SpaceX (SPCX +0.00%), the aerospace and AI company founded by Elon Musk, will go public on June 12. At its target valuation of $1.77 trillion, it will be the biggest IPO in history.

However, it will also be valued at 95 times its 2025 sales. It’s also reportedly more than four times oversubscribed, which suggests it could start trading at well over 100 times sales. That’s a frothy valuation for an unprofitable company that grew its revenue by 33% last year.

So instead of chasing SpaceX, which looks more like a meme stock with some glaring flaws, it’s smarter to invest in some established growth stocks with clearer long-term catalysts. These two stocks fit that description: Broadcom (AVGO +3.06%) and ASML (ASML +7.26%).

Image source: Getty Images.

Broadcom

Over the past decade, Broadcom has expanded through acquisitions of other chipmakers and infrastructure software companies. The bold strategy transformed it into a more diversified tech company than its peers in the semiconductor and software industries.

Today’s Change

(3.06%) $11.39

Current Price

$383.49

Key Data Points

Market Cap

$1.8T

Day’s Range

$370.77 – $385.59

52wk Range

$244.17 – $495.00

Volume

672.5K

Avg Vol

25.3M

Gross Margin

65.66%

Dividend Yield

0.67%

Broadcom once mainly produced networking, wireless, mobile, and infrastructure chips. But over the past few years, most of its growth has been driven by sales of custom application-specific integrated circuits (ASICs) for the artificial intelligence (AI) market.

Unlike Nvidia (NVDA +1.06%), which produces general-purpose data center GPUs for AI tasks, Broadcom’s AI accelerators are customized for hyperscalers. At scale, these custom chips can handle AI tasks more cost-efficiently than Nvidia’s stand-alone GPUs. Broadcom also locked in its customers by bundling its AI chips with its non-AI chips and infrastructure software.

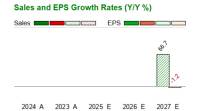

In fiscal 2025 (which ended last November), Broadcom’s AI chip sales surged 65% to $20 billion, accounting for 31% of its top line. It expects its AI chip sales to soar fivefold to over $100 billion in fiscal 2027 (at least 58% of its projected $171.5 billion in revenue).

From fiscal 2025 to fiscal 2028, analysts expect Broadcom’s revenue and EPS to grow at CAGRs of 53% and 66%, respectively, as the AI market expands. Yet its stock still looks surprisingly affordable at 23 times next year’s earnings. So if you’re looking for a simple way to profit from the ongoing AI boom, Broadcom checks all the right boxes.

ASML

Broadcom, Nvidia, and the world’s other top chipmakers couldn’t produce their most advanced chips without the Dutch semiconductor equipment giant ASML. ASML is the world’s largest producer of lithography systems, which are used to optically etch circuit patterns onto silicon wafers. It’s also the only producer of extreme ultraviolet (EUV) lithography systems, which are required to manufacture the world’s smallest, densest, and most power-efficient chips.

Today’s Change

(7.26%) $125.86

Current Price

$1860.05

Key Data Points

Market Cap

$668B

Day’s Range

$1775.51 – $1878.00

52wk Range

$683.48 – $1878.00

Volume

73.7K

Avg Vol

1.8M

Gross Margin

52.60%

Dividend Yield

0.51%

ASML perfected its EUV technology over the past three decades, and its massive machines cost up to $400 million and require multiple planes to ship. All of the most advanced chip foundries — including TSMC, Samsung, and Intel — use those systems to manufacture chips for fabless chipmakers like Broadcom and Nvidia.

ASML’s control of that crucial technology gives it tremendous pricing power and makes it a linchpin of the semiconductor market. It also makes it one of the easiest ways to profit from the insatiable demand for new chips without putting too much faith in individual chipmakers.

From 2025 to 2028, analysts expect ASML’s revenue and EPS to grow at CAGRs of 17% and 26%, respectively. The soaring demand for new AI and memory chips will drive its near-term growth, while its newest high-NA EUV systems (which will enable its foundry customers to manufacture even smaller chips) will drive its longer-term growth. It might not seem like a bargain at 36 times next year’s earnings, but its strengths justify that higher valuation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment