Over the last two decades, financial services has seen a steady increase in new challengers like Monzo, Revolut and Lemonade. These new entrants have changed the competitive landscape by shifting customer demands, driving product innovation and moving with increased agility.

Amplified by COVID-19 restrictions, empty office buildings and new WFH norms, surging technology valuations have begged us to ask fundamental questions about how we define and create value in our businesses and how we deploy capital to optimise returns.

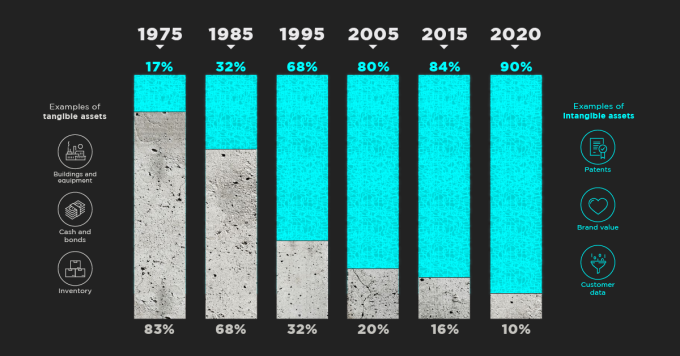

Looking at key differences, incumbents have a larger proportion of capital and resources tied up to maintaining assets (e.g. rent of a large head office or opex/capex to maintain legacy systems), whereas challengers, whether by design or by necessity, have adopted lighter and smarter assets, and freed up capital to change and grow their business. (see Figure 1).

Assets that were deemed strategic in the past have lost their value and new assets have emerged as a source of competitive advantage.

As part of our research, we looked at three different categories of assets (work, workforce and workplace) and compared the different configuration choices between incumbent and challenger banks and insurers, as well as the associated financial impact of such choices. We also surveyed financial services organisations in five major APAC financial centres to understand how they are enhancing their operating models in response to market changes as well as the differences between the five centres.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment