Geopolitical tension, shifting central bank policies, and fresh regulation around banks and technology are reshaping how income investors think about risk and reliability. Dividend growth stocks that pair solid financial health with consistent payouts can offer one way to respond to these cross‑currents, but not all income opportunities are affected in the same way. This article focuses on how the recent news backdrop connects with high‑quality dividend growth candidates, and highlights 3 stocks from our High‑Quality Dividend Growth Stocks screener that may be well positioned relative to these developments.

Charter Hall Group (ASX:CHC)

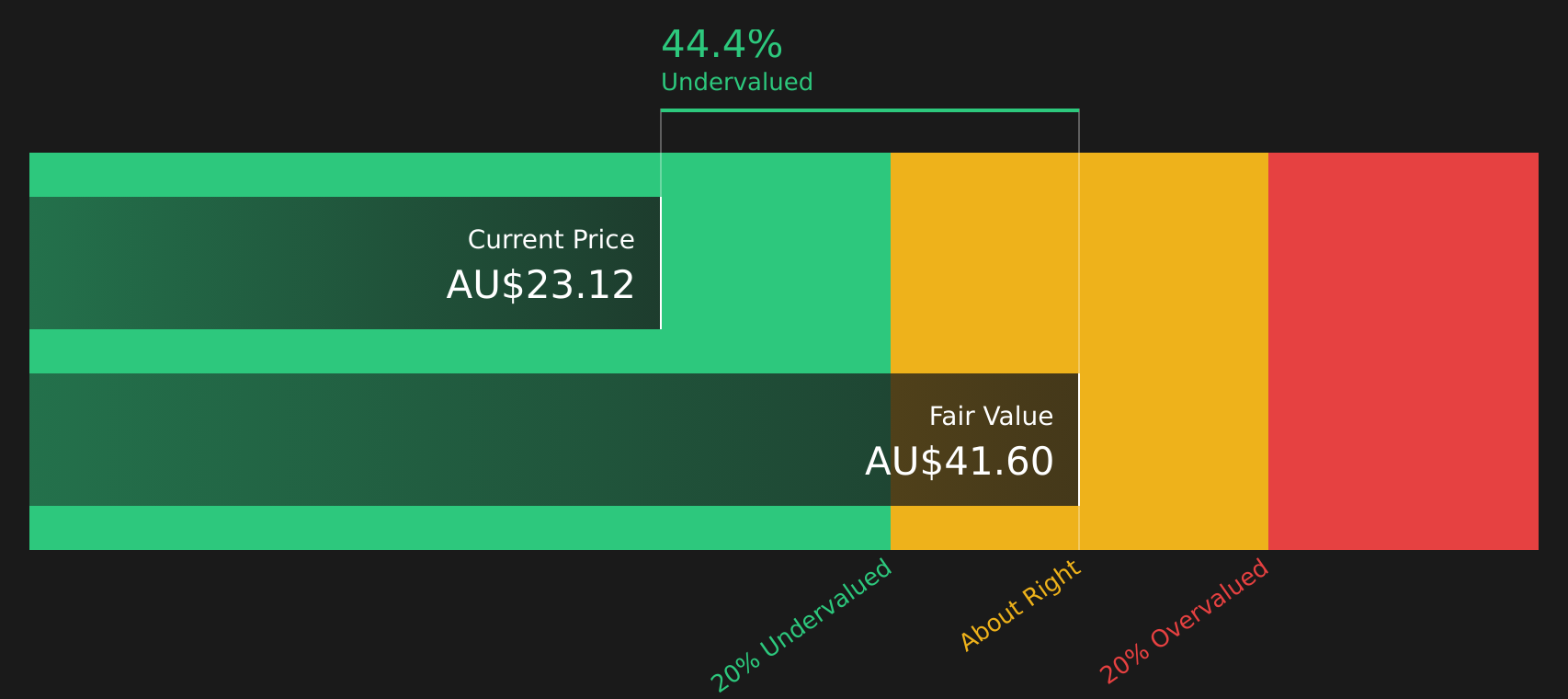

Overview: Charter Hall Group is an Australian property investment and funds management company that pools investor capital into diversified portfolios of office, industrial and logistics, retail, and social infrastructure assets to generate income and long term value. It manages the full property lifecycle, from sourcing and developing assets to ongoing management, for a mix of institutional and individual investors.

Operations: Charter Hall Group generates most of its revenue from funds management at A$433.7 million, followed by property investments at A$387.1 million and development investments at A$90.3 million, with all A$860.7 million of reported revenue coming from Australian assets.

Market Cap: A$10.7b

Income focused investors may find Charter Hall Group interesting because it combines a record of dividend growth with a large, diversified property platform that spans Australian office, logistics, retail and social infrastructure. Recent commentary points to strong institutional interest in Australian property and ongoing equity inflows into its funds, which can support fee income and cash flows. The latest ordinary dividend of A$0.2584 per stapled security underlines its income profile. At the same time, a high P/E multiple and reliance on external borrowing, plus meaningful exposure to office and retail, mean you are paying up for quality and taking real sector and funding risk. How those trade offs stack up for a dividend growth strategy is where the story gets more interesting.

Charter Hall Group’s rich P/E and growing funds platform raise a clear question: is the current premium still justified by the underlying cash flows, or does the real story only appear in the DCF valuation analysis for Charter Hall Group?

Bank of N.T. Butterfield & Son (NTB)

Overview: Bank of N.T. Butterfield & Son is a Bermuda headquartered community and offshore bank that provides everyday banking, lending, and card services alongside wealth management, treasury, and trust solutions to individuals, businesses, and institutional clients across jurisdictions such as Bermuda, Cayman, the Channel Islands, The Bahamas, Singapore, and Switzerland.

Operations: Bank of N.T. Butterfield & Son generates about US$613.1 million in revenue almost entirely from banking activities, with key contributions from Bermuda, Cayman, and the Channel Islands and the UK.

Market Cap: US$2.3b

Income investors looking at Bank of N.T. Butterfield & Son are weighing a 3.41% dividend yield, high 21.2% Return on Equity, and 39.3% net profit margin against banking risks such as a 4% level of bad loans, relatively light loss reserves, and sensitivity to small island economies. The planned US$1.8b acquisition of CIBC Caribbean, record of capital returns through dividends and buybacks, and exposure to fee based wealth and trust services stand out as potential positives as regulators push for stronger, better capitalised banks. A key consideration is how that mix of income, growth forecasts, acquisition execution risk, and credit quality balances out for long term shareholders once the details are reviewed more closely.

Bank of N.T. Butterfield & Son’s mix of a 3.41% dividend yield, 21.2% ROE and 39.3% net profit margin can look like a clean income story, but the real tension sits between that profitability and banking risk in the 4 key rewards and 3 important warning signs

REA Group (ASX:REA)

Overview: REA Group is a digital property company that runs leading real estate portals like realestate.com.au and realcommercial.com.au, connecting buyers, renters, sellers, and agents. It also offers mortgage broking, home loans, property data, and related digital services across Australia and selected international markets.

Operations: REA Group generates most of its revenue from Australia, with A$1.5b from Property & Online Advertising, A$360.8 million from Financial Services, and a A$109 million segment adjustment.

Market Cap: A$17.3b

REA Group may appeal to dividend-focused investors because it combines a dominant online real estate platform with high quality earnings, a net profit margin of 29.3%, and a record of growing dividends that some investors may find attractive when markets are volatile. At the same time, the stock trades on a premium P/E and has recently lagged the broader Australian market, while facing competition, regulatory scrutiny around pricing, and exposure to the property cycle. The case for paying this premium can depend on how investors view its digital moat, expansion into financial services, and India-related initiatives. A key consideration is whether that mix of income characteristics and growth opportunities justifies the current valuation premium in an environment of changing global capital flows and evolving technology regulation.

REA Group’s premium P/E and 29.3% net margin suggest investors may be missing how earnings quality ties into future cash generation. The real twist could sit inside the analysis report for REA Group

The three stocks covered here are just a starting point. The High-Quality Dividend Growth Stocks idea extends across 22 more companies surfaced by the High-Quality Dividend Growth Stocks screener, and each carries its own income profile, balance sheet strength, and risk backdrop. Use Simply Wall St to identify and analyze the specific catalysts, dividend growth histories, and financial narratives that matter most to you so you can focus on the highest conviction opportunities within this group.

Take Control of Your Investment Journey

If Bank of N.T. Butterfield & Son or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves?

Fresh ideas can start breaking out while everyone is still focused on yesterday’s winners. Use these under the radar lists while the information is sharp and take action promptly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment