This AUM growth rate over the three years is highly positive. However, if we look at the same numbers as a percentage of the mutual fund industry’s total AUM, we get a different picture. In February 2023, it was 16.8% of total AUM. Now, it is 18.6%. In relative terms, it has grown; but in terms of share of the total pie, the extent of growth is not great. Globally, in advanced markets, the relative share of passive funds is much higher. This begs the question: what inhibits their growth in India?

Advantages

The first advantage of passive funds is their lower expense ratio, known as the total expense ratio (TER). Compared to actively managed fund, it is much lower in passive funds since fund manager intervention is minimal.

However, their advantages extend beyond the TER. Mutual fund net asset values (NAVs) are published net of TER, hence the returns you compute are net of expenses anyway. If an actively managed fund outperforms the benchmark index, it is doing so after the expenses. Hence, if the active fund is outperforming the benchmark, arguably, the investor should not grudge the expenses. As the famous saying goes, there is no free lunch.

The broader issue is that most actively managed funds, say more than 50%, are not outperforming the benchmark. And from this comes the issue of begrudging the expenses. Customers want the bang for their buck. If the fund is not outperforming the benchmark, they would prefer lower expenses and settle for returns somewhere around the benchmark. To put the same point another way, the major advantage of passive funds is that they don’t need to outperform the benchmark index; they simply track it.

When you are investing in a passive fund, you are giving up the chances of getting the alpha, i.e. outperformance of your fund over the benchmark. An active fund can generate alpha even after expenses. However, in a passive fund, you are protecting yourself against underperformance. In an active fund, in case the fund manager’s calls go wrong, you would get significantly lower returns.

Another benefit is that smart beta—where the fund follows an index that is constructed on alternative rules—is available in passive funds. If you want to go beyond the ubiquitous Nifty 50, Nifty 500, or BSE Sensex, you can invest in passives based on factors. If you wish to diversify your investments abroad, passive products are available. Then what gives?

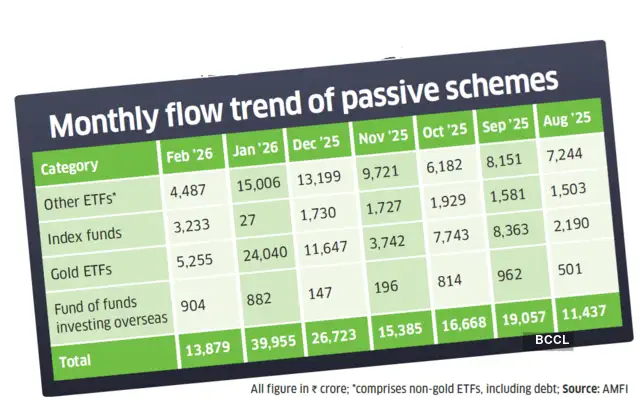

Monthly flow trend of passive schemes

All figure in Rs.crore; *comprises non-gold ETFs, including debt; Source: AMFI

What’s holding back

n Awareness: It may seem counterintuitive that in today’s age of the internet and free flow of information and views, we are talking of awareness as a limitation. Financial literacy is limited to tier-1 locations, and certain pockets of tier-2 and tier-3 areas. The awareness that passive funds run on lower expenses and protect you from the downside of a fund manager underperforming the index is limited.

The AMFI-CRISIL Factbook proves this point: as of March 2024, nearly 80% of passive fund AUM was held by corporate investors. Individual investors held just 19.4%—13.8% with HNIs and 5.6% with retail. The skew in the holding pattern indicates individuals are largely invested in actively managed funds.

n Optimism: Investors opting for active funds, or even being aware of passives and lower expenses, have a positive expectation that their fund will outperform the benchmark, post-expenses. Active funds do outperform the benchmark, though the extent is less than 50% of funds. This optimism drives savvy investors towards actives.

Revenue driver: According to AMFI, as of December 2025, around 45% of MF investments are via direct channels. The implication is that the other 55% that comes through the regular plan needs a push. The 45% chunk—which includes corporates (largely liquid funds), HNIs, and a section of retail—is already aware and has availed of lower TER.

The remaining 55% needs the nudge to enter the MF fold. The intermediary, i.e. the mutual fund distributor who will give the nudge, requires incentivisation to make it worth their professional time. Active funds contain this incentivisation, as the expenses are higher.

The methodology for TER and incentivisation of passive funds could be complex, but it is something regulators and stakeholders should give thought to. If the share of passive funds has to be taken up from 18.6% of AUM to anything meaningful, this is worth debating.

Conclusion

There is a debate in the industry over active versus passive. Ideally, it should be both active and passive. Both have their USPs. There are certain categories of funds—e.g. sector, thematic, small cap—where indices are available, but the proclivity is towards alpha, where the role of the fund manager and his/ her skills becomes relevant. Investors can follow the core-satellite approach.

For wealth accumulation over a long horizon, large-cap funds are more relevant, where the scope for the fund manager to outperform is limited. This may form the core of your portfolio, where passive funds can save your expenses. For tactical allocation, with a little higher risk-return exposures, e.g. small cap or thematic funds, there is a scope for the fund manager to outperform, as the information availability is not perfect. This may serve as the satellite of your portfolio, where active funds can generate alpha.

The Author is Corporate Trainer(Financial Markets) and Author

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment