As geopolitical tensions and energy market volatility capture global attention, Asian markets are navigating these challenges with a focus on growth opportunities. In this environment, companies with high insider ownership can signal confidence in their future prospects, making them attractive considerations for investors seeking robust growth potential.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.9% | 31.5% |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 73.1% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 106.4% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 21.1% | 55.9% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

We’re going to check out a few of the best picks from our screener tool.

Simply Wall St Growth Rating: ★★★★★☆

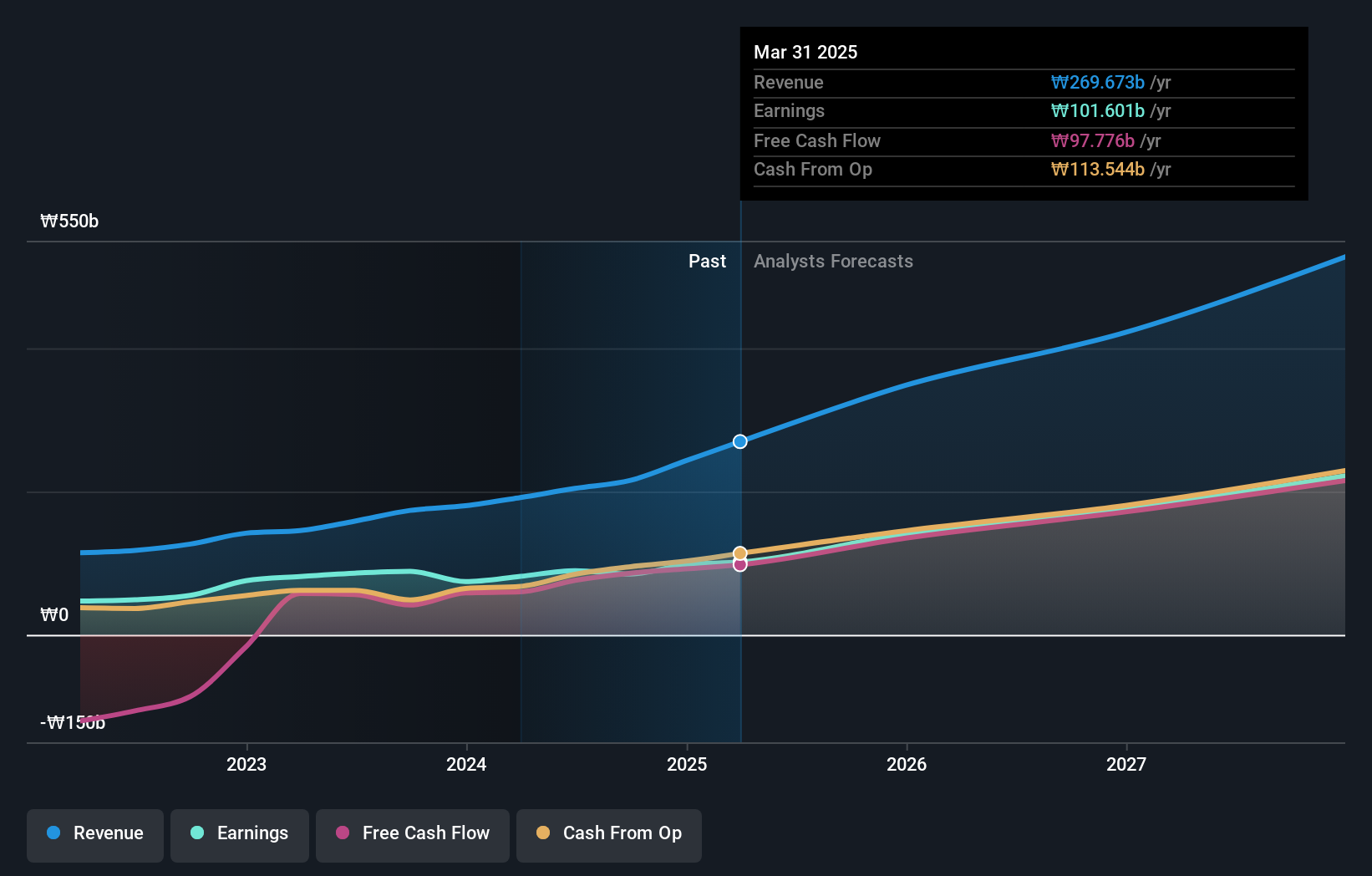

Overview: CLASSYS Inc. is a global provider of medical aesthetics devices with a market cap of ₩3.16 trillion.

Operations: The company’s revenue is primarily generated from its Surgical & Medical Equipment segment, amounting to ₩346.88 billion.

Insider Ownership: 23.4%

Revenue Growth Forecast: 21.6% p.a.

CLASSYS demonstrates strong growth potential, with revenue expected to increase by 21.6% annually, outpacing the Korean market. Despite a slower earnings growth forecast of 26.1% compared to the market’s 32.4%, its Return on Equity is projected to be robust at 29.4%. Recent earnings showed a rise in sales and net income, indicating solid performance. The stock is trading at a significant discount to its estimated fair value, suggesting possible undervaluation opportunities for investors seeking growth companies with high insider ownership in Asia.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Anhui Estone Materials Technology Co., Ltd, with a market cap of CN¥8.18 billion, is involved in the research, development, production, and sale of advanced inorganic non-metallic composites both in China and internationally.

Operations: The company’s revenue primarily comes from its Specialty Chemicals segment, which generated CN¥695.65 million.

Insider Ownership: 32.4%

Revenue Growth Forecast: 19.5% p.a.

Anhui Estone Materials Technology Ltd. is poised for growth, with earnings projected to rise 58.9% annually and revenue expected to grow at 19.5%, surpassing the Chinese market average. The company recently reported a significant turnaround, achieving a net income of CNY 0.42 million from a previous loss of CNY 16.8 million, reflecting improving financial health. A planned private placement aims to raise up to CNY 300 million, potentially enhancing capital structure and funding expansion initiatives.

Simply Wall St Growth Rating: ★★★★★☆

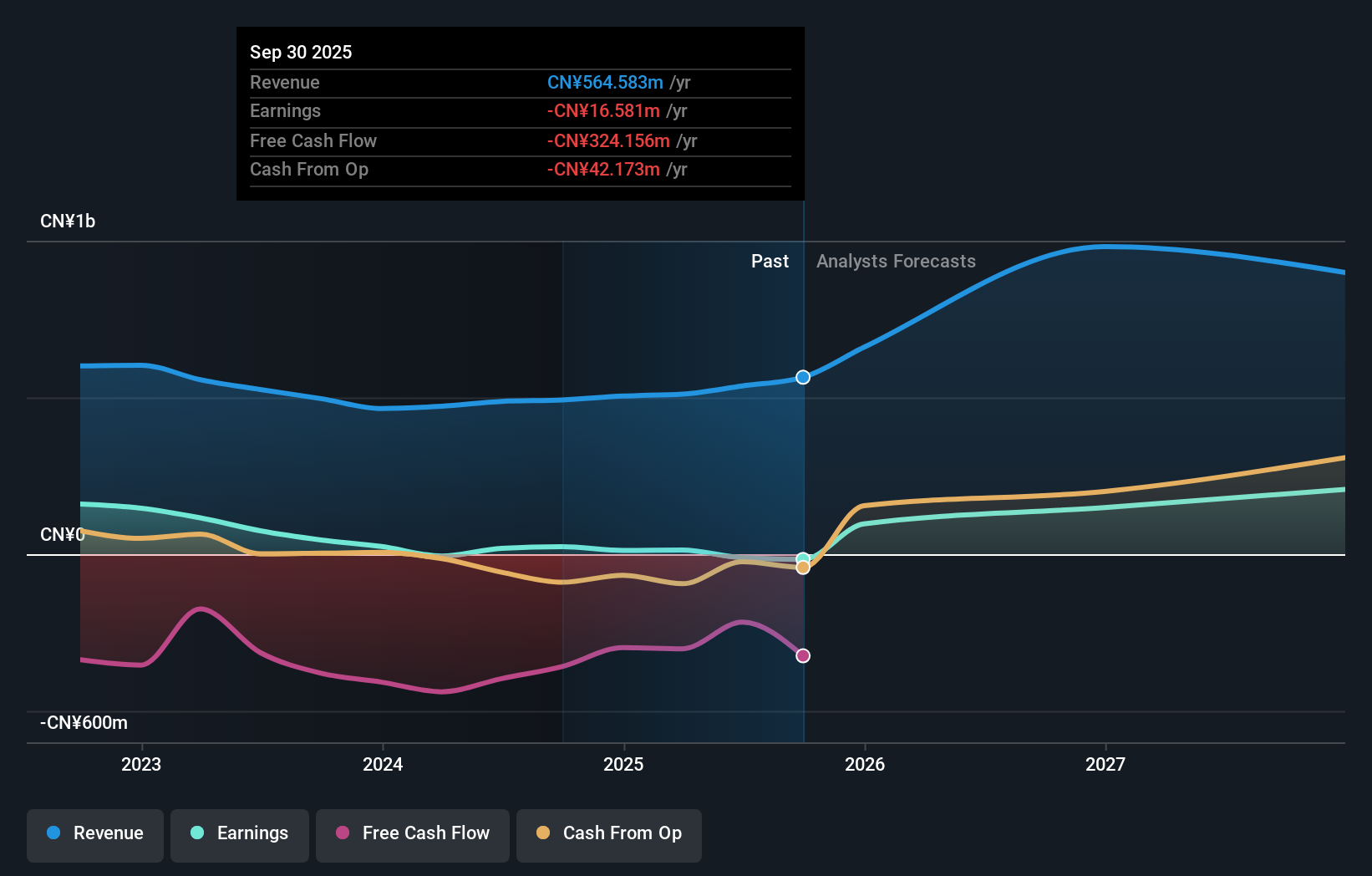

Overview: Beijing Relpow Technology Co., Ltd manufactures and sells power supply products both in China and internationally, with a market cap of CN¥14.77 billion.

Operations: Beijing Relpow Technology Co., Ltd derives its revenue primarily from the manufacture and sale of power supply products both domestically and internationally.

Insider Ownership: 26.9%

Revenue Growth Forecast: 43% p.a.

Beijing Relpow Technology is positioned for robust growth, with revenue projected to increase by 43% annually, outpacing the Chinese market average. Despite a net loss of CNY 43.07 million in Q1 2026, the company shows potential as earnings are forecast to grow significantly at 94.19% per year and become profitable within three years. However, recent share price volatility and low expected return on equity (13.4%) may pose challenges for investors seeking stability.

Next Steps

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment