Energy stocks sit at the crossroads of two powerful forces right now: lower geopolitical risk in the Strait of Hormuz and stubbornly high producer inflation, with May PPI at 6.5% year over year and core producer prices at 5.1%. That mix can reshape input costs, pricing power, and profit margins across the sector. This article looks at how the new U.S. Iran peace agreement and persistent cost pressures might affect a group of U.S. energy companies, and breaks down 3 stocks from the screener that appear positively exposed to these headlines so you can decide whether they fit your watchlist or not.

NOV (NOV)

Overview: NOV Inc. supplies the equipment, components, and technology that keep oil and gas drilling, production, and some industrial and renewable projects running, from drill bits and digital tools to offshore rigs and subsea pipe systems across the globe.

Operations: NOV generates about US$4.9b from its Energy Equipment segment and US$3.9b from Energy Products and Services, with a small offset of US$0.2b from eliminations and corporate.

Market Cap: US$6.7b

Investors watching NOV can see a company tightly linked to global drilling and offshore activity, now facing a mix of easing freight risk from the U.S. Iran peace agreement and still elevated production costs. Analysts expect strong earnings growth and the stock trades below some fair value estimates, yet recent results include a large one off loss, thin 1% profit margins, and guidance that flags softer near term revenue. Add in high P/E, a dividend not well covered by earnings, and reliance on external borrowing, and NOV appears to be a higher risk, higher potential payoff energy equipment stock. For investors, a key consideration is whether any anticipated recovery and cost actions materialize in time to compensate for these risks.

NOV’s thin margins and high P/E can make the stock look stretched, yet some investors see a turnaround story forming, and the real tension sits inside the 2 key rewards and 3 important warning signs

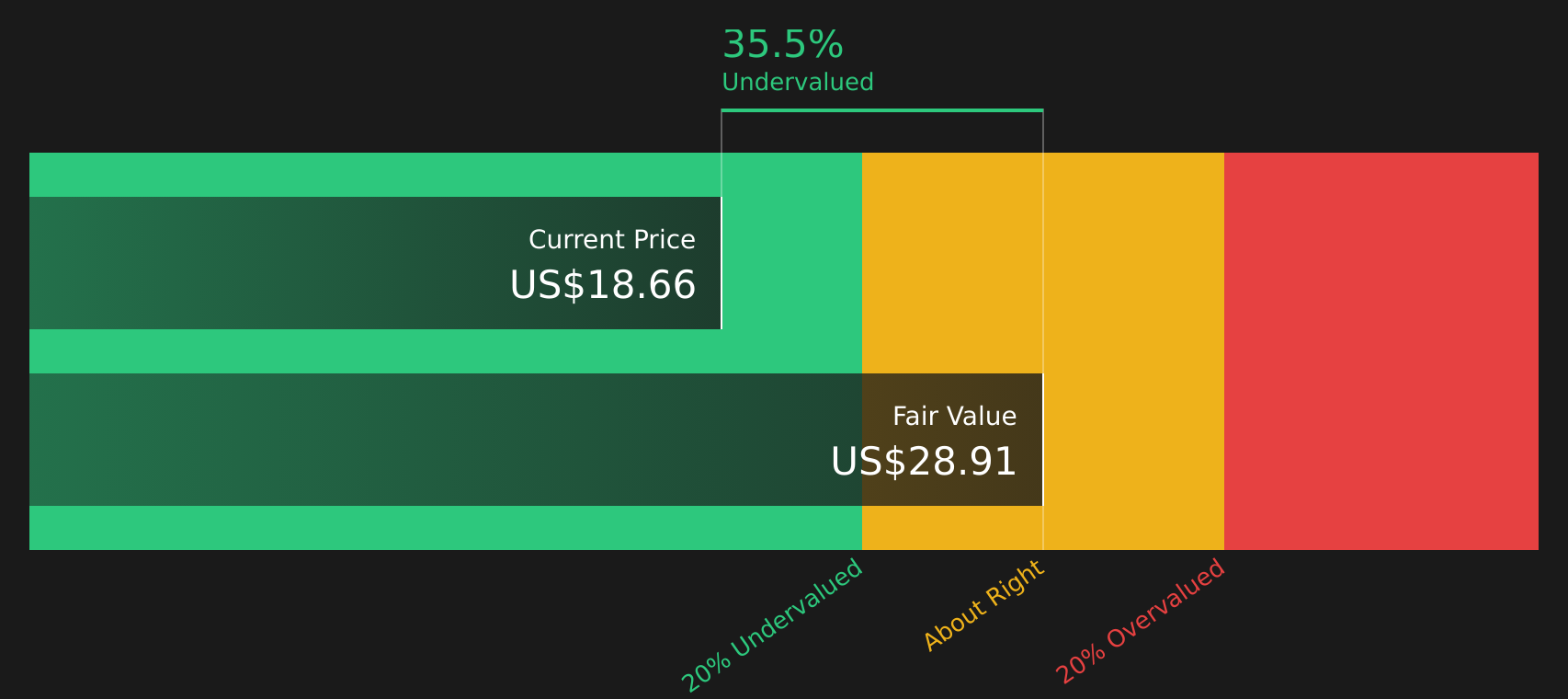

Transocean (RIG)

Overview: Transocean is a leading offshore drilling contractor that supplies high specification mobile rigs, equipment, and crews to oil and gas companies that need to drill complex wells in deepwater and harsh environments around the world.

Operations: Transocean generates about US$4.1b from providing contract drilling services, with revenue spread across the U.S. (US$1.7b), Brazil (US$912m), Norway (US$659m), and other countries (US$895m).

Market Cap: US$5.9b

Investors looking at Transocean are seeing a pure play on offshore drilling at a time when the U.S. Iran peace agreement reduces near term disruption risk in key shipping routes and producers still contend with higher input costs. The company combines an industry leading backlog of about US$7b, fresh multi year contracts, and a recent return to quarterly profitability with a heavy debt load and a funding structure built on external borrowing. In addition, there are expectations for strong earnings growth despite revenue pressure and recent credit rating upgrades tied to debt reduction. Transocean therefore sits at the intersection of improving fundamentals and meaningful balance sheet and cyclicality risks that deserve a closer look.

Transocean’s return to profitability, US$7b backlog, and fresh multi year contracts suggest a story investors may not be fully pricing. The 2 key rewards and 2 important warning signs could change how you think about its leverage and cyclicality.

Talos Energy (TALO)

Overview: Talos Energy is an independent oil and gas company focused on exploring and producing oil, natural gas, and natural gas liquids in the Gulf of Mexico and along the U.S. and Mexican coasts, with a second business focused on carbon capture and sequestration projects.

Operations: Talos Energy generates about US$1.7b from its Upstream segment, almost entirely from activities in the United States.

Market Cap: US$2.3b

Talos Energy stands out in this screener because it combines Gulf of Mexico oil production leverage with a growing carbon capture business, while trading at a steep discount to some fair value estimates and analyst price targets. The company is working on US$100m a year of efficiency and cost reduction initiatives and has been active with share buybacks, yet it still reports losses and recently booked a US$145m impairment, which highlights that execution and commodity price risks are real. With cost inflation already built into its guidance, reduced shipping risk after the U.S. Iran peace agreement, and concentrated exposure to offshore projects, Talos can be viewed as a high-risk, high potential payoff story that may merit a closer look at what could go right and what might still go wrong.

Talos Energy’s mix of Gulf of Mexico production, carbon capture projects, and cost cuts looks like a story investors have not fully pieced together yet. The analyst forecasts for Talos Energy could reveal how that effort collides with its recent losses.

The three stocks in this article are only a starting point, and the full screener of U.S. energy sector stocks on Simply Wall St highlights 45 more companies with equally compelling narratives inside the U.S. Energy Sector Stocks screener. Use Simply Wall St to identify and analyze the specific catalysts, financial health markers, and storylines that matter most to you so you can focus on the highest conviction opportunities.

Take Control of Your Investment Journey

If Talos Energy or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Momentum Flies

Breakout ideas do not stay quiet for long. Once momentum is strong, attractive entry points can quickly disappear. Scan fresh under-the-radar lists and consider acting early.

- Identify potential turnaround stories at an earlier stage by scanning a curated set of companies with resilient balance sheets using the list of solid balance sheet and fundamentals (48 results) before broader interest increases.

- Gain exposure to powerful secular themes by focusing on infrastructure, suppliers, and enablers across AI with the 49 AI infrastructure stocks while related ideas may still be under the radar.

- Position around long-term demand for critical metals by tracking producers and developers through the 30 best rare earth metal stocks before pricing dynamics and attention potentially change.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Transocean might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment