One of the best ways to make money in the stock market is to buy and hold high-growth companies over the long run. After all, growth stocks represent companies capable of growing earnings faster than the broader market, and this usually translates into healthy stock price upside.

We are going to take a closer look at two such growth stocks — Applied Digital (APLD 3.66%) and Western Digital (WDC +0.22%) — that you can buy with just $500 in investible cash (after meeting your expenses, clearing high-interest debt, and saving for difficult times). You can consider putting that money into these stocks, either individually or combined, and expect solid long-term gains.

Image source: Getty Images.

Applied Digital: Building data centers for an artificial intelligence (AI) world

The demand for dedicated artificial intelligence (AI) data centers is rising rapidly. From hyperscalers to AI companies, everyone is looking to get their hands on computing capacity to run AI workloads in the cloud.

Today’s Change

(-3.66%) $-1.33

Current Price

$35.02

Key Data Points

Market Cap

$10.0B

Day’s Range

$34.82 – $38.52

52wk Range

$4.20 – $42.27

Volume

1.1M

Avg Vol

23M

Gross Margin

27.07%

Applied Digital is benefiting big-time from the booming AI data center demand. After all, the company is in the business of designing, constructing, and operating dedicated AI data centers for hyperscalers and neocloud companies. Not surprisingly, Applied Digital has witnessed stunning revenue growth.

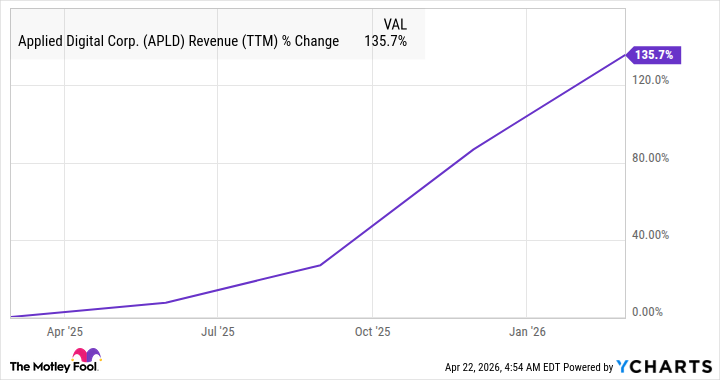

APLD Revenue (TTM) data by YCharts

Its top line jumped by 139% year over year in the third quarter of fiscal 2026 (which ended on Feb. 28) to $126.6 million. That figure is poised to accelerate significantly as it completes construction of its data center facilities. After all, Applied Digital already has a $16 billion contracted lease revenue pipeline from CoreWeave and another hyperscaler for 15 years.

The company is building 400 megawatts (MW) of data center capacity for CoreWeave, along with another 200 MW for another hyperscaler. It recently completed construction of 100 MW of data center capacity for CoreWeave, which means it has started generating lease revenue from this site. The completion of the remaining 500 MW of capacity for these two customers should further accelerate Applied Digital’s growth.

Even better, Applied Digital is focused on expanding its business and recently broke ground on a new data center campus in the southern U.S. The company points out that this facility can handle up to 300 MW of “high-density AI workloads, with initial operations expected to begin in mid-calendar 2027.” So, it is easy to see why analysts are expecting its revenue growth to take off.

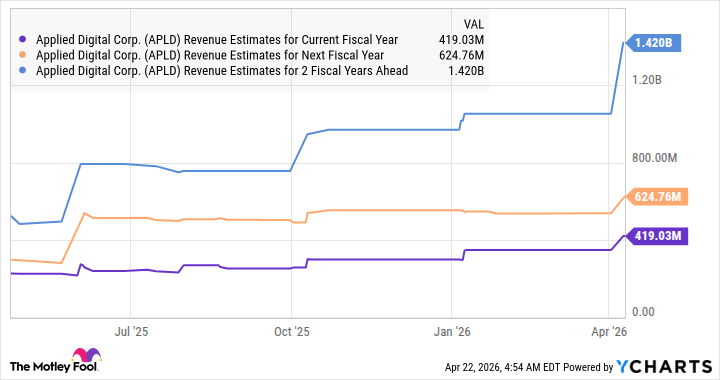

APLD Revenue Estimates for Current Fiscal Year data by YCharts

Not surprisingly, Applied Digital is rated as a buy by all 13 analysts covering the stock. Its 12-month median price target of $43 points to a potential 37% jump from current levels, suggesting that growth-oriented investors can still buy it following the 27% spike in its stock price this year.

Moreover, the significant spike that’s anticipated in Applied Digital’s revenue in the future, driven by its solid lease revenue pipeline and projects under development, could pave the way for bigger gains in the long run. All this makes this AI stock worth buying before it soars higher.

Western Digital: Severe shortage of storage drives should propel the stock higher

Shares of storage technology provider Western Digital have soared 123% in 2026, as of this writing. The stock’s stunning surge is the result of remarkable growth in its revenue and earnings, fueled by a favorable demand-supply situation in its end market.

The hard-disk drives (HDDs) that Western Digital manufactures are in red-hot demand in AI data centers, where they are being deployed to store the huge amounts of data needed to run AI workloads. Market research company IDC estimates that global data generation could triple between 2024 and 2029.

Today’s Change

(0.22%) $0.88

Current Price

$404.00

Key Data Points

Market Cap

$137B

Day’s Range

$400.05 – $414.50

52wk Range

$40.18 – $416.37

Volume

5.6M

Avg Vol

9.4M

Gross Margin

42.68%

Dividend Yield

0.11%

As a result, AI data centers have been buying up HDDs, as they enable them to store data cost-effectively. However, the incredible demand from this segment has created a severe shortage of HDDs. Western Digital has already sold out its HDD capacity for 2026. Its customers are now entering into supply agreements for 2027 and 2028 to secure HDD capacity, suggesting the shortage will continue.

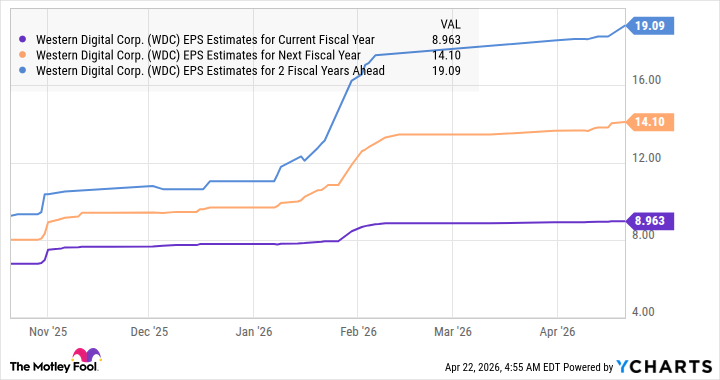

So, there is a solid chance that the price hikes in the HDD market are here to stay as demand outpaces supply. This explains why Western Digital’s bottom line is poised for a massive jump from last fiscal year’s level of $4.93 per share.

WDC EPS Estimates for Current Fiscal Year data by YCharts

Assuming Western Digital’s earnings indeed jump to $19.09 per share after a couple of fiscal years, and it trades at 32 times earnings at that time (in line with the tech-laden Nasdaq-100 index’s earnings multiple), the stock could reach $611. That’s a potential jump of 57%, which is why investors would do well to add this tech stock to their portfolios before it is too late.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment