The United States market remained flat over the last week but has seen a 19% increase over the past year, with earnings projected to grow by 18% annually. In this environment, growth companies with significant insider ownership can be appealing as they often indicate strong confidence from those closest to the business, potentially aligning well with future market expectations.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 34.3% | 69.4% |

| Upstart Holdings (UPST) | 14.1% | 60% |

| KVH Industries (KVHI) | 16.2% | 146.1% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| IREN (IREN) | 13.6% | 38.4% |

| ERock (EROC) | 20.1% | 56.3% |

| Corcept Therapeutics (CORT) | 10.9% | 47.8% |

| Cerebras Systems (CBRS) | 10.9% | 73.7% |

| AppLovin (APP) | 23.2% | 21.7% |

| Abeona Therapeutics (ABEO) | 16.2% | 32.9% |

Underneath we present a selection of stocks filtered out by our screen.

Simply Wall St Growth Rating: ★★★★★☆

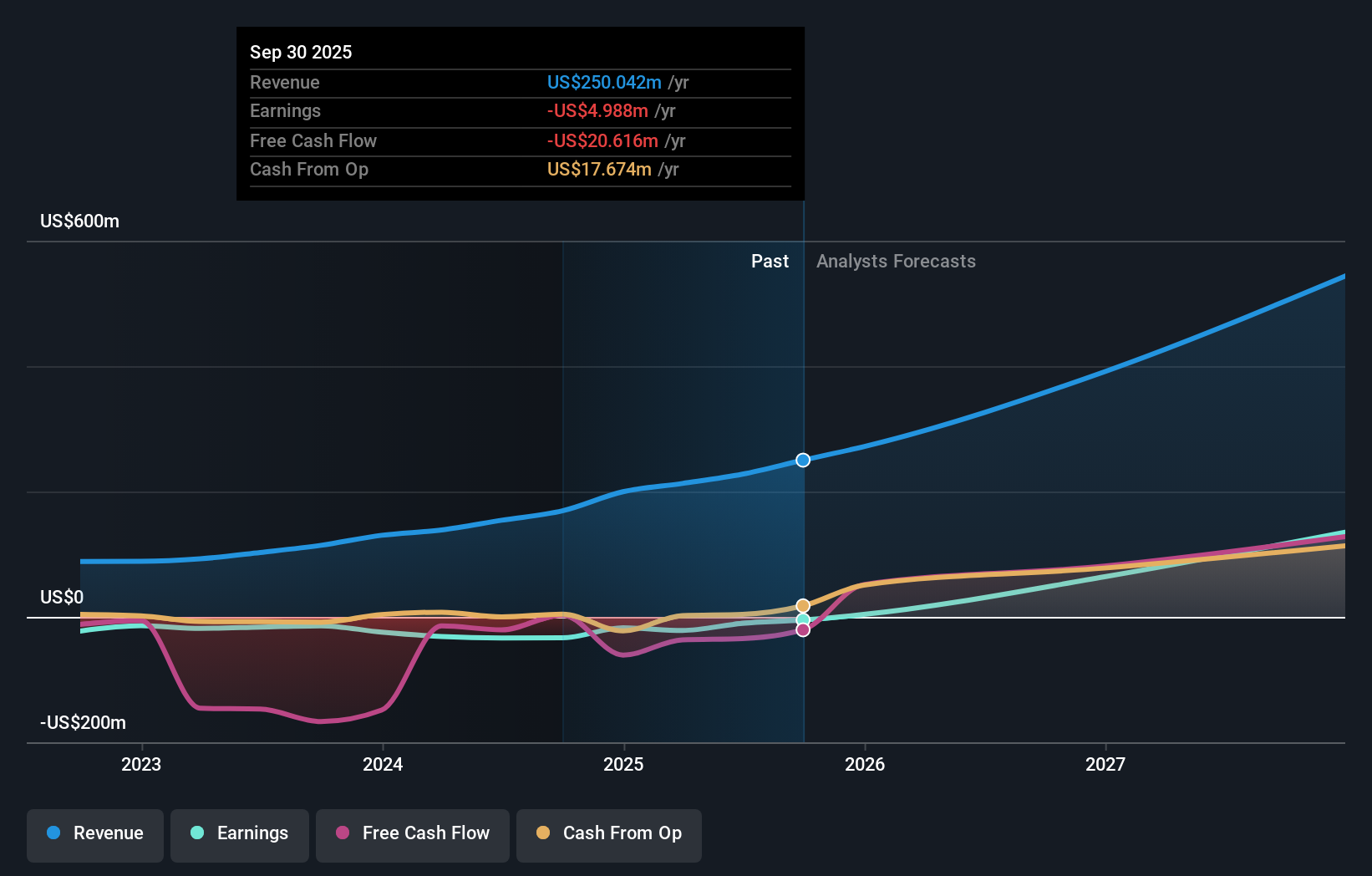

Overview: Harrow, Inc. is a pharmaceutical company focused on the discovery, development, and commercialization of ophthalmic products in the United States with a market cap of $1.60 billion.

Operations: Harrow generates its revenue from two segments: Branded products, contributing $198.68 million, and Compounding products, accounting for $69.99 million.

Insider Ownership: 16.5%

Earnings Growth Forecast: 49.1% p.a.

Harrow is positioned for significant growth, with revenue expected to increase by 26.6% annually, outpacing the US market average. Recent strategic alliances, such as the partnership with Samsung Bioepis for BYOOVIZ commercialization, highlight its expanding footprint in ophthalmology biosimilars. Insider buying activity reflects confidence in its future prospects. Despite a current net loss of US$27.6 million in Q1 2026, Harrow’s forecasted profitability over the next three years suggests robust potential for investors focused on growth companies with high insider ownership.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: AvePoint, Inc. offers a cloud-native data management software platform across various regions including North America, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of $2.78 billion.

Operations: The company’s revenue primarily comes from its Software & Programming segment, which generated $443.68 million.

Insider Ownership: 23.8%

Earnings Growth Forecast: 22.8% p.a.

AvePoint is trading at 32.5% below its estimated fair value, indicating potential undervaluation. The company’s earnings are forecast to grow significantly at 22.8% annually, outpacing the broader US market’s growth. Recent additions to the Russell 2000 Defensive and Growth-Defensive Indexes enhance its visibility among investors. Despite no significant insider trading activity in recent months, AvePoint’s strategic advancements in AI governance and cloud security reflect strong growth prospects amidst a competitive landscape.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Peapack-Gladstone Financial Corporation is the bank holding company for Peapack Private Bank & Trust, offering private banking and wealth management services in the United States, with a market cap of approximately $812.92 million.

Operations: The company’s revenue is derived from two primary segments: Banking, which generates $207.67 million, and Wealth Management, contributing $67.08 million.

Insider Ownership: 11.1%

Earnings Growth Forecast: 36.2% p.a.

Peapack-Gladstone Financial’s insider ownership aligns with its growth trajectory, evidenced by a significant 37.3% earnings increase over the past year and forecasted annual profit growth of 36.25%, outpacing the US market. The appointment of Paul Kotronis as Senior Managing Director aims to bolster their commercial real estate lending platform, enhancing regional presence and deposit growth. Despite substantial insider selling recently, Peapack’s strategic expansion in payment technology supports operational efficiency and competitive positioning in real estate transactions.

Where To Now?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we’re here to simplify it.

Discover if Harrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment