The Psychology of Gold Ownership: Why What You Think You Own and What You Actually Own Are Two Different Things

Most investors build their understanding of asset ownership through the lens of brokerage statements. A number appears on a screen, it moves with the market, and the brain files it under the appropriate mental category. With gold, this cognitive shortcut creates a structural blind spot that only becomes visible under exactly the conditions investors are trying to protect themselves from.

The distinction between holding an asset and holding a claim on an asset sits at the foundation of any serious analysis of physical gold vs digital gold. In calm markets, the gap between these two states is largely theoretical. When financial systems come under stress, that gap can become the difference between wealth preservation and a lesson in counterparty risk.

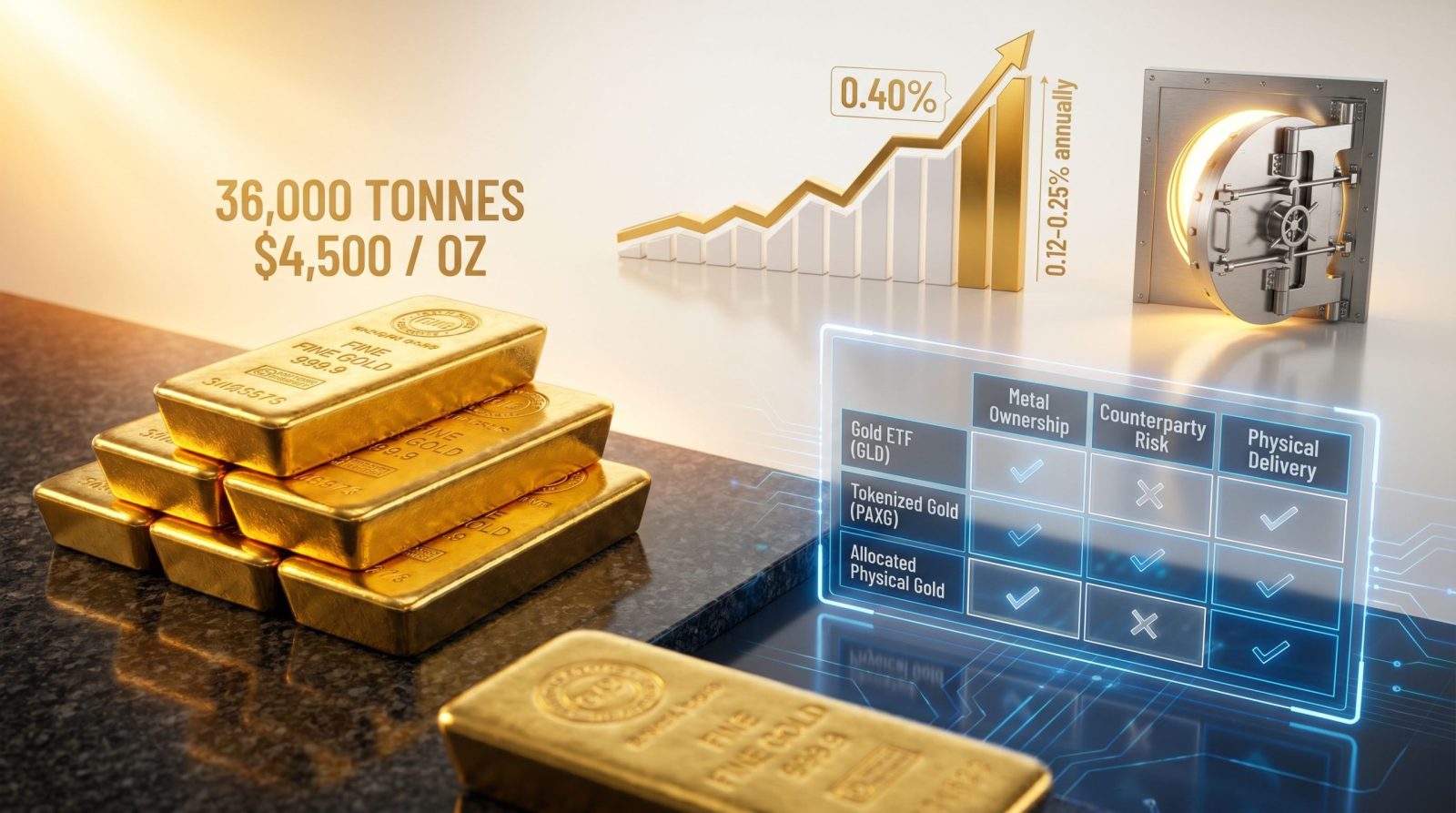

With gold trading at approximately $4,500 per troy ounce as of May 2026 (World Gold Council), significant new capital has entered the market across a range of gold-linked instruments. Not all of that capital represents genuine gold ownership. Understanding precisely what each product type delivers, and where its structural limits are, is the foundational analysis most investors skip.

When big ASX news breaks, our subscribers know first

Mapping the Digital Gold Landscape: A Structural Taxonomy

The term digital gold is applied loosely across a wide range of instruments that share a common feature: their value is derived from the gold price, but they do not convey ownership of the metal itself.

Gold ETFs: Financial Instruments, Not Metal Interests

Gold exchange-traded funds such as SPDR Gold Shares (GLD) and iShares Gold Trust (IAU) are among the most widely held gold-linked instruments globally. These funds hold physical gold in custodial vaults, but investors in the fund hold shares, not metal. The legal structure does not permit retail shareholders to take delivery of their proportional gold holding. Upon sale, proceeds are settled in currency.

The GLD expense ratio sits at 0.40% annually (SPDR Gold Shares), making it cost-efficient for financial market exposure. However, the instrument is structurally a fund share, not a direct metal interest. For a deeper comparison of physical gold vs ETFs, understanding this structural distinction is essential before allocating capital.

Gold Futures and Options: Expiring Price Agreements

Futures contracts are time-bound agreements on the price of gold. The overwhelming majority of futures positions are closed out before expiry, meaning metal rarely changes hands. These instruments serve legitimate hedging and speculative purposes but carry leverage, margin call exposure, and rollover costs that make them structurally unsuitable as long-term wealth preservation vehicles.

Tokenized Gold: Blockchain Representation With Variable Redemption

Products such as Paxos Gold (PAXG) and Tether Gold (XAUt) represent gold positions on distributed ledgers, theoretically backed one-to-one by a troy ounce of vaulted metal per token. In practice, redemption mechanics, regulatory standing, and custodial transparency vary considerably between providers and across jurisdictions. Retail access to physical delivery remains limited in most implementations, and the regulatory environment governing these products continues to evolve.

Unallocated Gold Accounts: Claims Against a Pool

Bank and fintech gold savings products typically operate on an unallocated basis. The investor holds a proportional claim against a pooled gold holding owned by the institution. The metal appears on the institution’s balance sheet, not the investor’s. This structure introduces counterparty exposure that is absent from direct physical ownership.

Structural Comparison: Digital Gold Product Types

| Product Type | Metal Ownership | Counterparty Risk | Physical Delivery | Liquidity |

|---|---|---|---|---|

| Gold ETF (e.g., GLD) | No, fund shares | Moderate, custodian | Not available to retail | High |

| Gold Futures | No, price contract | High, exchange/broker | Rare in practice | Very High |

| Tokenized Gold (e.g., PAXG) | Theoretical | Moderate to High | Limited for retail | Medium |

| Unallocated Gold Account | No, pool claim | High, institution | Generally unavailable | Medium |

| Allocated Physical Gold | Yes, direct ownership | None | On demand | Medium |

The Structural Properties That Make Physical Gold Different

Physical gold is not a financial instrument. It is the monetary asset itself, and that distinction carries structural consequences that compound in importance as market conditions deteriorate.

Supply Scarcity as a Monetary Foundation

Global annual gold production runs at approximately 3,661 tonnes per year, against a total above-ground stock of roughly 216,000 tonnes (World Gold Council). This stock-to-flow ratio means annual production adds less than 2% to existing supply each year, a figure that barely shifts regardless of price incentives.

Gold cannot be manufactured, printed, or conjured by institutional policy decisions. This physical constraint underpins its function as a long-term store of value in a way that no financial instrument can replicate. Furthermore, buying physical gold through allocated storage programmes makes this structural advantage increasingly accessible to retail investors.

The Counterparty-Free Asset

Physical gold held in an investor’s possession or in genuinely allocated storage carries no counterparty dependency. Its value does not depend on any institution remaining solvent, any technology platform continuing to function, or any legal framework recognising a claim. This property sits entirely outside the conventional financial liability chain, which is why it behaves differently from gold-linked instruments precisely when those instruments come under the most stress.

The Institutional Signal: What Central Banks Actually Hold

Central bank gold reserves globally exceed 36,000 tonnes of physical gold in bar form (IMF / World Gold Council), and that aggregate figure has grown every year since 2010. Sovereign reserve managers do not hold ETF shares. The institutional reasoning is structural: physical gold is the only reserve asset whose integrity cannot be compromised by another government’s decision, another institution’s insolvency, or another central bank’s policy choice.

France’s repatriation of its gold reserves from US custody between mid-2025 and early 2026 illustrates this principle in action at the sovereign level. The decision reflects a preference for direct physical possession over custodial claims, a preference that mirrors the structural argument available to any investor serious about genuine wealth sovereignty.

The institutions with the deepest analytical resources and the longest investment horizons hold bars, not fund shares. The structural logic behind that choice applies with equal force at the individual investor level.

When the Paper-Physical Divergence Becomes Real

March 2020: The Crisis That Revealed the Gap

During the March 2020 COVID-19 market dislocation, GLD fell approximately 13 to 14% from its February 2020 high as leveraged investors liquidated positions to raise cash (World Gold Council). The mechanism had nothing to do with gold’s monetary properties. Forced selling by margin-pressured investors with no fundamental view on the metal drove paper prices lower.

Physical gold premiums at dealers rose at exactly the same time. The metal became harder to acquire as its paper price declined, demonstrating that the two instruments respond to fundamentally different demand drivers.

April 2025: A More Severe Repeat

The same dynamic recurred in April 2025, with greater severity. Paper gold sold off on forced liquidations and margin calls while physical premiums widened to levels not observed in decades. The divergence was not an anomaly. It was the structural mechanics of two different instruments doing exactly what their designs predict under stress.

The paper-physical spread does not open during normal market conditions. It opens precisely when conditions are abnormal, which is exactly when an investor’s definition of a safe-haven asset is being tested in real time.

The ETF Recourse Chain Under Stress

A gold ETF functions through a chain of authorised participants, custodial institutions, and settlement infrastructure. Under normal conditions, this chain is invisible and frictionless. Under systemic stress, including banking freezes, settlement failures, or custody disputes, the investor’s recourse routes through those same institutions. Consequently, physical gold held in allocated storage does not share this structural vulnerability. This is a core reason why gold as a safe haven is better understood through the lens of direct ownership rather than financial instruments.

What Digital Gold Instruments Do Well: An Honest Assessment

The case for gold ETFs and related products is not without substance. These instruments serve legitimate functions for specific investor objectives.

Tactical equity hedging: ETFs offer liquid, low-cost exposure to gold price movements within existing brokerage infrastructure. For a trader managing equity portfolio risk over a three-to-six-month horizon, the operational simplicity and 0.40% annual expense ratio (SPDR Gold Shares) make ETFs a rational tool.

Tax-advantaged account compatibility: ETFs held within retirement accounts and tax-advantaged structures such as IRAs or superannuation funds offer compounding benefits that physical metal cannot replicate in the same wrapper. For retirement-focused investors whose primary concern is long-term tax efficiency, this represents a genuine structural advantage.

Accessibility and fractional entry: Digital gold platforms reduce the cost of entry and eliminate the logistical friction of physical ownership, making gold price exposure accessible to investors at any portfolio size. The Royal Mint’s analysis of physical vs digital gold diversification offers useful perspective on how investors are increasingly blending both approaches.

When digital gold instruments are the appropriate tool:

- Short-term tactical hedging against equity market volatility

- Gold price exposure within tax-advantaged retirement accounts

- Investors prioritising liquidity and transaction speed over ownership sovereignty

- Fractional or incremental exposure for smaller portfolio sizes

The Macro Environment Making This Distinction More Urgent

Monetary Debasement and the Limits of Financial Instruments

US net interest payments crossed $1 trillion for the first time in fiscal year 2025 (Congressional Budget Office), a figure that illustrates the structural trajectory of sovereign debt and currency purchasing power. Holding a brokerage position in a gold-linked instrument provides exposure to gold price movements, but it does not place the investor structurally outside the monetary system producing those dynamics. Physical gold does.

Capital Controls, Financial Surveillance, and Sovereignty Risk

An environment of increasing financial monitoring and the theoretical risk of capital controls creates specific value in the portability and privacy properties of physical gold that no digital instrument can replicate. These are not hypothetical concerns for investors in historically stable jurisdictions; they are structural features that sovereign wealth managers and central bank gold buying patterns have already incorporated into their reserve management frameworks.

The BRICS+ Accumulation Signal

Nations within the BRICS+ grouping have been systematically building physical gold reserves as part of a broader effort to construct monetary infrastructure less dependent on US dollar settlement. Central bank purchasing has continued at near-record pace, representing structural demand that operates independently of retail sentiment. This institutional accumulation pattern is itself a directional signal about where sophisticated reserve managers see long-term monetary value.

The next major ASX story will hit our subscribers first

Allocated vs Unallocated: The Distinction Most Investors Have Never Examined

Within the universe of physical gold ownership, a critical distinction separates genuinely protective structures from those that retain counterparty exposure.

| Feature | Allocated Gold | Unallocated Gold |

|---|---|---|

| Specific bars or coins in your name | Yes | No |

| Appears on provider’s balance sheet | No | Yes |

| Counterparty risk | None | Present |

| Rehypothecation risk | None | Possible |

| Insolvency protection | Strong | Weak |

Allocated gold means specific, numbered bars or coins are held in the investor’s name. That metal does not appear on the storage provider’s balance sheet and is not pooled with other clients’ holdings. Unallocated gold, however, is a proportional claim against an institution-owned pool, introducing the same counterparty exposure the investor was trying to eliminate by moving away from financial instruments. CBS News provides a useful overview of what investors should know when navigating this distinction.

Resolving the Storage Problem: The False Trade-Off

The most common objection to physical gold ownership is logistical: storage, insurance, security, and operational friction. This objection carried more weight before the development of institutional-grade allocated vault storage programmes accessible to retail investors.

Professional allocated vault storage typically costs approximately 0.12 to 0.25% annually, a figure that often compares favourably to ETF expense ratios once insurance and independent audit costs are incorporated. The defining feature of genuinely allocated vault storage is that the investor owns specific, identified metal, not a pooled claim, and retains the right to take physical delivery on demand.

This development eliminates the binary choice between convenient-but-exposed and sovereign-but-inconvenient. Institutional-grade ownership infrastructure has made the structural properties of physical gold vs digital gold accessible without the operational complexity that previously deterred retail investors.

A Decision Framework for Physical Gold vs Digital Gold Allocation

Most informed investors hold both forms of gold exposure, calibrated to their specific objectives. The strategic question is proportioning, not selection.

| Investor Priority | Recommended Instrument | Rationale |

|---|---|---|

| Short-term equity hedge | Gold ETF | Liquid, low-cost, fast execution |

| Tax-advantaged retirement growth | Gold ETF in IRA or superannuation | Tax efficiency advantage |

| Long-term monetary protection | Allocated physical gold | No counterparty risk, sovereign ownership |

| Crisis insurance and capital control resilience | Physical gold, held or vaulted | Functions outside the financial system |

| Fractional entry and accessibility | Digital gold platform | Lower cost of entry, convenience |

Investors whose primary concern is monetary debasement, systemic disruption, or capital control risk should weight physical allocated holdings more heavily. Investors whose primary concern is tax efficiency and short-term market exposure may rationally weight digital instruments more heavily. The two are not competitors; they are instruments optimised for different objectives along the same investment thesis.

Frequently Asked Questions

Is a gold ETF the same as owning physical gold?

No. A gold ETF represents shares in a fund, a financial instrument whose value tracks the gold price but which does not confer ownership of the metal. ETF shareholders cannot take physical delivery of their proportional holding, and the value of their position depends on the fund’s custodians and the broader financial system functioning normally. Physical gold carries no counterparty dependency.

Why do central banks hold bars rather than ETF shares?

Physical gold is the only reserve asset that carries no other party’s liability. It cannot be frozen by a foreign government’s decision, defaulted on by a custodian, or devalued by another institution’s balance sheet choices. Central banks collectively hold over 36,000 tonnes in bar form, a figure that has grown every year since 2010 (IMF / World Gold Council).

Can paper gold and physical gold prices diverge?

Yes. In March 2020, GLD fell approximately 13 to 14% from its February high as leveraged investors raised cash, while physical premiums at dealers rose simultaneously. The same dynamic occurred in April 2025, with physical premiums reaching levels not observed in decades. The divergence occurs because paper gold responds to financial market mechanics, including forced selling, while physical gold responds to monetary demand fundamentals.

What does allocated vault storage typically cost?

Allocated vault storage through specialist providers typically runs approximately 0.12 to 0.25% annually, which frequently compares favourably to ETF expense ratios once storage, insurance, and independent audit are included. The critical distinction from physical gold vs digital gold accounts is that the investor owns specific, identified metal and retains the right to take physical delivery.

This article is for informational and educational purposes only. It does not constitute investment advice. Past performance is not a guarantee of future results. All investments, including precious metals, involve risk. Please consult a qualified financial adviser before making any investment decisions.

Want To Know Which ASX Stocks Could Be The Next Major Mineral Discovery?

Discovery Alert’s proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex geological data into actionable investment insights the moment they’re announced — explore historic discoveries and their exceptional returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment