If you’ve been consistently contributing to the C and S Funds, congratulations. With the S&P 500 recently breaking past 7,200 and hitting new all-time highs, your TSP balance is likely looking better than ever.

You’ve earned those returns. Now it’s time to protect them. Because there’s an uncomfortable truth about Wall Street that every investor eventually learns:

Paper profits aren’t real until you lock them in.

Right now, the C and S funds are doing great because they’re tied to the stock market, which is hitting new highs. But leaving 100% of your profits sitting in there is like hitting the jackpot at the casino and betting it all on the next spin.

While the headline numbers look great, smart money is already looking at what comes next. Because they see how fragile the broader economy is, and underneath the hood there’s not one, but four major warning signs that are flashing red.

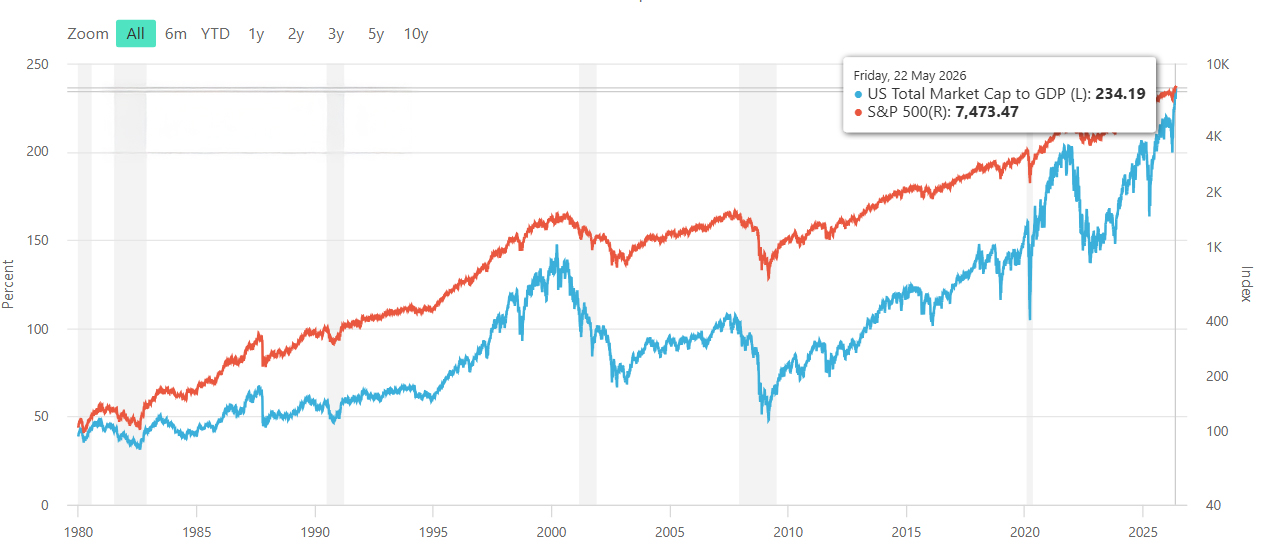

The Warren Buffett Indicator

Warren Buffett’s single favorite market metric is a simple calculation that compares the total value of the U.S. stock market to the entire GDP of the country. It’s a widely cited metric because it answers a fundamental question: Is the stock market growing because the economy is growing, or is it just overvalued speculation?

Historically, a ratio of around 100 means the stock market is fairly valued and accurately reflects the real-world economy. Economists generally agree when the ratio reaches 200 it’s getting into a danger zone. Right now, the Buffett Indicator is sitting at a record high of 234.

To put that in perspective, during the absolute peak of the 2000 Dot-Com bubble, just weeks before a crash wiped out trillions of dollars in retirement wealth, the indicator only reached roughly 160. A reading of 234 means the market is severely overvalued right now.

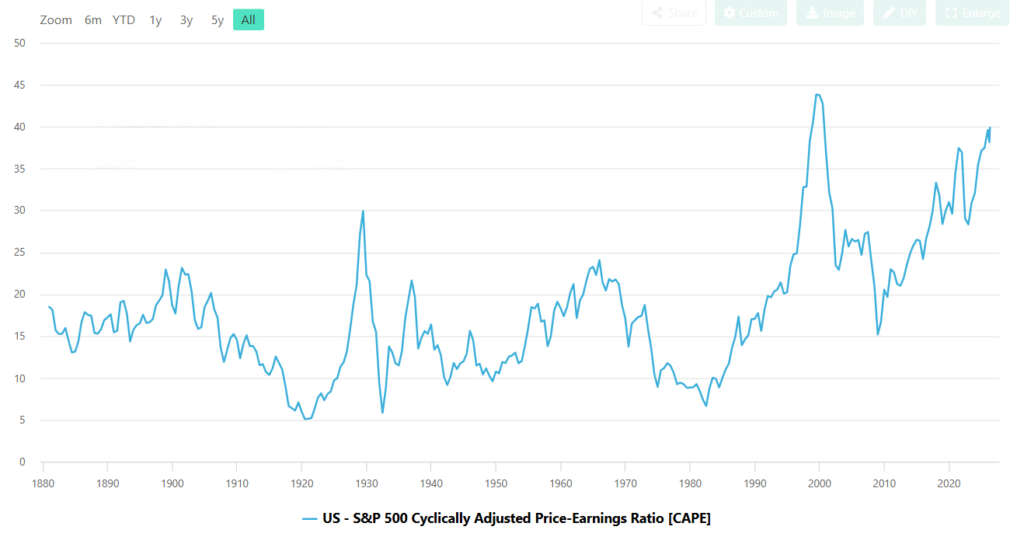

The CAPE Ratio

The Cyclically Adjusted Price-to-Earnings (CAPE) ratio evaluates how expensive stocks are by looking at inflation-adjusted corporate earnings averaged over the past 10 years. This is a critical metric because it smooths out short-term profit spikes and corporate stock buybacks, revealing the true, long-term valuation of the market. Historically this ratio is around 17.

Today, the CAPE ratio is sitting at a blistering 39.89. In the entire history of the U.S. stock market, valuations have only reached these extremes twice: during the late-1990s tech bubble, and the post-COVID stimulus frenzy of 2021.

Both of those periods ended in devastating, prolonged market corrections that wiped out years of retirement gains for investors who didn’t rotate their profits in time.

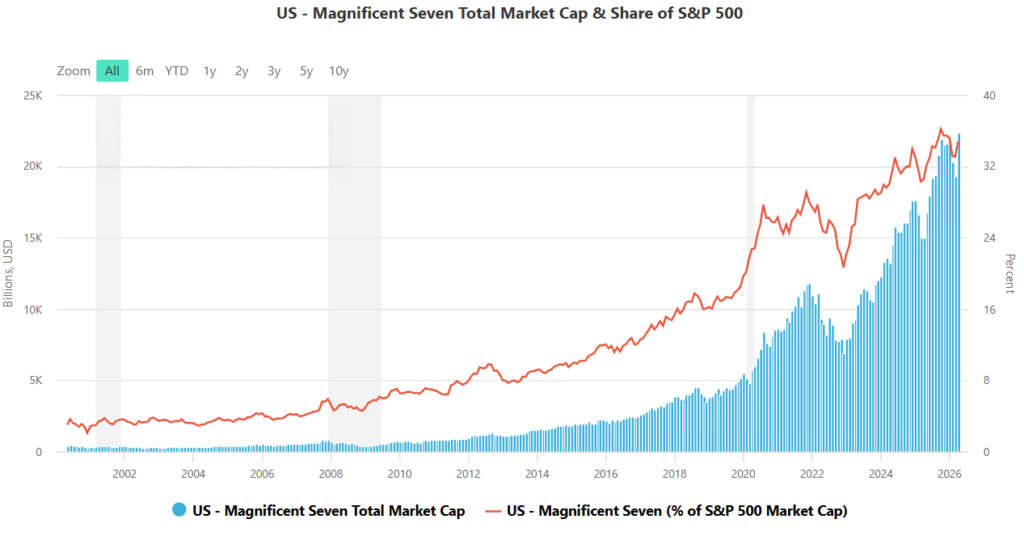

The AI Tech Bubble

When you look at the S&P 500, it looks like the entire corporate landscape is booming. But that’s an illusion. The recent gains are heavily concentrated in a handful of mega-cap technology companies spending billions on Artificial Intelligence infrastructure.

While these companies are profitable, their stock prices have skyrocketed far beyond what many believe their current earnings can actually justify. Their record-high valuations are being propped up by hundreds of billions of dollars spent on AI infrastructure, fueled by the hope that it will eventually generate enough profit to justify the hype.

The market concentration is so extreme that even top banking executives and prominent tech leaders are sounding the alarm, openly saying this looks more and more like a bubble. That means disappointing future earnings in any one of these big tech companies could pop the bubble, and drag the entire market down like dominoes.

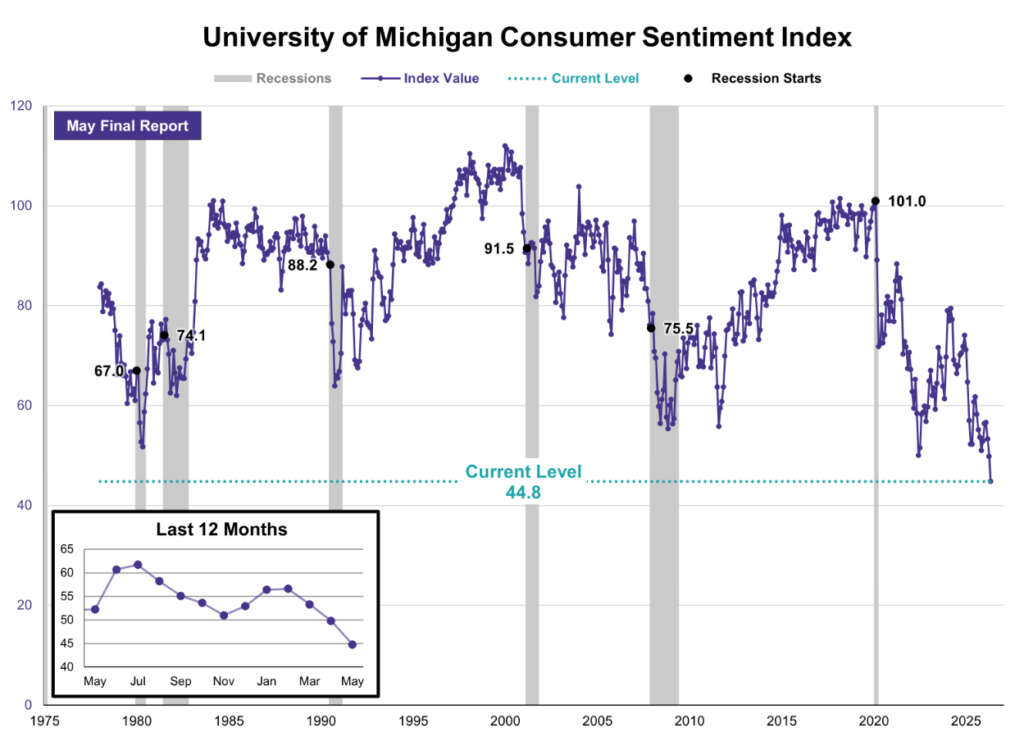

The Consumer Sentiment Index

Finally, there’s a major disconnect between Wall Street wealth and Main Street reality. While the stock market hits all-time highs, consumer sentiment is plunging. Everyday Americans are being suffocated by sticky inflation, skyrocketing debt, and high borrowing costs.

In fact, the University of Michigan’s famous Consumer Sentiment survey just recorded the lowest level in its over 50 years of existence. Meaning, never before in modern history have Americans been more pessimistic about the future of the economy.

Historically, the stock market cannot defy gravity forever when the underlying consumer base is financially tapped out. Consumer spending makes up for 70% of the GDP, which means when there’s a gap this big, eventually there’s always a reckoning.

Locking In Tax-Free Gains

History shows exactly what happens when investors ignore these warning signs. In 2000, these exact same indicators flashed red just before the dot-com crash wiped out $5 trillion in wealth. In 2008, another $7 trillion vanished. And in 2020, a liquidity shock erased 30% of the market in a matter of weeks.

Market crashes don’t come with a warning memo. They happen overnight, wiping out years of profits before anyone can react.

Today, the economy is teetering on the edge again. The ongoing war with Iran has triggered a global energy crisis, sending oil prices surging and reigniting inflation. Looking at the broader economy, your C and S Fund balances are like a roller coaster car slowly clanking to the absolute peak of the track. A steep drop is inevitable.

Protecting your retirement isn’t about perfectly timing the market top. That’s impossible. It’s about reading the data and recognizing when it’s time to lock in your gains with something real.

When indicators reach historical extremes, amateur investors get greedy. They leave their entire life savings exposed to the paper market, riding the roller coaster up, and eventually riding it right back down when the correction hits.

Savvy investors rotate profits into physical assets.

And since your funds are inside a TSP, you can actually move those profits into physical assets completely tax free.

The Gold “Loophole” for Federal Employees

Most federal employees assume the only way to protect their money from a market correction is moving it to the G-Fund. But as we’ve seen with inflation running rampant, the G-Fund’s low yield guarantees a loss of purchasing power over time.

Fortunately, there’s a better way.

Thanks to a little-known provision in the TSP Modernization Act, federal employees over the age of 59½, and those who are already retired, don’t have to choose between the risks of the C Fund and the inflation trap of the G Fund.

You’re legally allowed to use a penalty-free, tax-free rollover that moves a portion of your TSP funds into a Gold IRA.

This allows you to take paper profits and convert them into physical, government-backed precious metals, like American Gold Eagles minted by the U.S. Mint.

By rotating a portion of your profits into gold, you’re locking in your gains permanently.

You’re also building an inflation-proof, market-proof shield around your retirement, while keeping all the tax advantages of your traditional retirement account.

How To Learn More

Financial advisors who make commissions off your C and S Fund mutual funds aren’t going to tell you to rotate your profits into physical metals. But keep in mind, they get their fees whether the market goes up or down.

That’s why National Gold Group created a free guide written specifically for federal employees and retirees, called “The TSP-to-Gold Guide.”

Inside this free guide, you’ll discover:

- The “TSP-to-Gold” Strategy: The exact 3-step, tax-free rollover process that lets you move a portion of your money without triggering IRS penalties, taxes, or costly mistakes.

- The “Crisis Shield” Analysis: A visual breakdown of exactly how gold reacts during violent stock market crashes, liquidity shocks, and periods of high inflation.

- The “Peace of Mind” Protection Plan: How to use your TSP funds to get government-backed physical gold, verify your gold is secured in IRS-approved depositories, and avoid predatory ongoing IRA fees.

- The “Total Control” Distribution Playbook: How to maximize your liquidity, including how to take physical delivery of your metals or liquidate them for cash, maintaining full control over your retirement withdrawals without getting trapped by hidden fees.

You’ve earned the profits in your TSP. Now make sure to protect them with something real.

>> Download your free guide here.

Copyright

© 2026 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment