Dividend growth stocks sit at an interesting crossroads for income investors who want more than just a static payout. When a company steadily lifts its dividend, it can signal confidence in its cash generation and a willingness to share that cash with shareholders. This article looks at how one recent news event may affect a select group of dividend growers, and what that could mean for your watchlist. Ahead, you will find three stocks from our Dividend Growth Stocks screener that appear positively exposed to the news backdrop, along with clear, practical takeaways for your own research.

Fastenal (FAST)

Overview: Fastenal is a wholesale distributor of industrial and construction supplies, providing everything from bolts and screws to safety gear and metal framing systems to manufacturers, maintenance teams, construction firms, and government entities across the US and internationally.

Operations: Fastenal generates the bulk of its revenue in the United States, with about US$7.0b in sales there, supported by additional contributions from Canada, Mexico and other international markets.

Market Cap: US$54.4b

Fastenal stands out in a dividend growth screen because it combines an uninterrupted dividend growth record with high reported profitability, including a net margin of 15.4% and historic return on equity of 32.6%. The company has been investing heavily in Fastenal Managed Inventory technology and digital channels, which management expects to play a bigger role in future sales. Recent commentary highlights Q4 2025 double digit daily sales growth and continued share gains even as industrial demand is described as sluggish. At the same time, the company is contending with tariff related cost pressures, elevated inventories and capital spending, and a valuation that screens as expensive on both P/E and discounted cash flow metrics. For investors, the key consideration is whether Fastenal’s execution and balance sheet justify paying a premium for its dividend track record and growth ambition.

Fastenal’s mix of high margins, rising digital sales channels and a premium valuation raises a clear question for income investors: is the market underestimating the trade off here or overpaying for it, and what does the DCF valuation analysis for Fastenal reveal that the headline numbers do not

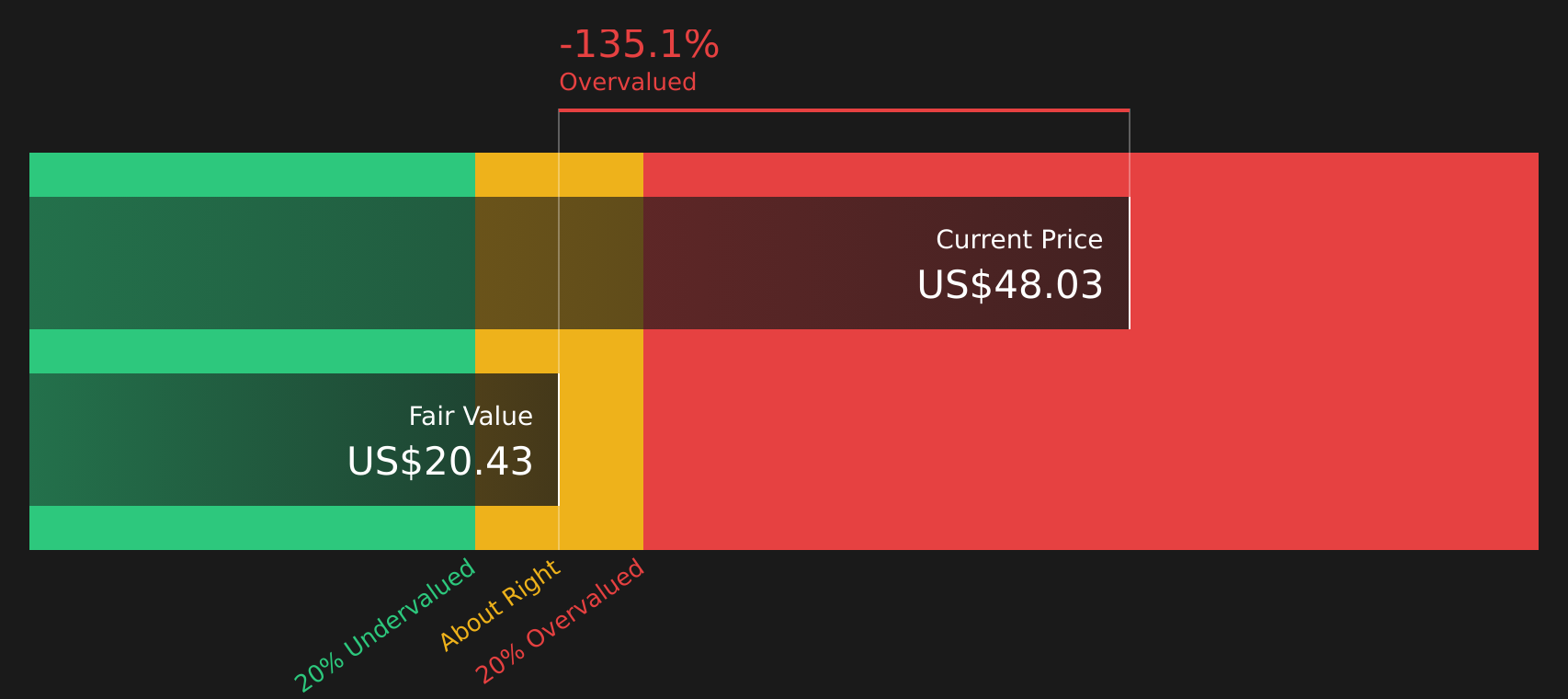

Carlisle Companies (CSL)

Overview: Carlisle Companies is a manufacturer of roofing, insulation, and other building envelope products, supplying commercial and residential customers worldwide with materials that help protect buildings from weather, moisture, and energy loss.

Operations: Carlisle generates about US$3.7b of revenue from its Carlisle Construction Materials segment and around US$1.3b from Carlisle Weatherproofing Technologies, with the United States contributing roughly US$4.5b of total sales.

Market Cap: US$15.3b

Carlisle Companies appears on a dividend growth screen because it pairs a long history of dividend increases with a focused building products portfolio that management describes as resilient and cash generative. The recent pivot to a pure play building envelope business under its Vision 2030 plan, along with efforts such as automation and the Carlisle Operating System, is aimed at improving margins even as commercial and residential construction conditions remain mixed and pricing power looks limited. At the same time, high leverage, earnings volatility, and reliance on reroofing may leave investors exposed if demand cools or buybacks and acquisitions do not deliver the intended benefits. The key consideration for dividend-focused portfolios is whether Carlisle’s combination of steady dividends, operational self-help, and building efficiency trends adequately compensates for the added balance sheet and construction cycle risk.

Carlisle Companies is reshaping itself into a focused building envelope business, and the real story may lie in how its cash flows, leverage and construction exposure interact within the analysis report for Carlisle Companies

Eaton (ETN)

Overview: Eaton is a global power management company that provides electrical equipment, aerospace systems, vehicle components, and eMobility solutions that help utilities, data centers, manufacturers, and transport operators control and protect the flow of power safely and efficiently.

Operations: Eaton generates most of its revenue from Electrical Americas at about US$13.9b, followed by Electrical Global at roughly US$7.2b and Aerospace at around US$4.4b, with a smaller segment adjustment of about US$3.1b.

Market Cap: US$158.5b

Eaton attracts dividend growth investors because its power grid, electrification, and data center businesses are closely tied to long term spending programs such as the Inflation Reduction Act. Management highlights hundreds of billions of dollars aimed at grid upgrades and climate projects that touch many of Eaton’s core products. At the same time, the stock trades on a higher P/E than the US Electrical industry, uses substantial debt to support returns, and is seeing insider selling and mixed earnings momentum, which can increase downside risk if growth disappoints or large projects are delayed. The planned separation of the Mobility business and acquisitions like Boyd Thermal add another layer of opportunity and execution risk that income investors may wish to weigh carefully.

Eaton’s power and electrification story looks strong, but the real tension is how its premium P/E, debt load and project pipeline fit together in the analysis report for Eaton

The three dividend growth stocks in this article are only a starting point, as the full Dividend Growth Stocks screener highlights 46 more companies with equally compelling income and business narratives that could broaden your watchlist. Use Simply Wall St to identify, analyze and filter for the specific catalysts and dividend growth profiles that matter to you so you can focus on the highest conviction ideas in minutes.

Take Control of Your Investment Journey

If Eaton or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives For Your Curiosity?

Fresh stock ideas do not stay under the radar for long. Once momentum builds, ideal entry points can vanish before the crowd reacts, so consider researching them early.

- Spot companies where resilient cash flows meet stronger balance sheets and use the curated list of solid balance sheet and fundamentals (48 results) to see which stocks currently pass those filters.

- Review potential opportunities in early stage miners by using the hand picked 33 elite gold producer stocks that screens for producers with meaningful output and funding already in place.

- Track potential AI infrastructure beneficiaries before interest broadens by scanning the focused 51 AI infrastructure stocks curated for companies supplying the picks and shovels of computing power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Eaton might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment