With inflation readings, bond yields and oil prices pulling markets in different directions, it is easy to feel stuck on the sidelines. The Healthy high growth potential screener offers one way to cut through that noise by highlighting companies where analysts currently expect strong earnings growth over the next 3 years and balance sheets that pass basic financial health checks. This article focuses on that theme and reveals 3 stocks from the screener that stand out for further research, giving you a focused starting list rather than another overwhelming watchlist.

Kioxia Holdings (TSE:285A)

Overview: Kioxia Holdings is a Japan based memory specialist that designs and manufactures flash memory chips, solid state drives and related storage products used in data centers, PCs, smartphones and other smart devices across Japan, North America, Europe and Asia. It also provides supporting software, production management and engineering services around its memory products.

Operations: Kioxia currently generates all of its ¥2,337,628m revenue from its Memory Business, with key sales regions including the United States, China, Japan, Taiwan and other Asian and European markets.

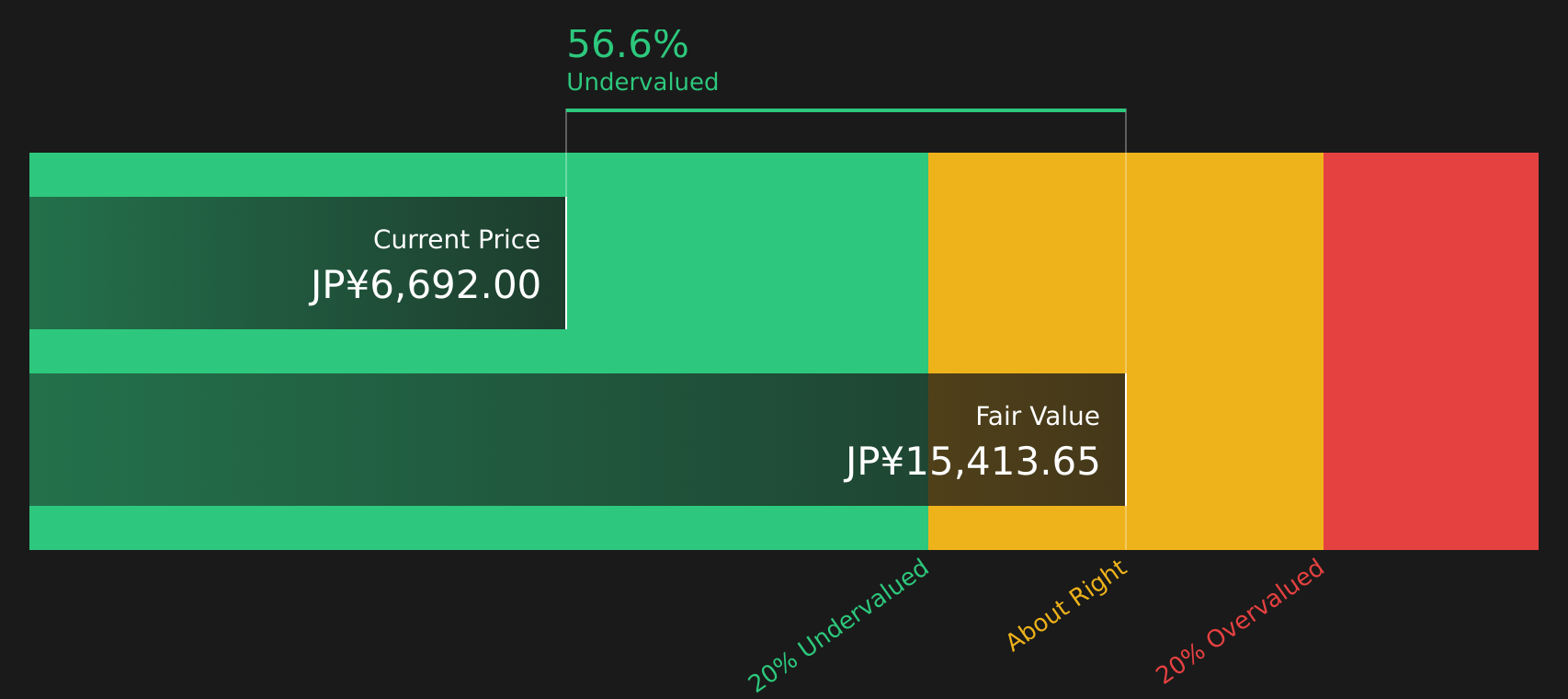

Market Cap: ¥42,137.7b

Kioxia Holdings is closely linked to AI and data center storage trends, with earnings reported as having increased significantly over the past year and forecasts indicating expectations for faster growth than the broader Japanese market. Profitability metrics are strong, including a 23.7% net margin and high Return on Equity. However, one estimate suggests that the stock trades well below a calculated fair value, which raises questions about whether high expectations and a rich P/E multiple already reflect much of the anticipated momentum. Investors also need to weigh a highly leveraged balance sheet, concentrated funding through external borrowing and a relatively new management team against the potential opportunities from next generation 3D NAND production and AI driven demand.

Kioxia Holdings sits at the intersection of AI demand, strong margins and a stretched balance sheet, and the real story only emerges when you line those up against a fresh valuation lens in the DCF valuation analysis for Kioxia Holdings

Baycurrent (TSE:6532)

Overview: Baycurrent is a Japan based consulting group that helps companies across sectors such as technology, finance, healthcare and manufacturing plan and execute projects in areas like AI, digital transformation, data analytics, cloud, security and managed services.

Operations: Baycurrent generates all of its ¥148,332m revenue from its Consulting Business in Japan.

Market Cap: ¥988.3b

Baycurrent stands out in the screener because it combines high earnings growth forecasts of around 22% a year with strong profitability, including a recent Return on Equity of about 32.3% and net margins around 25.5%. Analysts see revenue growth running well ahead of the wider Japanese market and forecasts point to even higher ROE over the next few years. One valuation model suggests the stock trades at a deep discount to estimated fair value despite a higher headline P/E. At the same time, investors need to weigh funding risk from its reliance on external borrowing and the recent share price volatility against recent buybacks, dividend increases and experienced management.

Baycurrent’s high growth forecasts and strong profitability make the headline story, but the real tension sits in how that picture aligns with funding risk and valuation in the analysis report for Baycurrent

Furukawa Electric (TSE:5801)

Overview: Furukawa Electric is a Japan based industrial group that supplies optical fiber networks, power cables, automotive wire harnesses and specialty metal products used in telecoms, energy grids, vehicles and electronics worldwide.

Operations: Furukawa Electric generates most of its revenue from Electrical Electronics at ¥765,067m, followed by Infrastructure at ¥370,856m, Functional Products at ¥161,089m and Services, Development, Etc. at ¥42,208m, partially offset by a ¥31,662m unallocated adjustment.

Market Cap: ¥2,620.5b

Furukawa Electric is attracting attention because it operates at the intersection of data, power and electric vehicle wiring. Its shares are reported to be trading only slightly below one estimate of fair value, with recent earnings growth and forecasts for approximately 21.5% yearly earnings expansion. Profit margins are reported at around 5.5%, and some analysts expect revenue to grow faster than the broader Japanese electrical sector, citing exposure to the global wire harness market and index inclusion that may support liquidity. On the other hand, investors may wish to consider funding risks from heavy reliance on external borrowing, the impact of one off items on earnings and the implications of several new directors joining the board in recent years.

Furukawa Electric sits where data traffic and power infrastructure meet, yet its story still feels incomplete. Walk through the 3 key rewards and 3 important warning signs (2 are major!) to see what might be quietly tilting the risk reward balance in the background.

The three stocks in this article are just a starting point, and the full Healthy high growth potential screen has surfaced 66 more companies with similarly compelling growth and financial health stories waiting to be compared in the Healthy high growth potential screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction ideas instead of a crowded watchlist.

Take Control of Your Investment Journey

If Furukawa Electric or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Momentum Flies?

Fresh stock ideas can move from quiet accumulation to full breakout before most investors even notice. Scan these curated lists while the data is under the radar for now, act now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Kioxia Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment