The Australian stock market is experiencing a mixed phase, with recent gains followed by profit-taking as geopolitical tensions create uncertainty. Amidst this backdrop, growth companies with high insider ownership can be attractive due to the confidence insiders demonstrate in their businesses.

|

Name |

Insider Ownership |

Earnings Growth |

|

Torque Metals (ASX:TOR) |

18.6% |

94.2% |

|

Magnetic Resources (ASX:MAU) |

33.6% |

124.2% |

|

Image Resources (ASX:IMA) |

20.4% |

148.6% |

|

Forrestania Resources (ASX:FRS) |

32.6% |

102.3% |

|

Fenix Resources (ASX:FEX) |

18.3% |

64.7% |

|

Echo IQ (ASX:EIQ) |

19.6% |

109.4% |

|

Cyclopharm (ASX:CYC) |

10.1% |

117.1% |

|

Clinuvel Pharmaceuticals (ASX:CUV) |

10.3% |

27.1% |

|

Austral Resources Australia (ASX:AR1) |

16.7% |

38.8% |

|

Adveritas (ASX:AV1) |

17.9% |

109.9% |

Let’s dive into some prime choices out of the screener.

Simply Wall St Growth Rating: ★★★★★☆

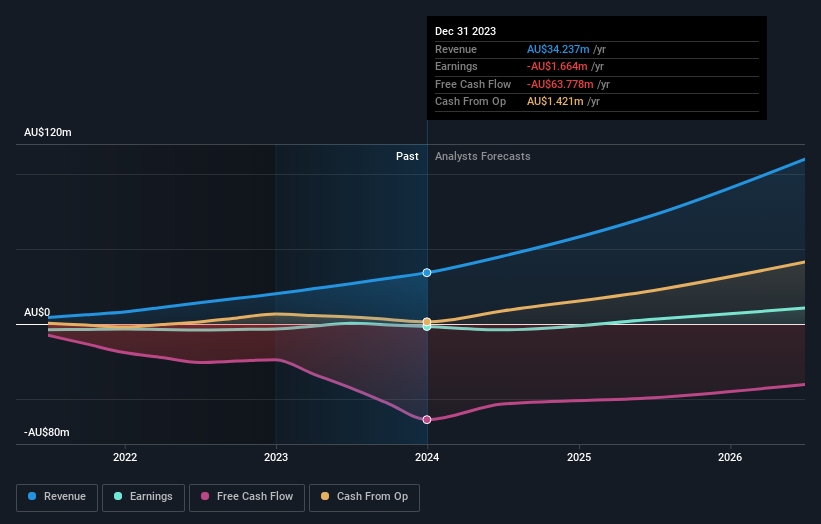

Overview: Chrysos Corporation Limited develops and supplies mining technologies across Europe, the Middle East, Africa, the Asia-Pacific, and the Americas with a market cap of A$818.92 million.

Operations: The company’s revenue primarily comes from its mining services segment, which generated A$80.36 million.

Insider Ownership: 15%

Chrysos Corporation demonstrates potential as a growth company with high insider ownership, evidenced by its forecasted revenue growth of 22.3% annually, outpacing the broader Australian market. Despite low forecasted return on equity and limited insider buying in recent months, Chrysos is expected to become profitable within three years. Recent earnings results show significant improvement with A$43.4 million in revenue and a net income of A$0.732 million for the half year ended December 2025, highlighting positive momentum.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: LGI Limited focuses on carbon abatement and renewable energy solutions utilizing biogas from landfills in Australia, with a market cap of A$386.87 million.

Operations: The company generates revenue through three main segments: Carbon Abatement (A$18.58 million), Renewable Energy (A$19.52 million), and Infrastructure Construction and Management (A$2.08 million).

Insider Ownership: 19.9%

LGI Limited exhibits strong growth potential, with earnings forecasted to grow at 25.8% annually, surpassing the Australian market’s average. Recent financials show a rise in sales to A$20.31 million and net income of A$3.08 million for H1 2025, reflecting a positive trend despite past shareholder dilution and low future return on equity projections. The company’s strategic leadership transition is underway as CFO Dean Wilkinson plans retirement in September 2026, ensuring stability during this growth phase.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment