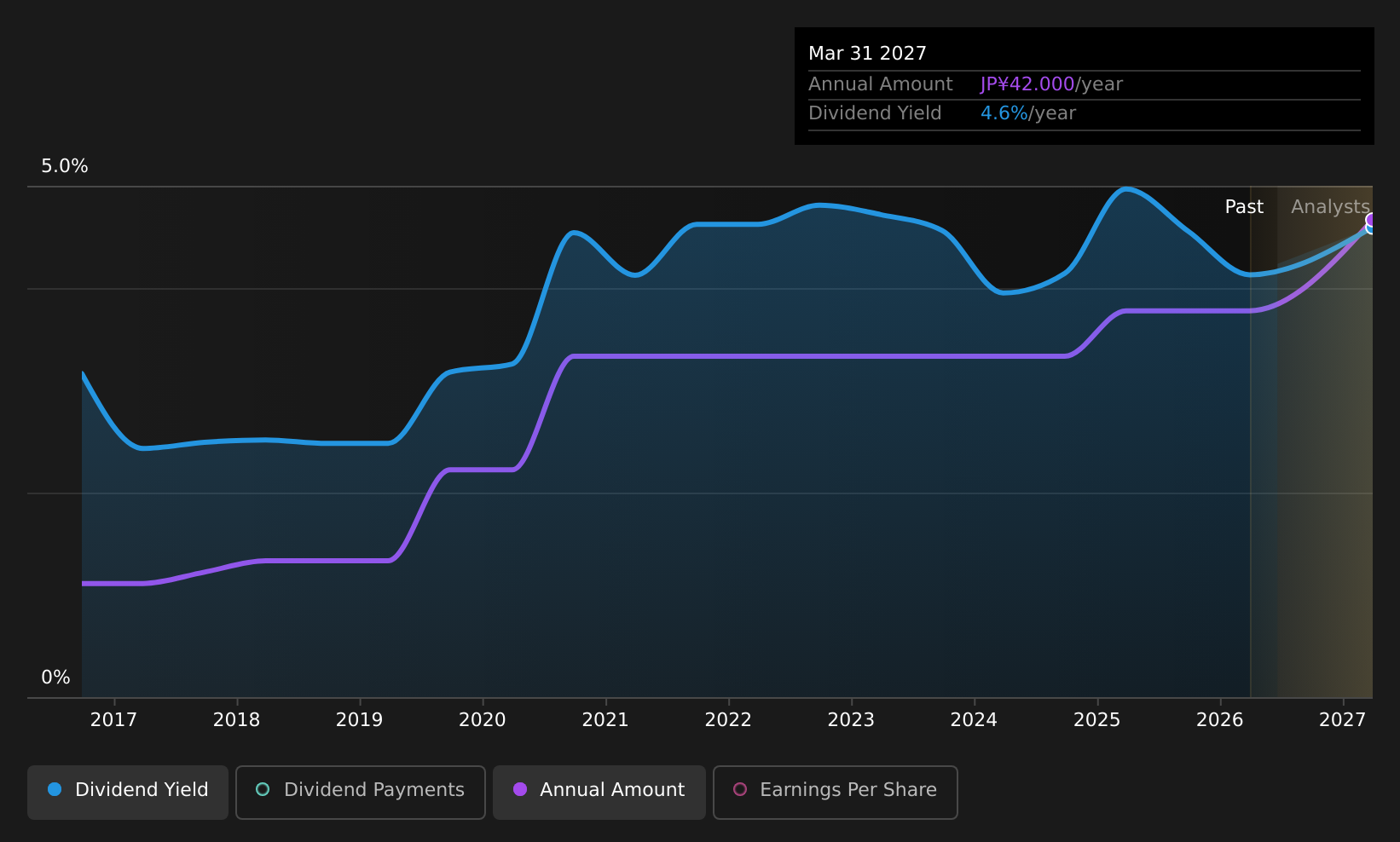

Marubun Corporation’s dividend outlook is mixed. Recent guidance suggests a significant increase in dividends for fiscal 2027, with year-end payments rising to ¥39 per share from ¥25 a year ago. Despite past volatility, the company’s revised policy aims for higher payout ratios, targeting a 50% earnings payout or 3.5% DOE. Dividends are well-covered by both earnings and cash flows, supported by a low payout ratio of 39.7%. However, its share price remains highly volatile.

Turning Ideas Into Actions

Seeking Other Investments?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Nikko might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment