We’re seeing a frenzy among investors seeking access to SpaceX before it goes public.

That’s been a boon to one mutual fund (Baron Partners BPTIX) and three exchange-traded funds (Baron First Principles RONB, ERShares Private-Public Crossover XOVR, and Tema Space Innovators NASA) that built stakes in SpaceX private equity. Those four funds saw $7.9 billion in combined net inflows in May alone, a massive haul.

To state the obvious, it’s not advisable to invest in a fund or ETF for the exposure it affords to a particular security, even one as highly sought-after as SpaceX. Nonetheless, some investors have clearly chosen to do so, and therefore the question for them is what’s next.

That question doesn’t have a simple answer. It will depend on how large the SpaceX position is as a percentage of each fund’s net assets, as well as the degree to which the position appreciates in value between now and the moment it begins publicly trading.

The Math of It

Before I delve into each variable, one question investors might have right off the bat is how much they could gain from owning a stake in SpaceX via these funds. Arithmetically, the payoff should approximate the change in SpaceX’s value at any points between now and the day of its IPO times the position’s percentage weighting in the fund at the relevant times.

If, for instance, an ETF doesn’t change its SpaceX fair value between now and when trading begins, it’s simply the difference between that fair value and where it prices at the opening on day one times the stake’s percentage weighting entering that day.

On the other hand, if an ETF changes its mark between now and the day of its IPO, it’s the change in the valuation on the day the mark is changed multiplied by the position’s weighting entering that day, and so forth through IPO day.

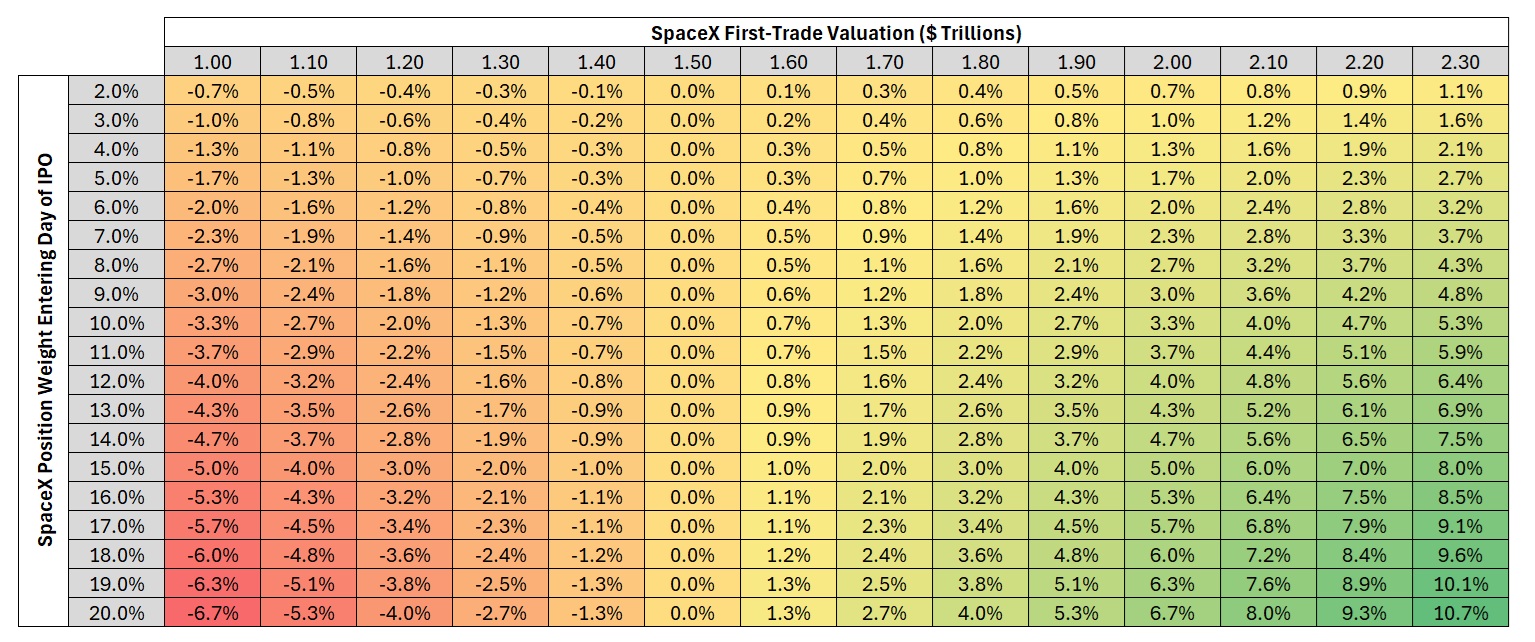

Here’s a matrix illustrating a simple hypothetical scenario in which an ETF today values its SpaceX stake to correspond to a $1.5 trillion SpaceX valuation and doesn’t change that mark until the stock begins to trade. The vertical axis shows various possible percentage weightings for the stake, and the horizontal axis shows potential valuations once trading begins. The cells show the percentage contribution SpaceX would make to returns for each pairing.

The larger the weighting and valuation change between now and when trading begins, the larger the potential payoff would be. For instance, if a fund entered IPO day with SpaceX at a 15% weighting and the stock began trading at a price corresponding to a $2 trillion valuation, that fund would see a 5-percentage-point boost to returns (that is, the 33.3% valuation gain from $1.5 trillion to $2 trillion multiplied by the 15% weighting = 0.05).

It’s worth noting that, unthinkable as it might seem given the nonstop hype surrounding the IPO, it’s possible the stock could trade down at the open, with that potential scenario also represented in the matrix above.

Position Weighting

The math of any potential payoff is straightforward, but it’s hard to predict because it hinges on two variables—the position’s weighting and the change in SpaceX’s value—that are harder to handicap.

Let’s start with the position weighting. This one doesn’t have to be complicated. Usually when a fund takes a position in a security, the weighting won’t fluctuate that much because the manager can buy and sell to adjust the position to the desired weighting as needed.

But that’s not how it works when it comes to private equity. Though some of these ETFs have been able to pad their stakes over time, the position is largely fixed in dollar terms, and it’s questionable whether these ETFs will be able to transact in the short time until the IPO.

Thus, practically speaking, the position will be much more sensitive to changes in the ETF’s size than would ordinarily be the case. For instance, suppose an ETF has a $200 million SpaceX stake that accounts for 10% of net assets. If that ETF sees $500 million of fresh inflows, pushing net assets to $2.5 billion, the weighting will shrink to 7.5%. This isn’t theoretical—it’s played out at each of these funds and ETFs as money has poured in.

Paradoxically, the more popular these ETFs become with investors, the greater the possibility that influx of assets will dilute the SpaceX weighting, thereby potentially lessening the very thing it’s being so sought for in the first place: its potential to contribute to performance.

Valuation

We don’t know how the market will value SpaceX once trading begins. What we do know is how these ETFs had marked their SpaceX positions as of May 29, 2026.

(Note: Baron Partners held a roughly 31.7% stake in SpaceX as of April 30, 2026, the most recent date holdings were reported. It appears it was valuing those shares at an implied $1.25 trillion value on that date.)

It stands to reason that the lower a fund’s mark, the more potential upside it has, and so on that basis it would appear the Baron ETF has the most room to run. That said, any of these three ETFs could change its mark in the days ahead. In fact, the managers arguably have some incentive to mark up their positions before additional assets flood in and further shrink the SpaceX stake as a percentage weighting.

We could see an indicative price range for SpaceX shares in the coming days, and, with that, it’s possible the managers will change their marks.

Day 1 and Beyond

Once SpaceX begins trading, anyone who wants the stock can buy it on the open market. At that point, whatever scarcity value these funds and ETFs have derived from the pre-IPO exposure they’ve afforded expires. That explains why the period between now and the stock’s first tick as a public stock is most relevant to an investor trying to suss out what’s next.

By the same token, the days following IPO could get interesting for investors who opt to stay in these funds and ETFs. Here’s why: If some investors have temporarily camped out in them for SpaceX exposure, it’s possible they’ll bail once the stock starts trading. Should that occur, these funds and ETFs could see outflows swell their SpaceX weighting, a scenario that has precedent.

While it’s true that SpaceX equity would be liquid by then, these funds’ and ETFs’ SpaceX stakes could be subject to lockup provisions and other limits on their sale. Were that the case, they would need to meet any redemptions from liquid assets, thereby explaining why the portfolio could shrink around the SpaceX position, increasing its weighting.

(It’s also worth considering potential tax impacts if appreciated stocks must be sold to fund redemption. Those consequences would likely loom larger for the Baron mutual fund than the ETFs given ETFs’ ability to sidestep capital gains by purging low-cost basis shares as part of the in-kind creation/redemption process or by harvesting losses in the normal course.)

Though the funds and ETFs could face limits in paring their SpaceX position post-IPO, they would still be expected to value their SpaceX stake in line with however the public equity was being priced in the open market. Thus, the position could grow to a large weighting, remain illiquid, yet be no less volatile than the publicly traded, fully tradable version.

This isn’t bad, per se, especially from the standpoint of investors who are bullish on SpaceX’s prospects and therefore welcome a potentially large stake that will be held for some time. Nonetheless, it could court significant risk depending on the position’s eventual size and how the public equity trades after the offering.

Reminder: It’s 1 Position Among Many

The SpaceX stake alone isn’t going to drive these funds’ returns. As I showed earlier, two of the three ETFs have seen their SpaceX position diluted to a single-digit weighting by heavy inflows. That means other holdings are likely to be the main performance driver, at least through the IPO.

The only possible exception is Baron Partners, which entered May with around 31.7% of its net assets in SpaceX. In the time since, that fund saw about $3.8 billion in additional inflows, pushing net assets to nearly $16.6 billion by the end of May. Thus, the position has probably shrunk significantly as a percentage weight, though its exact size won’t be known until the firm reports holdings as of May 31, 2026.

That aside, these funds will largely ride with their other publicly traded stock holdings between now and the IPO. In the Tema ETF’s case, it’s around three dozen other common stocks tied to firms like Rocket Lab, Planet Labs, and Intuitive Machines, which align with the strategy’s “emerging space economy” theme. Those stocks have surged since the ETF launched in March 2026, but they look very pricey and have been volatile.

Apart from its private holdings, the ERShares ETF invests in a basket of around 30 stocks that constitute an “entrepreneur” index that its manager developed, with holdings ranging from behemoths like Nvidia and Alphabet to relative upstarts like Tempus AI and Pegasystems.

That index, and the ETF, have been subpar performers: From the ETF’s November 2017 inception through May 31, 2026, the index appears to have gained around 16% per year, but the ETF earned only 10.7% annually over that span, compared with 18.4% per year for the Russell 1000 Growth Index. From Dec. 3, 2024, when the ETF initiated its stake in a SpaceX special-purpose vehicle, through May 31, 2026, the ETF gained 6.9% per year, slightly better than its index (6.3% annually) but worse than the Russell index (18.3% per year).

Finally, the Baron ETF also invests in a focused portfolio of growth stocks like Tesla. It’s modeled after the Baron Partners fund, with which it shares most of its holdings in common. While Baron Partners has delivered exceptional long-term returns, our analysts have misgivings about the manager’s penchant for extreme concentration in individual names. The ETF doesn’t appear to be as bunched in its top holdings as its open-end sibling, but it’s a risk that bears monitoring.

Switched On

Here are other things I’m reading or watching to:

- Morningstar’s Guide to College-Savings Plans

- Jason Zweig on the insidiousness of taxes on our fund investments

- Wemby (duh)

- “Dazed and Confused” (which celebrated the 50th anniversary of its May 28, 1976, “last day of school” date this past Thursday)

- Band of Brothers “Points”

Don’t Be a Stranger

I love hearing from you. Have some feedback? An angle for an article? Email me at jeffrey.ptak@morningstar.com. If you’re so inclined, you can also follow me on Twitter/X at @syouth1, and I do some odds-and-ends writing on a Substack called Basis Pointing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment