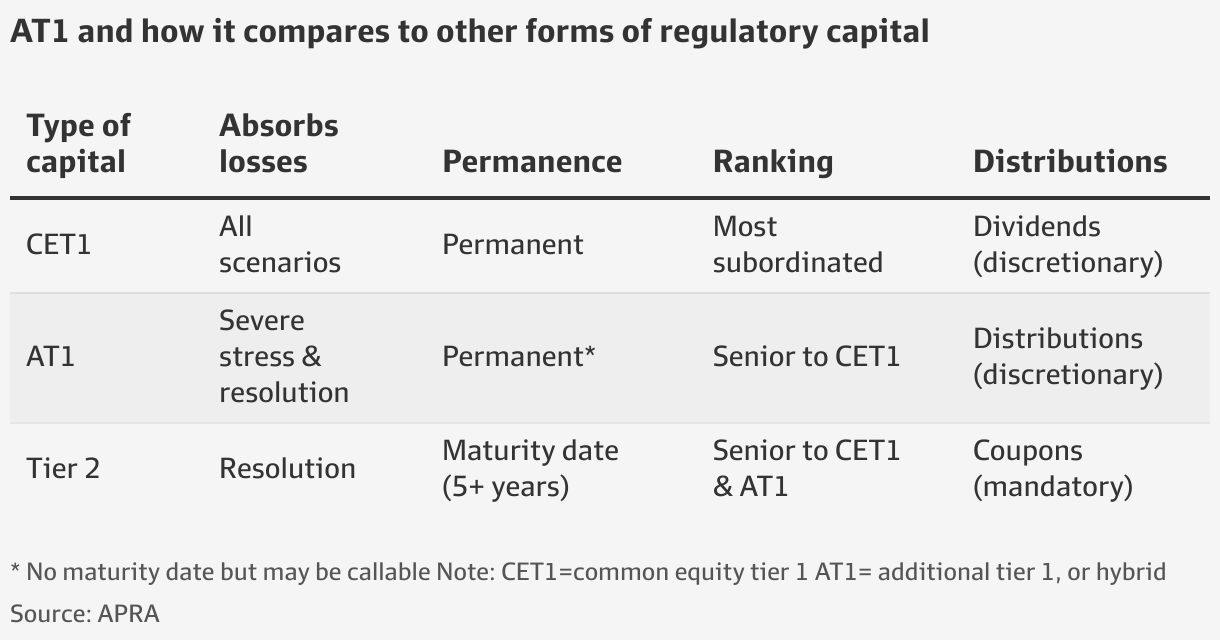

But the paradox of hybrids is that APRA wants investors to believe the banking system is safe while also impressing on investors in hybrids that they are insuring the banking system and that they should appreciate the policy may be called upon. In other words, they may be forced to take a hit if things get wobbly.

Loss for mum and dad investors

APRA’s concern is that the banks have raised almost all of this $43 billion of hybrid capital via ASX-listed securities issued to ordinary Australians. It estimates just over half the securities are in parcel sizes under $500,000, and are therefore small investors.

That worries APRA because it might be impractical and unpopular to force mum and dad investors to take a loss, and actually spread fear, rather than reassure depositors that they have this layer of capital to protect them.

So, APRA is proposing tweaks to the structure of hybrids and exploring ways to change the ownership base so that global institutions, and not ordinary investors, are providing this layer of insurance.

Some would argue this is a well overdue step, if not an outright admission it has made a multi-decade mistake in allowing the situation. In several instances in Europe, banks and regulators have run into political trouble when they have sought to bail in retail investors, and in some cases have back-tracked.

Of course, the most recent high-profile case was the move by Swiss regulators to wipe out Credit Suisse tier one holders when it was acquired by UBS. Here the investors were mainly global institutions, but some private bank customers and even staff who were paid bonuses in hybrid capital lost money.

But the counter-argument is that APRA is going too far and is fixing something that ain’t broke. The prudential regulator lays out carefully what is required of a security to meet its definition of regulatory capital. But is it APRA’s role to decide who actually provides that capital? It’s a tricky one.

Some veterans in the industry dispute APRA’s assessment that small investors comprise just over half of the hybrid investor base. They say it’s about a quarter of that, because larger wealthy investors have spread their millions across a range of securities.

But that does not mean there aren’t market structure issues to be aware of. Some sources say clients of just one wealth group accounts for a quarter of the ownership of the hybrid market. That one firm’s clients are providing this much regulatory capital to our esteemed financial system is curious.

If APRA does, however, engineer a migration of tier one capital from the ASX-listed investor base to institutions, that process will involve a lot of friction and some high cost.

It will also have implications for the cost of bank capital. Hybrids are an extraordinarily cheap form of financing for the banks, in part because they are considered as equity by the tax office, which allows them to pay those highly coveted franked distributions to holders.

When a bank markets a hybrid deal, the rate and margin includes the franked component, but the bank pays only the cash cost. This means it is effectively raising equity capital at less than half the return on equity.

But it’s a privilege afforded only to Australian banks. In other jurisdictions, banks must pay hybrid investors a more competitive rate. In fact, the handful of Australian bank hybrids issued in the global market trade at rates that are about 1 to 2 per cent above the ASX-listed equivalents.

The consequence of this is that if Australian banks are forced to raise their tier one capital from institutions that can’t access franking credits, the costs are going up, and they might require a tax ruling that makes the interest payments deductable.

This may lead the banks, including the regionals, to opt for other forms of capital such as common equity to meet minimum capital requirements.

On the investor side, it may result in investors accessing these securities via managed funds or exchange traded funds. There are positives and negatives from this.

In some respects, credit and fixed income is better suited to investing in these structures that lower costs and increase diversification. In fact, more investors prefer ASX-listed hybrid and subordinated ETFs to access the asset class.

But some would argue that direct access to securities should be encouraged, especially in the period ahead, in which fixed income offers compelling returns to equities.

A move too far?

One sector that will not welcome this development is stockbrokers. The steady stream of hybrid deals from the big banks has been a source of fee income for brokers and wealth managers in all market conditions. Brokers are paid a 0.75 per cent selling fee and a 0.5 per cent joint manager fee on deals. (Hybrids were exempted from a law change that banned stamping fees.)

About $12 million of fees were paid by National Australia Bank to a roster of joint and co-managers for distributing its $1.25 billion issue. Whether the fees dry up and how brokers respond remains to be seen. But it may result in an evolution of what fixed income products are sold to investors and how. That may be healthy as the asset class becomes even more relevant.

The final issue is whether APRA has gone too far, and is over-emboldened by a mandate to shore up the banking system no matter the cost. It could be argued that bank hybrids are so popular, and the yields so low, because APRA has done such a good job. The incentive for APRA is to tighten up the system as much as possible, and after another wave of global bank failures, it has the political cover to go even harder.

But we should recognise there is a cost of safety, and a debate is starting to bubble away that APRA supervision has created a homogenous, risk-averse system that may be withholding credit from parts of the economy that could do with it. It’s also why investors – be they little old ladies or wealthy families – are prepared to backstop the banking system at a favourable rate.