9 out of 18 asset revaluation stocks fall

Attention should be paid to land-oriented revaluation companies

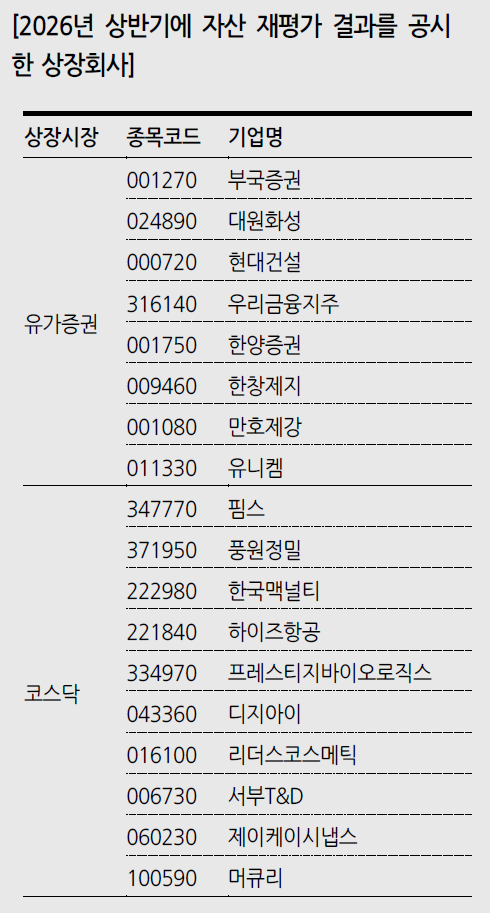

![Status of listed companies that disclosed the results of asset revaluation in the first half of 2026. [Data = Hanwha Investment & Securities]](https://wimg.mk.co.kr/news/cms/202607/02/news-p.v1.20260702.831525780a2649ffb83f62265c95c4da_P1.png)

Recently, low PBR (share price net asset ratio) stocks with real assets such as land and buildings are becoming more attractive on the back of intensifying inflation and soaring real estate prices.

In addition, shareholder activities that require asset revaluation of tangible assets and investment real estate reflected in acquisition costs have recently become active, and some in the market are expecting a rise in stock prices due to asset revaluation. However, it was analyzed that the impact of actual asset revaluation results on stock prices is not as simple as expected.

Hanwha Investment & Securities surveyed 18 listed companies in the securities and KOSDAQ market that announced the results of the asset revaluation in the first half of this year on the 2nd and found that eight stocks rose, nine fell, and one remained unchanged after the revaluation announcement. Of the eight gainers, only one surged to the upper limit, followed by gains of 9.1 percent, 5.5 percent and 3.8 percent in the top group of stock gains, while the other four saw gains of less than 1.5 percent.

Eom Soo-jin, a researcher at Hanwha Investment & Securities, pointed out, “You may think that the implementation of asset revaluation on land and buildings will be a positive factor for stock prices, but in fact, the impact and effect of asset revaluation are complex.”

According to the 18 companies that disclosed asset revaluation in the first half of the year, eight companies were listed in the securities market, including Bukuk Securities, Daewon Hwaseong, Hyundai Engineering & Construction, Woori Financial Group, Hanyang Securities, Hanchang Paper, Manho Steel, and Unikem.

In the KOSDAQ market, 10 companies, including Pims, Pungwon Precision, Korea McNulty, Heize Airlines, Prestige Biologics, DGI, Leaders Cosmetics, Seobu T&D, JK Synaps, and Mercury, have been reevaluated.

The most dramatic example was the Great Mars. Daewon Hwaseong announced at 9:16 a.m. on June 18 that it reevaluated the land in Osan, Gyeonggi-do, where the factory is located, raising its book value from 36.3 billion won to 91 billion won. Trading volume also nearly tripled compared to the day before the announcement.

Daewon Hwaseong’s revaluation difference reached 54.8 billion won, and the debt-to-equity ratio is expected to improve from 238.7% to 137.2% as the total loan dependence decreases.

Daewon Hwaseong is a manufacturer of plastic synthetic leather and is believed to have aimed at improving its financial structure through this re-evaluation at a time when the financial burden has increased since the suspension of the wallpaper business.

Mercury stands out in the KOSDAQ market. As a result of re-evaluating the land of its headquarters in Gajwa-dong, Seo-gu, Incheon at 9:52 a.m. on January 6, Mercury announced the re-evaluation of the land from the previous book value of 10 billion won to 68.5 billion won, and the stock price closed more than 9% higher than the previous day.

On the other hand, many stocks did not elicit a significant response from the market. This is because the market already knows that major land or buildings, which account for a large portion of total assets, have a higher market price than acquisition costs, which was reflected to some extent in the usual stock price.

In addition, in the case of companies whose asset revaluation announcement and earnings announcement overlapped, slower growth and weaker performance momentum were more decisive factors in the stock price decline than the value of the revaluation book that could not generate immediate cash flow. For example, the stock prices of Hyundai Engineering & Construction and Woori Financial Group fell 2.51% and 5.28%, respectively, after the disclosure of the asset revaluation.

Researcher Um Soo-jin said, “The re-evaluation of assets also comes with side effects, such as worsening profitability indicators such as ROA (total return on assets) and ROE (return on equity capital) and causing a decrease in net profit due to increased depreciation costs.”

Hanwha Investment & Securities Co. cited successful asset revaluation cases such as trying to raise its credit rating before borrowing a large amount to invest in promising future businesses or implementing it for the first time since its establishment to support long-term pent-up stock prices by accepting reasonable demands from minority shareholder solidarity.

Hanwha Investment & Securities advised that when looking at stocks related to asset revaluation, it should pay attention to “holding” rather than “building owners.” When book value rises due to revaluation, intensive revaluation of land that is not subject to depreciation at all rather than buildings or general tangible assets can significantly alleviate the fatal side effects of asset revaluation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment