The black in your car’s tyres is not painted. Raw rubber is naturally pale and would crack within weeks without reinforcement.

That reinforcement is carbon black. It makes up nearly a third of a tyre’s tread, giving it strength, durability, and wear resistance. Without it, modern tyres and many industrial rubber products simply would not exist.

India produced over 200 million tyres last year, and a significant share of the carbon black used in them came from one company – PCBL Chemical Limited.

Source: http://www.tradingview.com

PCBL is India’s largest and the world’s seventh-largest carbon black producer. It operates four plants, generates power from furnace waste gas, and supplies almost every major Indian tyre manufacturer.

For decades, it was known as Phillips Carbon Black. Then things changed.

In 2021, the company became PCBL Limited. In 2024, it renamed itself PCBL Chemical Limited. Dropping ‘carbon black’ from its name signalled a much broader ambition.

In January 2024, it acquired Aquapharm Chemicals Ltd, among the top three global phosphonates players. However, since then, the stock has been down about 24% from its 52-week high.

FY26 was one of its weakest years in recent history, with EBITDA down 22%, profit more than halving, and its chemicals business slipping into a quarterly loss.

So is PCBL still just a cyclical carbon black company, or a chemicals company, or is it one whose transformation the market is genuinely missing?

Let’s dig in.

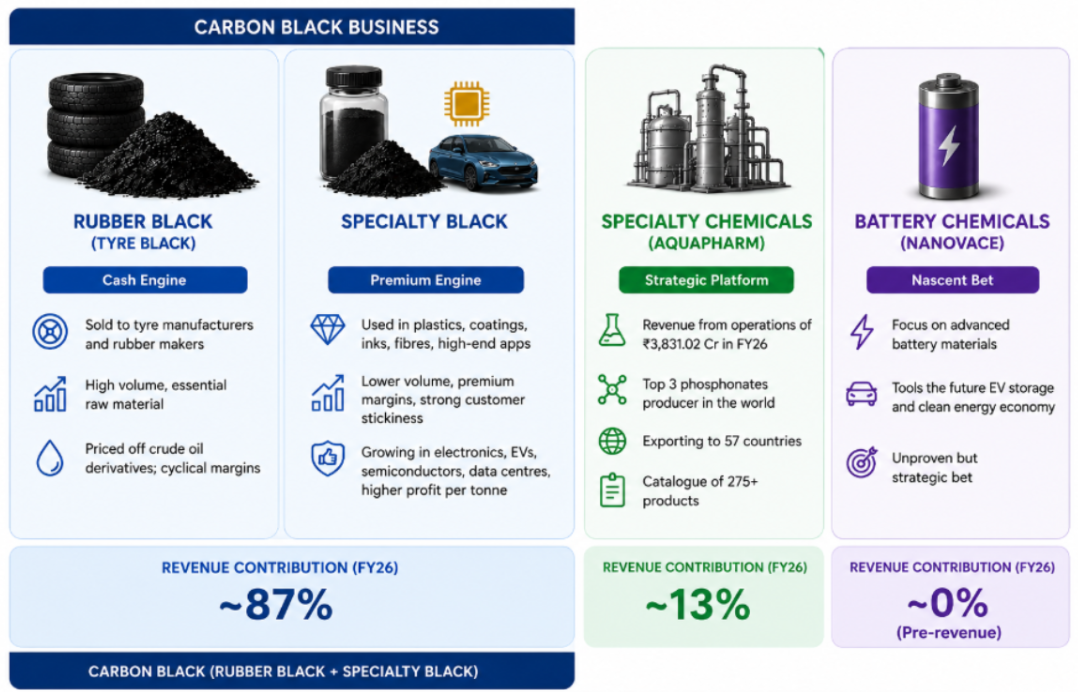

Understanding what PCBL sells

Before assessing the opportunity, let’s understand the company’s four business segments.

Source: Author illustrations

Firstly, carbon black is not a single commodity. It spans two distinct segments.

The first is rubber black, or tyre black, sold to tyre manufacturers. It’s a high-volume business with margins tied to crude oil derivatives. This is PCBL’s cash engine.

The second is specialty black, used in plastics, coatings, inks, fibres, and increasingly in semiconductors, EVs, and data centres. Volumes are lower, but margins and customer stickiness are much higher.

Beyond carbon black are two newer business segments.

- Specialty chemicals, acquired through Aquapharm in 2024. The business makes phosphonates for water treatment, detergents, and oil and gas, making PCBL one of the world’s top three phosphonate producers.

- The second is battery chemicals under Nanovace. It is the company’s newest and most speculative growth platform, and we’ll explore it shortly.

So the real PCBL is four things stacked on top of each other:

- A large, cyclical rubber black business throwing off cash

- A smaller, higher-margin specialty black business riding the electronics and EV wave

- A recently bought specialty chemicals platform in phosphonates

- And an unproven but ambitious bet on battery materials.

The transformation thesis is about shifting the centre of gravity from the first to the rest.

The cash engine everyone underrates

It is easy to dismiss carbon black as a commodity. That misses what PCBL’s core business really is.

Carbon black generated around Rs 6,512 crore of revenue in FY26 and continues to fund the company’s newer growth businesses. Its captive power plants, fuelled by furnace tail gas, provide a structural cost advantage that smaller competitors struggle to match.

The moat is built on scale, capital intensity, and customer stickiness.

The business is still expanding. PCBL sold a record 618,956 tonnes in FY26, with domestic volumes up 9% and specialty volumes continuing to grow. A new 90,000-tonne expansion has lifted capacity to about 880,000 tonnes, with management targeting one million tonnes by FY27-FY28.

But record volumes did not translate into record profits. FY26 was all about that disconnect.

The year the margins broke

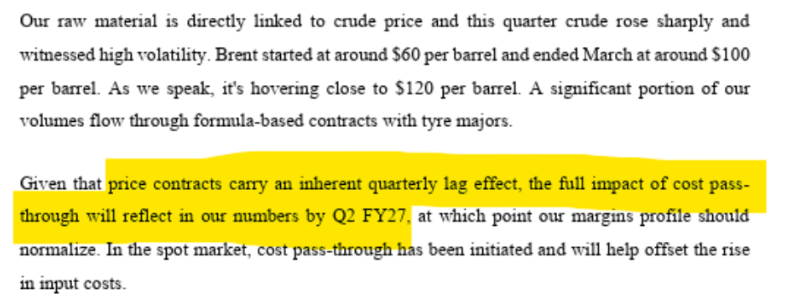

FY26 was a year when almost every cost head moved against PCBL. Crude oil, the key determinant of carbon black feedstock costs, remained elevated for much of the year.

Since carbon black is largely sold on contracts that lag input costs, higher feedstock prices squeezed margins before selling prices could adjust.

Dependence on Crude prices

Source: Q4 FY26 concall transcript

At the same time, the conflict in West Asia disrupted trade routes, driving up freight costs and hurting exports. Intense competition in overseas markets added further pressure.

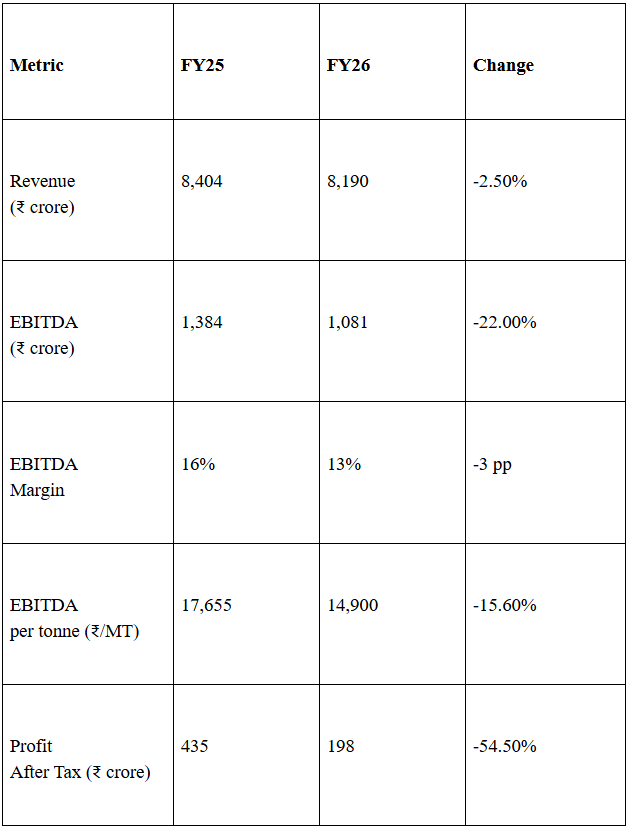

The financials reflect that reality.

Summarised Financials

Source: http://www.screener.in/company filings

The carbon black business illustrates the challenge. FY26 was a year of record sales volumes but weaker profitability, with segment PBIT declining from Rs 1,042 crore to Rs 721 crore as rising feedstock costs temporarily outpaced price pass-through.

This is why FY26 can be interpreted in two very different ways.

The bearish view is that PCBL Ltd is a commodity business whose earnings remain hostage to crude prices. The bullish view is that it’s a cyclical trough driven by temporary external shocks, even as the company demonstrated record demand for its products.

Both interpretations have merit, which is why the next three developments matter far more than FY26 itself.

The diversification: Phosphonates and Aquapharm bet

The clearest signal of PCBL’s transformation was its Rs 3,800 crore acquisition of Aquapharm in January 2024.

Aquapharm makes phosphonates, specialty chemicals used in water treatment, detergents, and oil and gas applications. The deal made PCBL one of the top three phosphonate producers globally.

Like carbon black, this is a qualification-led business where customers rarely switch suppliers once products are approved.

The strategic rationale is straightforward. Aquapharm was acquired to reduce PCBL’s dependence on the cyclical carbon black business. Specialty chemicals are less exposed to commodity cycles, offer higher margins, and benefit from long-term demand driven by water treatment, industrial cleaning, and energy.

Aquapharm Chemicals: End-user industries

Source: Author illustration

In FY26, however, Aquapharm did not deliver.

The specialty chemicals business generated around Rs 1,443 crore of revenue, but EBITDA declined from Rs 194 crore to Rs 162 crore as weakness in oil and gas weighed on demand. In Q4, the segment even reported a small operating loss.

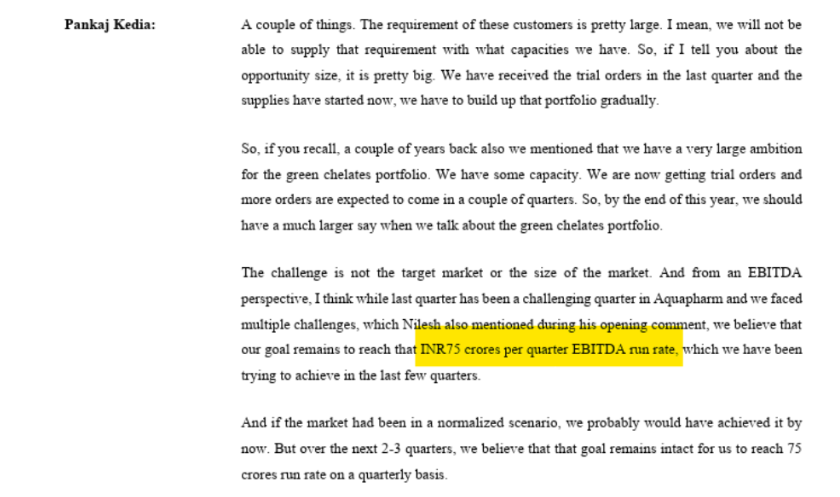

Management expects a recovery, guiding for a quarterly EBITDA run rate of about Rs 75 crore and 20-25% revenue growth in FY27, supported by green chelates (chemicals used to soften water) and improving oil and gas demand.

PCBL Chemicals Ltd’s conference call excerpt

Source : Q4 FY26 concall transcript

The competitive moat remains intact; the key question is execution and end-market recovery.

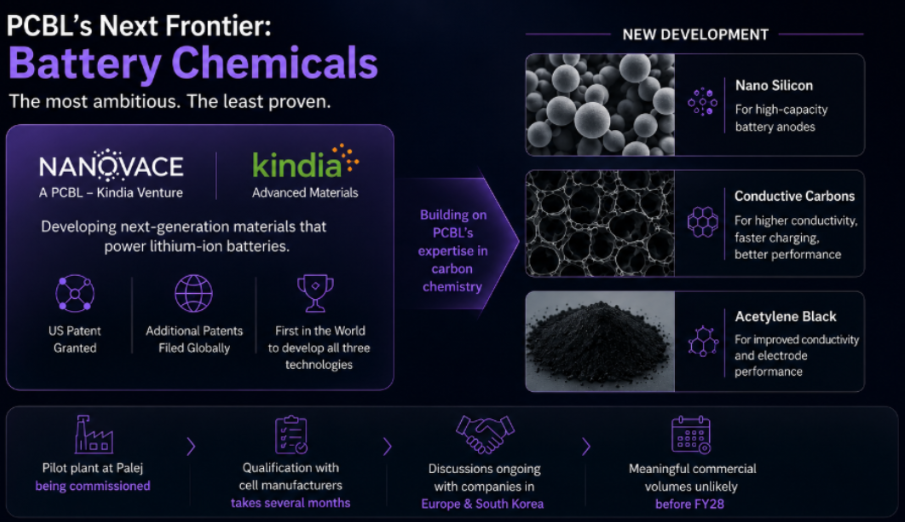

The optionality bet: Nanovace and the battery chemicals

Battery chemicals are PCBL’s most ambitious and, simultaneously, the least proven bet.

Through its joint venture, Nanovace, with Australia’s Kindia, the company is developing lithium-ion battery materials, including nano-silicon anodes, super-conductive carbons, and acetylene black.

It has secured a US patent for its nanomaterial process and filed several more globally.

The strategy is logical. PCBL’s expertise in carbon chemistry, combined with the rapid growth of India’s EV and energy storage markets, positions the company to benefit from rising demand for high-value battery materials.

Source: Author Illustrations

For now, this is a future opportunity, not a profit driver. The pilot plant at Palej is only just being commissioned, and qualifying battery materials with cell manufacturers takes time. Commercial production is therefore unlikely before FY28.

Nanovace contributes virtually nothing to earnings today. Its value lies in its long-term potential. If even one of its technologies succeeds commercially, PCBL’s growth story could extend well beyond carbon black. If not, the downside is limited because the market is not assigning much value to the business today anyway.

The specialty black bridge

Between PCBL’s legacy business and its future ambitions sits specialty black, arguably its most overlooked growth driver.

Built on the same carbon black expertise, specialty black serves plastics, coatings, inks, electronics, EVs, and data centres, while earning higher margins than tyre black. PCBL has expanded specialty capacity to around 132,000 tonnes from 112,000 tonnes at Mundra and added a 1,000-tonne superconductive specialty black line at Palej.

Unlike battery chemicals, this opportunity requires no leap of faith. The technology is proven, demand already exists, and every shift from commodity to specialty black improves margins. As utilisation rises through FY27, it should steadily strengthen profitability.

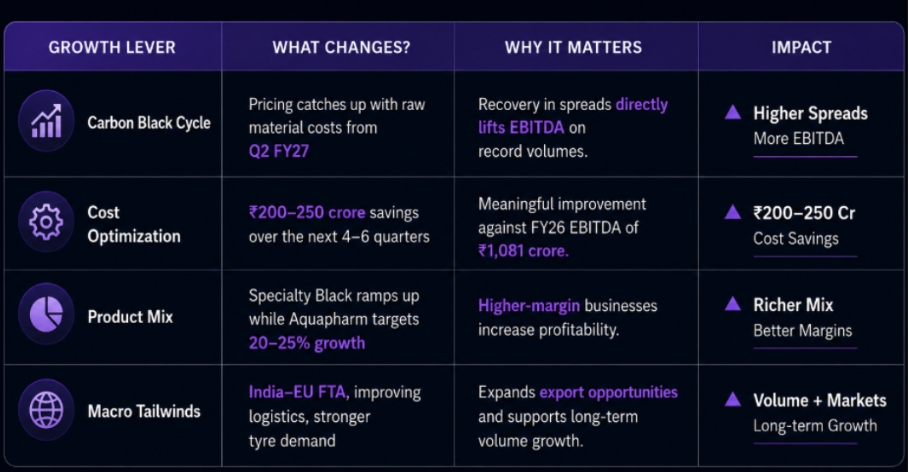

The inflection case

The bull case for PCBL is not that one business suddenly transforms the company. It is that several independent levers begin working at the same time, creating operating leverage on a cost basis that does not need to grow significantly.

Source: Author illustration

Each of these drivers is meaningful on its own. Together, they could create an earnings inflection.

Management expects double-digit EBITDA growth in FY27, outpacing the high single-digit volume growth anticipated in the carbon black business. The improvement is expected to come from recovering spreads, lower costs, and a richer product mix rather than simply selling more tonnes.

The balance sheet also provides confidence. Despite investing nearly Rs 750 crore in capex during FY26, PCBL reduced net borrowings by Rs 454 crore to Rs 4,536 crore. That is a sign of disciplined capital allocation. The company is investing aggressively for future growth while strengthening its financial position, giving it the flexibility to benefit when industry conditions improve.

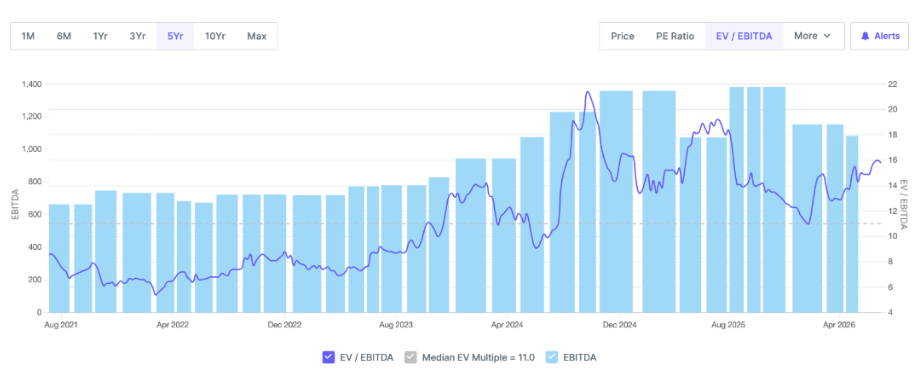

Valuations

At the current market price, PCBL trades at roughly 15-16x FY26 EV/EBITDA, which is above its 5-year median multiple of 11x. On the surface, that appears expensive for a company whose earnings contracted during the year.

But FY26 was a margin trough rather than a normal earnings year, making the trailing multiple a poor indicator of intrinsic value.

EV/EBITDA multiple chart

Source: http://www.screener.in

While FY26 margins were weighed down by temporary cost pressures, management expects profitability to improve through a combination of spread normalisation, Rs 200-250 crore of structural cost savings, and an increasing contribution from specialty products.

Management expects FY27 earnings to be supported by three levers: normalisation in carbon black spreads, Rs 200-250 crore of cost optimisation initiatives, and a richer specialty product mix.

Disclaimer: What follows is a simple, illustrative if-then exercise to help you think about how the market might value PCBL chemicals on a 1-year forward basis. It is emphatically not a target price.

Assuming these drivers play out as guided, EBITDA could recover to approximately Rs 1,550-1,600 crore in FY27, representing a 43-48% increase over FY26. At the current enterprise value, this implies a forward EV/EBITDA multiple of roughly 12-13x.

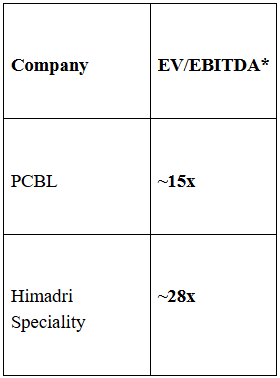

Peer Valuation

Source: http://www.screener.in

*Approximate trailing multiples.

PCBL trades at a premium to global carbon black manufacturers such as Cabot and Orion, although it still trades below Himadri Speciality. This suggests the market no longer views PCBL as a pure commodity carbon black producer.

Instead, investors appear to be assigning value to three factors beyond the base carbon black business:

- The continued expansion of higher-margin specialty black

- The earnings recovery potential at Aquapharm,

- The long-term optionality of Nanovace’s battery materials platform.

Whether this premium is justified ultimately depends on execution. If these businesses scale as management expects, today’s multiples could prove reasonable. However, if Specialty Black growth slows, Aquapharm fails to improve profitability, or Nanovace remains commercially insignificant, PCBL’s valuation could gradually converge toward those of global carbon black peers.

Conclusion

PCBL has built India’s largest carbon black business, acquired a top-three global phosphonates player, expanded specialty black capacity, and entered battery materials.

The company has changed its name, reflecting diversification away from carbon black. Now, it has to prove the business has changed, too.

Disclaimer

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment