With inflation running at 4.2% on CPI, 6.5% on PPI and rate markets now pricing in a possible hike rather than cuts, income investors are suddenly playing a different game. Higher yields and a firm labor market can reward companies that already generate solid cash flow, carry manageable debt and keep dividends on a realistic footing. This article focuses on three stocks from a High Quality Dividend Stocks screener that fit that description and are directly exposed to the current interest rate debate. The goal is to help you think through which income opportunities may still hold up if tighter policy sticks around longer than expected.

Wall Street’s queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab’s valuation page.

Emerson Electric (EMR)

Overview: Emerson Electric is a diversified technology and software company that helps industrial customers run their plants more safely and efficiently using hardware such as valves and sensors alongside automation software that controls and analyzes complex processes in sectors like energy, power, and manufacturing.

Operations: Emerson generates most of its US$18.3b business segment revenue from Intelligent Devices and related segment adjustments at US$15.3b, with Safety & Productivity at US$1.4b and Software and System Test & Measurement at US$1.6b, while Europe contributes US$3.6b of reported geographic revenue.

Market Cap: US$79.6b

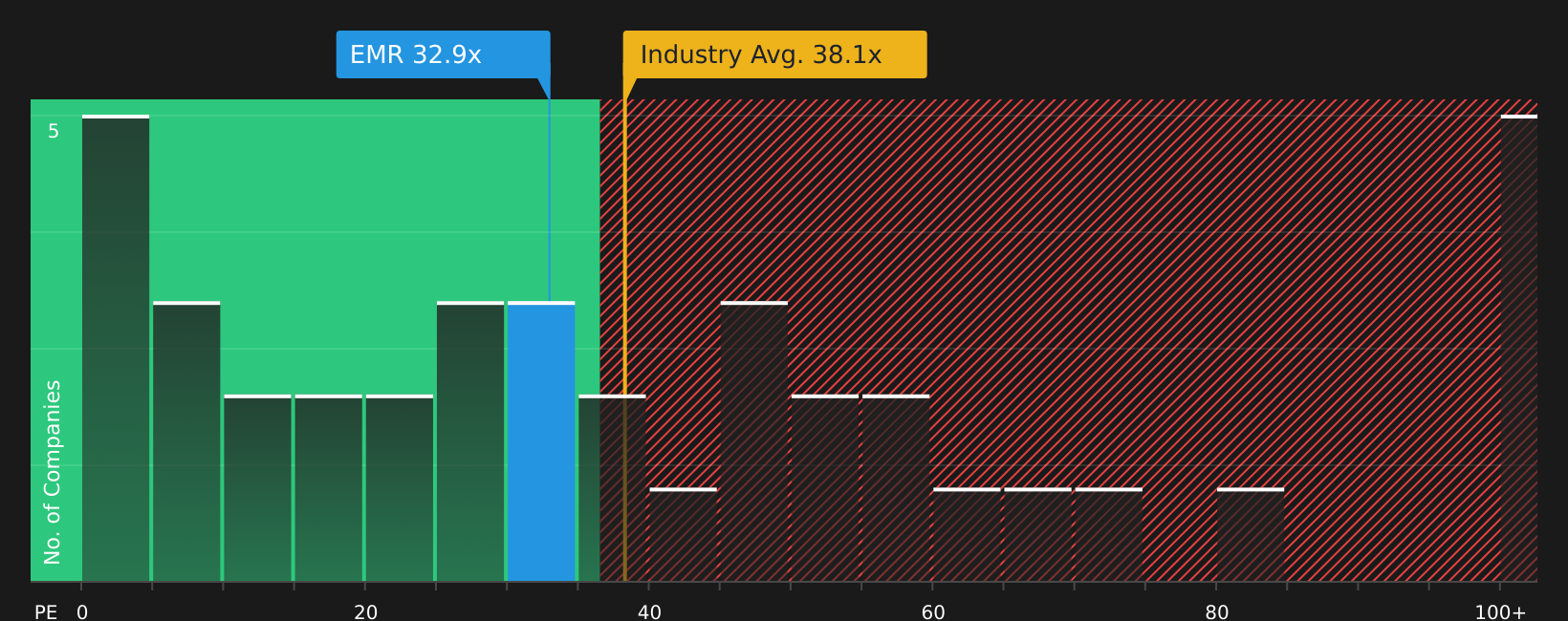

Income focused investors may want to pay attention to Emerson because it combines a long record of dividend growth with exposure to themes such as industrial automation and AI, backed by reported cash generation and margin improvement. Recent partnerships in AI and corrosion monitoring, plus new grid and energy projects, illustrate how its software and hardware are tied to real world infrastructure spending. A P/E below the Electrical industry average and improving profitability indicate that investors may not be overpaying for a mix of stability and growth potential. The potential drawbacks include a debt heavy balance sheet and recent insider selling, so investors may want to weigh the quality of its cash flows and contracts against balance sheet risk and execution on its software plans.

Emerson’s mix of industrial automation, AI partnerships and a P/E below the Electrical industry average suggests the market may be missing something. Start with the 5 key rewards and 2 important warning signs to see what could tip the balance next.

Fastenal (FAST)

Overview: Fastenal is a wholesale distributor of industrial and construction supplies, providing fasteners like bolts, nuts, screws, and washers, along with a wide range of hardware and maintenance products to manufacturers, construction firms, transportation companies, energy producers, and public sector customers across North America and other international markets.

Operations: Fastenal generates US$7.0b in business segment revenue from the United States, with reported geographic revenue of US$7.0b from the United States, US$1.1b from Canada and Mexico, and US$0.3b from other countries.

Market Cap: US$53.3b

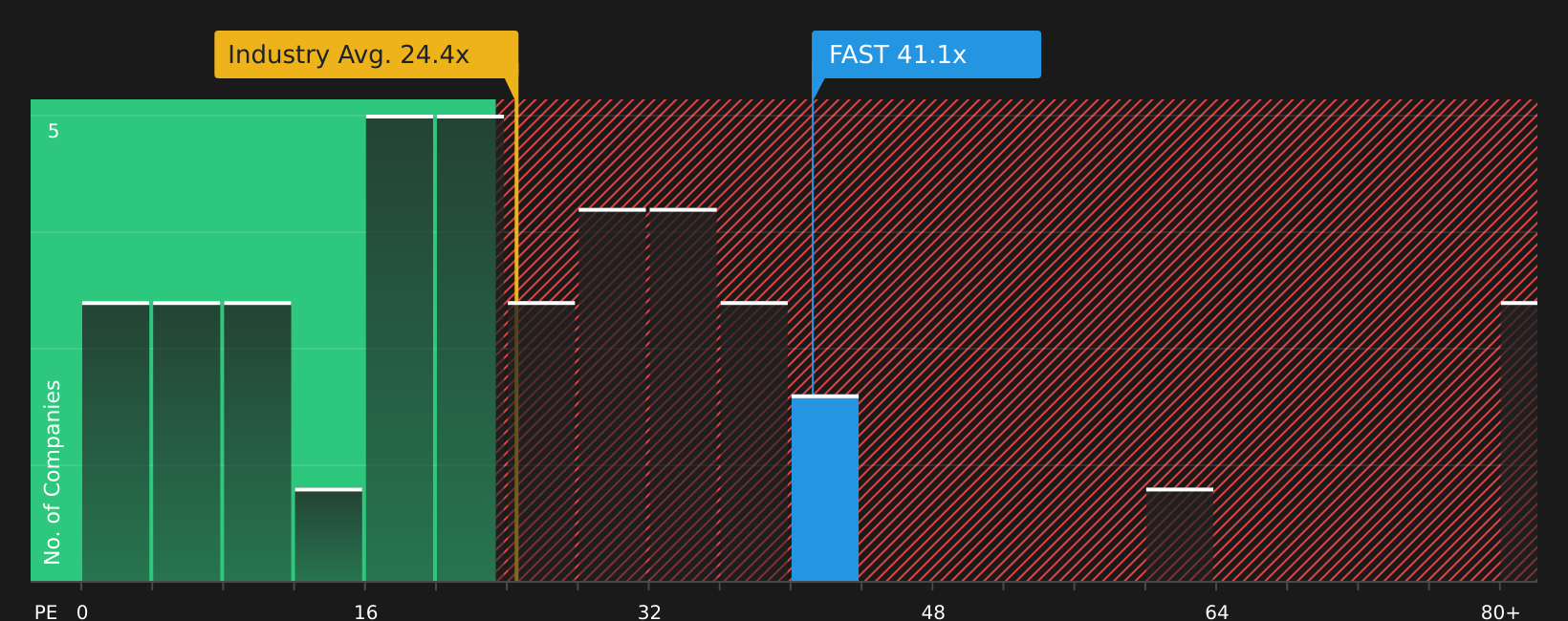

Income investors looking for resilience in a higher rate and inflationary setting may want to look closely at Fastenal, which couples high return on equity and stable profitability with very low debt and a long record of regular dividends. The company’s Fastenal Managed Inventory and growing digital sales help make it a critical supplier for customers that cannot afford supply chain hiccups, which can support pricing when costs and tariffs are rising. At the same time, a rich P/E, dividends that are not fully covered by free cash flow, and sensitivity to industrial demand and trade friction mean you are paying a premium for that perceived quality. The key consideration is whether the balance of cash generation, execution on its Carrollton expansion, and inflation pressures justifies that price.

Fastenal’s rich P/E and low debt profile suggest a quality premium that many investors accept on instinct rather than on numbers. Put that story under the microscope with the analysis report for Fastenal to review what the margin and cash flow detail might be signaling next.

Hubbell (HUBB)

Overview: Hubbell manufactures the electrical components and grid equipment that keep power systems and large facilities running, from utility hardware like insulators and switches to wiring devices, industrial controls and smart metering and communications gear sold worldwide.

Operations: Hubbell generates about US$3.8b of revenue from Utility Solutions and US$2.2b from Electrical Solutions, with US revenue of roughly US$5.6b and additional segment adjustments of US$439.1m.

Market Cap: US$24.8b

If you are looking for income that can hold up while inflation stays stubborn and rates push higher, Hubbell is worth a close look because it pairs high profitability and steady dividend growth with exposure to long term themes such as grid modernization, data centers and electrification. Management talks openly about using pricing to offset cost inflation and tariffs, and recent calls highlight strong traction in passing higher input and freight costs through to customers. At the same time, the NSI Industries acquisition adds scale in electrical components but also layers on new debt. The key question is whether its cash generation, pricing discipline and integration of NSI are strong enough to offset higher interest costs and keep those dividends on solid ground.

Hubbell’s grid and electrification story looks strong, but the real question is how its growth runway stacks up against higher rates and the NSI deal. Weigh that trade off with the analyst forecasts for Hubbell

The three stocks covered here are just a starting point, and the full High Quality Dividend Stocks screener has surfaced 51 more companies with similarly compelling income stories and financial profiles via the High Quality Dividend Stocks screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the dividend ideas that best match your risk tolerance and conviction.

Take Control of Your Investment Journey

If Emerson Electric or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Some of the sharpest breakouts start quietly, then move fast once momentum caught by the crowd sends prices flying. Scan these fresh ideas while it matters and consider them before they move.

- Find potential income workhorses with resilient balance sheets by screening a curated 8 dividend fortresses that aim to keep paying investors while others are dropping their payouts.

- Look at companies building tomorrow’s infrastructure by using the focused 48 AI infrastructure stocks before these picks move from under the radar for now to fully priced momentum stories.

- Explore potential automation leaders with the hand picked 33 robotics and automation stocks to spot businesses gaining traction before their growth stories are widely reflected in prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Emerson Electric might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment