As global markets navigate a landscape marked by inflation pressures and geopolitical tensions, Asia’s economic resilience remains a focal point for investors. In this context, growth companies with substantial insider ownership are often viewed as having strong potential, as high insider confidence can signal alignment between management and shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 68.3% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 106.4% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| Meitu (SEHK:1357) | 22.7% | 31.5% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| HUMAN MADE (TSE:456A) | 23.9% | 22.6% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.6% |

| Great Microwave Technology (SHSE:688270) | 21.1% | 85.5% |

| Fulin Precision (SZSE:300432) | 10.4% | 60.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

We’ll examine a selection from our screener results.

Simply Wall St Growth Rating: ★★★★★★

Overview: Park Systems Corp. develops, manufactures, and sells atomic force microscopy (AFM) systems globally and has a market cap of approximately ₩2.36 trillion.

Operations: The company’s revenue primarily comes from its Scientific & Technical Instruments segment, which generated approximately ₩194.07 billion.

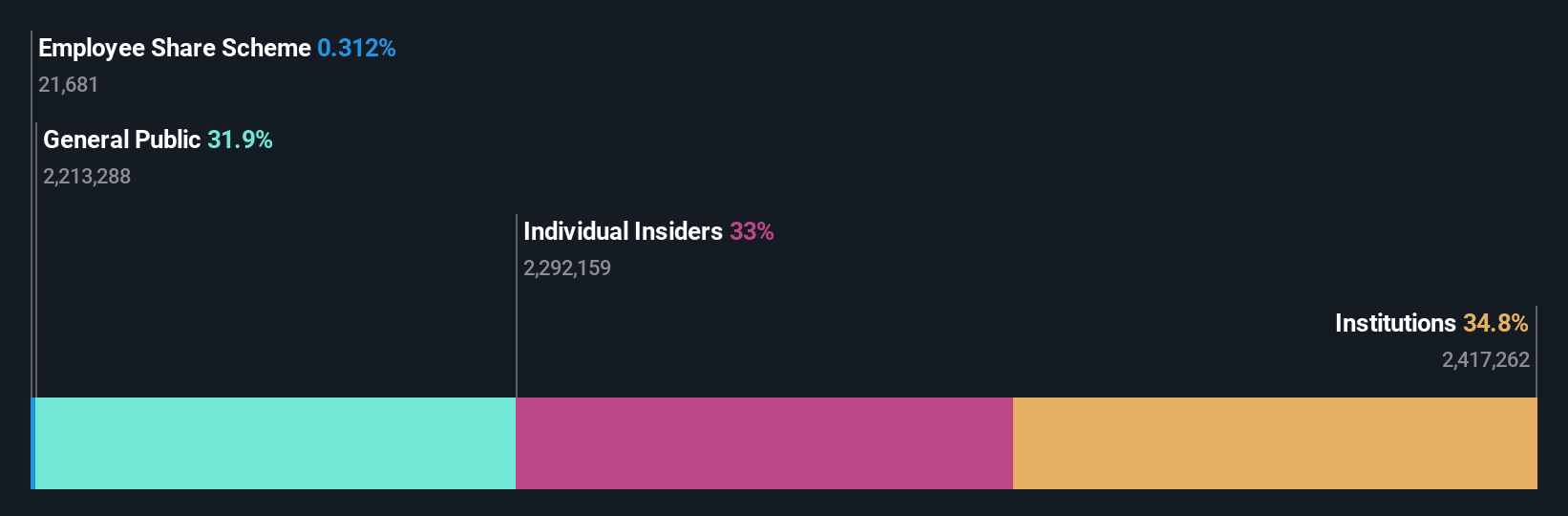

Insider Ownership: 33%

Return On Equity Forecast: 22% (2029 estimate)

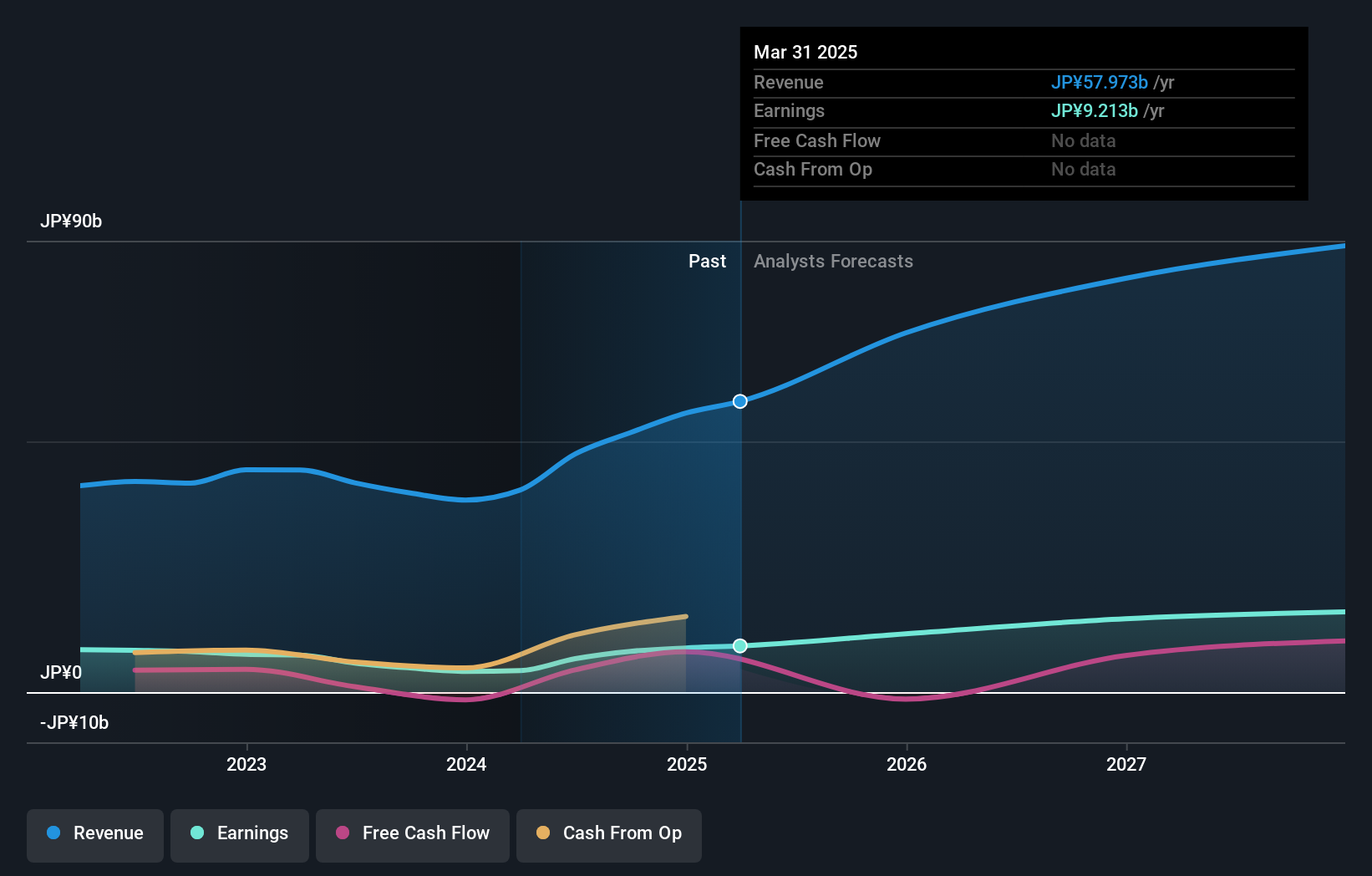

Park Systems, with significant insider ownership, is positioned as a growth company in Asia. Recent private placements raised KRW 100 billion, indicating strong investor interest. The launch of advanced products like the Park FX40 IR and NX1 highlights its innovative edge in nanotechnology. Despite high share price volatility and reduced profit margins, forecasted earnings growth of 37.5% annually surpasses market averages. The new headquarters in Gwacheon underscores its commitment to R&D expansion and global reach.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zhende Medical Co., Ltd. focuses on the research, development, production, and sale of medical care and protective equipment both in China and internationally, with a market cap of CN¥22.58 billion.

Operations: Zhende Medical generates its revenue through the development, production, and sale of medical care and protective equipment across domestic and international markets.

Insider Ownership: 10.1%

Return On Equity Forecast: N/A (2029 estimate)

Zhende Medical, with substantial insider ownership, is poised for growth in Asia’s expanding wound care market. The recent joint venture with Mölnlycke Health Care aims to leverage combined expertise to enhance market access and drive long-term growth. Despite a modest revenue increase to CNY 1 billion in Q1 2026, earnings are forecasted to grow significantly at 38% annually, outpacing the Chinese market average. The strategic alliance underscores Zhende’s commitment to advancing its product portfolio and capitalizing on emerging opportunities.

Simply Wall St Growth Rating: ★★★★★★

Overview: Micronics Japan Co., Ltd. develops, manufactures, and sells body measuring equipment as well as semiconductor and liquid crystal display inspection equipment globally, with a market cap of ¥583.79 billion.

Operations: Micronics Japan generates revenue from its global operations in body measuring equipment, semiconductor inspection tools, and liquid crystal display inspection devices.

Insider Ownership: 15.3%

Return On Equity Forecast: 35% (2029 estimate)

Micronics Japan is positioned for robust growth driven by its strong presence in the semiconductor market. The company has revised its earnings guidance upward, reflecting a favorable outlook with net sales expected to reach JPY 71.6 billion by September 2026. Despite recent share price volatility, analysts forecast significant annual earnings growth of 25%, surpassing the Japanese market average. High insider ownership aligns management interests with shareholders, potentially enhancing long-term value creation amidst expanding probe card demand.

Make It Happen

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we’re here to simplify it.

Discover if Zhende Medical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment