")

Roman Tiraspolsky

Let’s drift into the mortgage arena and discuss what’s waiting in the wings for the Blackstone Mortgage Trust, Inc. (NYSE:BXMT).

For those unaware, we covered various components of Blackstone (BX) extensively in the past week, including the company as a whole its Blackstone’s Apartment Income REIT Corp. (AIRC) acquisition. However, today’s analysis builds on a statement we made a week ago when assessing Blackstone’s real estate portfolio, which claimed that negative interest rate duration risk would dent the firm’s mortgage business. The mortgage business we referred to was, of course, Blackstone Mortgage Trust.

Without further ado, let’s traverse into the reasons why we think the Blackstone Mortgage Trust is a Hold.

Recent Performance

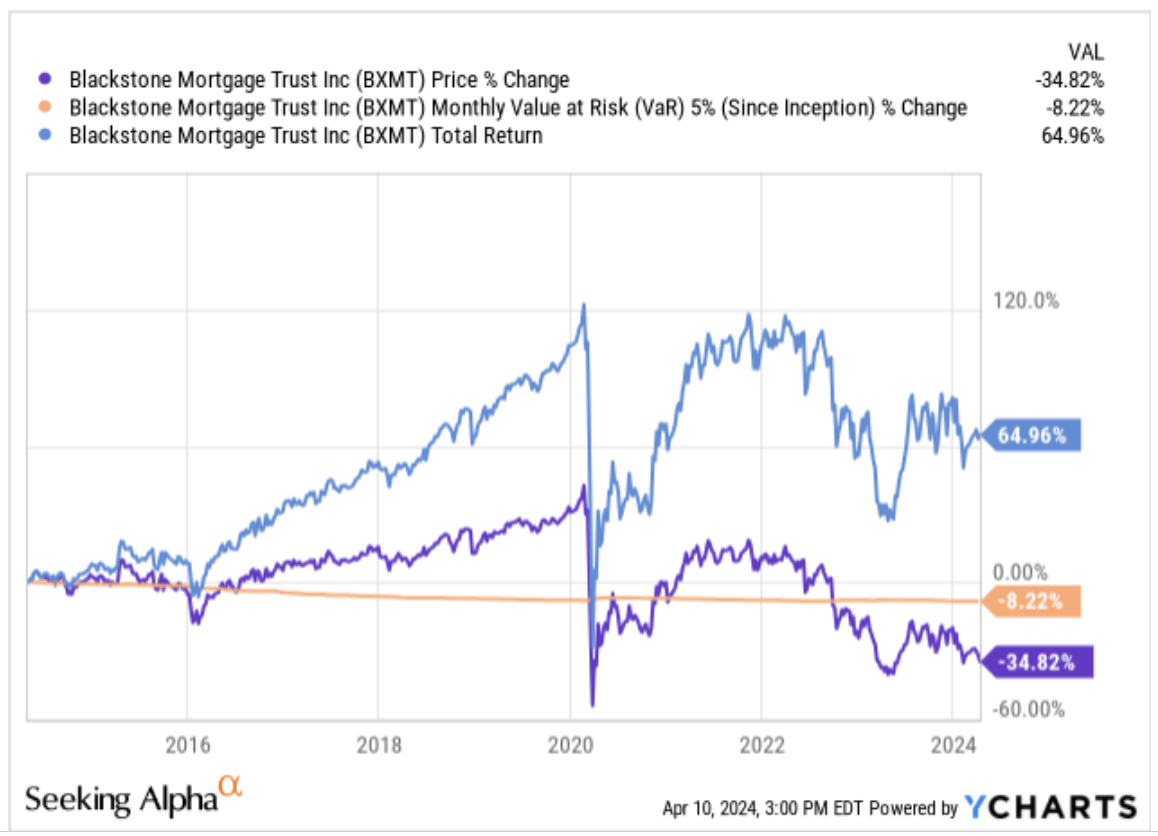

A look at Blackstone Mortgage Trust’s recent performance shows that it has shed approximately 12.2% of its value since the turn of the year. Although its dividend has helped it trim those losses, the asset’s net return indicates faultlines have emerged.

Seeking Alpha

In our view, Blackstone Mortgage Trust suffered from systematic features. The market has anticipated lower interest and mortgage rates for quite some time, which likely led to repositioning. However, Blackstone Mortgage Trust could make amends as it is set to release its earnings on April 24th.

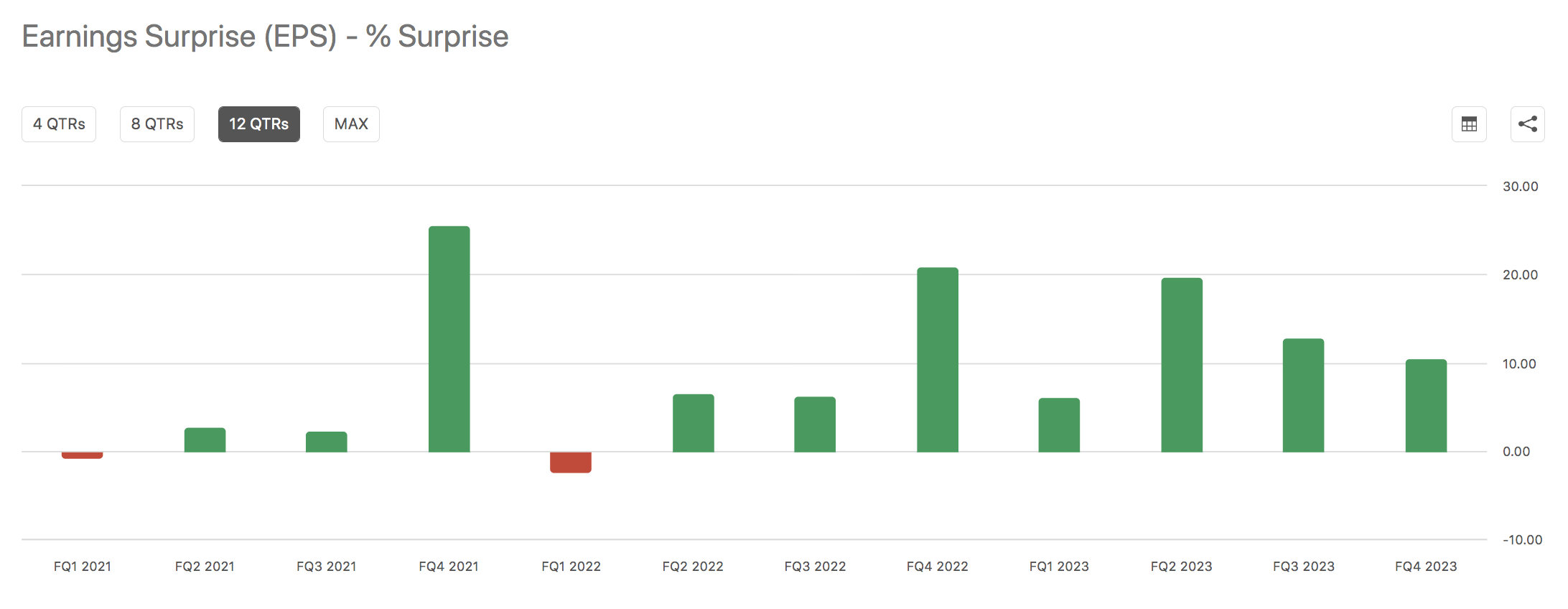

This vehicle has triumphed in each of its past seven quarters, beating earnings comprehensively. Mortgage and interest rates have remained high since Blackstone’s latest earnings release. Therefore, we won’t be surprised if the vehicle reaches its GAAP EPS estimate of 46 cents.

Seeking Alpha

Despite its temptation, trading BXMT prior to earnings would be a tactical play. If you’re not interested in tactical bets, stay tuned as we conduct a comprehensive fundamental analysis.

A Fundamental Assessment

Asset Base

Let’s start off the fundamental part of this analysis by discussing Blackstone Mortgage Trust’s asset base.

As visible in the diagram below, Blackstone Mortgage Trust is geographically and sector-diversified. However, most of the vehicle’s exposure relates to the U.S. office and general multifamily credit markets.

Blackstone Mortgage Trust

Although Blackstone Mortgage’s portfolio is well-diversified, we remain concerned about two components: 1) declining yield curves and 2) The likelihood of reserve increases.

Although the U.S. March CPI settled hot at 3.5%, the year-over-year trend is in decline. Moreover, as illustrated by the following GDPNow diagram, the U.S. economic forecast is uncertain. In fact, we believe the U.S. economy is set to enter a natural softening period later this year due to the peak interest rate effect paired with real economic factors such as wavering business inventories and a potential pivot in consumer confidence.

A similar theme might occur in the vehicle’s other primary regions. In fact, inflation is already tapering steadily in the UK, Europe, and Australia, providing a leading indicator of what’s ahead.

GDPNOW (Atlanta Fed)

Considering the aforementioned, we believe price levels will continue to decline, leading to lower yield curve levels and, ultimately, lower interest rates.

U.S. Yield Curve (worldgovernmentbonds.com)

Lower yield curves might spell danger for mortgages as variable interest mortgages often possess negative duration, meaning their values are positively correlated to interest rates. Sure, as revealed later, other factors do play a role. However, interest rate sensitivity is salient.

Blackstone Mortgage Trust’s material doesn’t convey duration statistics. Therefore, I collated key metrics and computed an effective duration myself. The data is visible in the following diagram, showing that Blackstone Mortgage Trust’s current interest rate sensitivity is likely around 2.23% for a 1% parallel shift in interest rates.

Note: The formula used for the effective duration was Portfolio Maturity/(1.All-in-Yield) = Modified Duration/(1.All-in-Yield) = Effective Duration.

| Metric | Value |

| Portfolio Avg. Maturity | 2.4 yrs |

| Portfolio All-In-Yield | 3.66% |

| Effective Duration Estimate | 2.23x |

Source: Blackstone Mortgage Trust

Furthermore, Blackstone Mortgage Trust is at risk of tying up capital. The fund has already increased its reserves throughout the past year to adjust according to economic risk/market risk. We anticipate further economic uncertainty to occur in the following quarters, meaning additional reserves may be required, potentially detracting from Blackstone Mortgage Trust’s profitability.

Blackstone Mortgage Trust

On a more positive note, we think Blackstone Mortgage Trust’s diversification could yield significant benefits throughout the next few quarters. Additionally, given the subsector’s absorption and occupancy difficulties, Blackstone Mortgage Trust has an opportunity to lock in lucrative yields on its office exposure due to heightened subsector risk.

Portfolio Details (Blackstone Mortgage Trust)

Financing

Assessing assets without considering their adjacent liabilities limits the research’s scope, especially as Blackstone Mortgage is leveraged by 3.2x.

Blackstone Mortgage Trust’s debt maturity schedule shows that term loans expiring in 2026 and 2029 make up the majority of its debt. Moreover, the fund has convertibles and senior secured notes expiring in 2027.

Debt Maturity Schedule (Blackstone Mortgage Trust)

A look at Blackstone Mortgage Trust’s traditional loans illustrates a net interest margin of 1.69%. We mentioned the negativity convexity risk earlier; however, it must be noted that Blackstone Mortgage’s funding costs can decrease in the event of lower short-term yields. As such, it somewhat neutralizes our aforementioned argument.

Financing (Blackstone Mortgage Trust)

Furthermore, Blackstone Mortgage Trust finances some of its asset base with collateralized loan obligations. The obligations might end up increasing in cost in the event of lower interest rates due to a likely credit spread spike. However, we remain somewhat neutral here as the tradeoff between interest rates and credit spreads can be difficult to predict.

CLO Loans (Blackstone Mortgage Trust)

Lastly, consideration must be given to Blackstone Mortgage Trust’s access to equity capital. Blackstone Mortgage Trust operates under Blackstone and, therefore, has substantial access to equity recapitalization if necessary.

Valuation and Dividends

As shown in the diagram below, dividends are the primary contributor to Blackstone Mortgage Trust’s returns. However, the MREIT’s 5% monthly value-at-risk of 8.22% suggests tail risk is prevalent, warranting close consideration of price risk.

Aside: A 5% monthly VAR of 8.22% means the asset loses 8.22% or more in 5% of its trading months.

Seeking Alpha; YCharts

Blackstone Mortgage’s 2023 book value per share (after dividends) settled at $25.16, giving its stock a price-to-book ratio of about 0.75x, which in isolation looks brilliant. In fact, there’s little to dispute its price-to-book ratio. However, as visible below, many of BXMT’s peers have similar price-to-book ratios (or even lower), suggesting little relative value is in store.

Furthermore, as discussed earlier, duration could soon be a problem in the MREIT space, which is why we don’t buy into MREITs being systematically undervalued. To elaborate, negative duration and economic effects could compress the vehicle’s net book value, which is why we are hesitant to deem the asset undervalued. Instead, we would say the amalgamated variables (including a peer-based comparison) places this asset in fair value territory.

Seeking Alpha

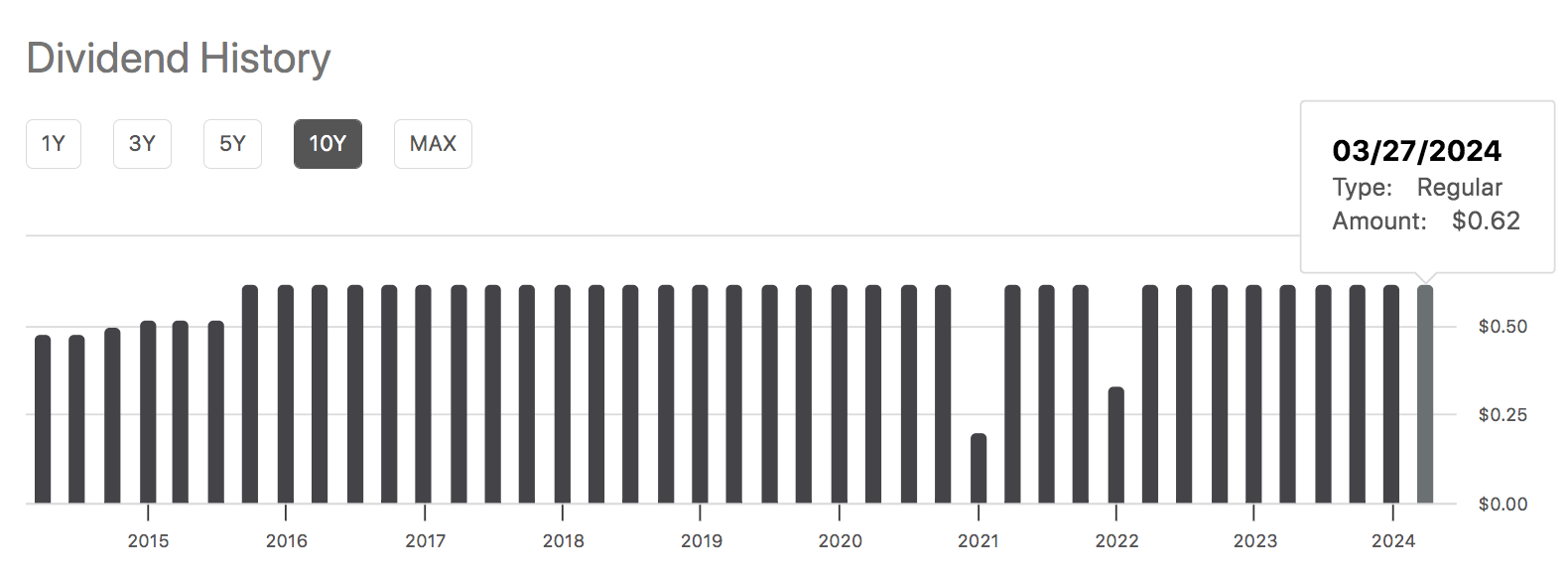

Furthermore, Blackstone Mortgage has a consistent history of paying dividends, as shown by the diagram below and its 5-year yield on cost of 7.19%. Thus, Blackstone Mortgage Trust is a solid income-generating asset.

Seeking Alpha

Final Word

Okay, so Blackstone Mortgage’s key metrics aren’t bad; the economic environment is uncertain but not disastrous; can’t I just buy BXMT for its dividends? I’m not here to tell you what you can and cannot buy. However, in our view, an interest rate pivot will eventually occur this year and compress Blackstone Mortgage’s book value due to a negative duration effect. Although we anticipate Blackstone Mortgage’s dividend yield to add a floor to its market price, we think investors would be better served looking elsewhere until Blackstone Mortgage Trust suffers a correction.

Consensus: Hold/Neutral