The global ETF industry is entering a new phase of maturity, with active ETFs—particularly in fixed income—emerging as the next major engine of growth, according to Travis Spence, global head of ETFs at J.P. Morgan Asset Management. He spoke at the European Media Summit on 20 May 2026 in London.

Active ETFs fuel industry expansion

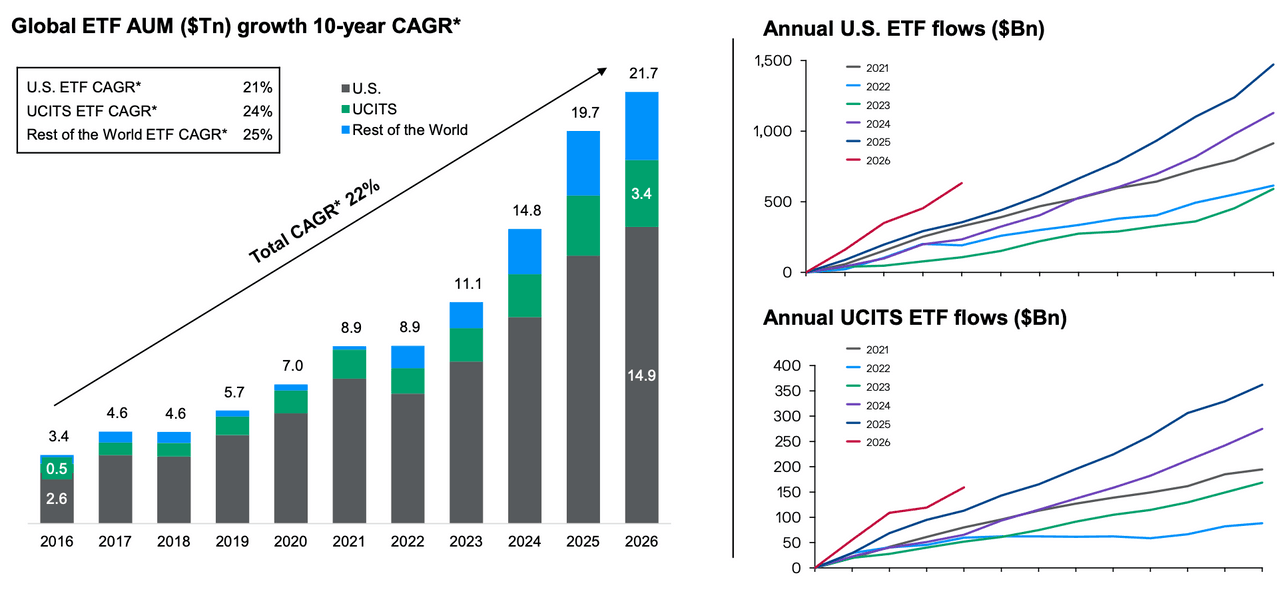

Professional asset managers still represent 85% of the European ETF investor base. However, the industry itself has doubled in size every five years, supported by a 20% compound annual growth rate (see Chart 1, left). While growth accelerated to 30% in recent years, 2026 has started even more strongly (see Chart 1, right).

Chart 1: Global ETF industry is on pace for a 3rd consecutive record year in 2026 Source: Left: Guide to ETFs – EMEA (Slide 4). Data as of 30 April 2026. Right top: Bloomberg, Factset and J.P. Morgan Asset Management as of 30 April 2026. US ETFs only; excludes ETNs. Right bottom: Bloomberg, Factset and J.P. Morgan Asset Management as of 30 April 2026. UCITS ETFs only; excludes ETNs. *Compound annual growth rate (CAGR).

The trend is particularly visible in the US market, where active strategies now account for 85% of all ETF launches. In Europe’s Ucits market, the share has risen to 43%, up from just 3% three years ago.

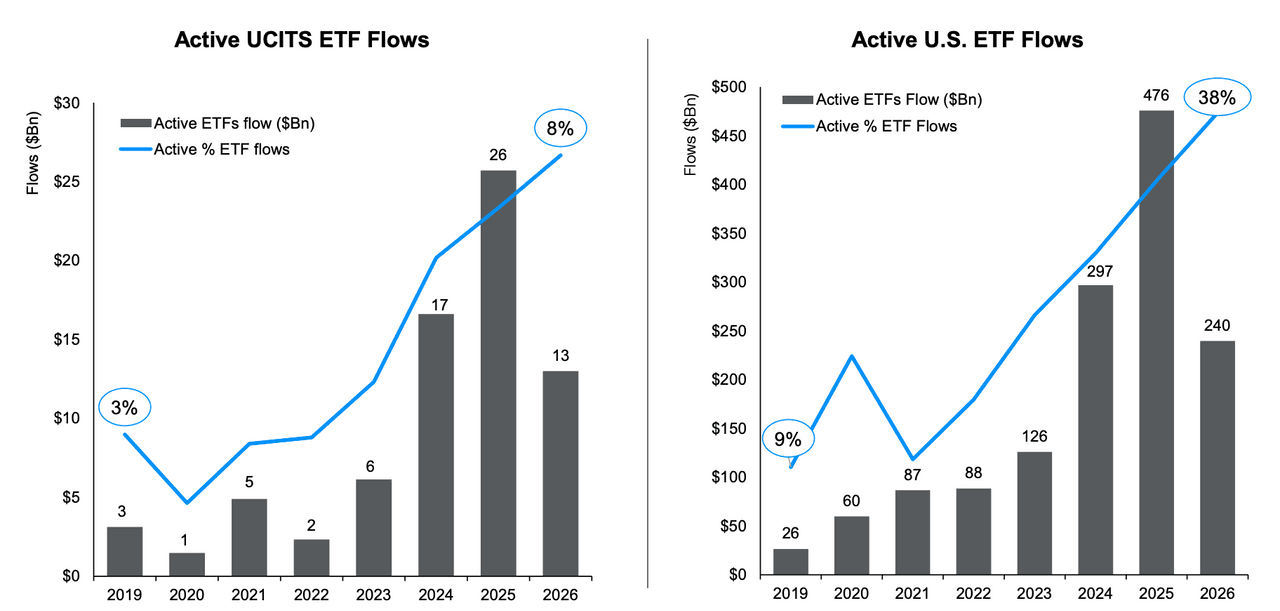

“There’s more active ETFs than there are passive ETFs in the US,” he said. Spence estimated that active ETFs are now taking in 36% of net flows across the entire globe, up from 25% in 2025 (see Chart 2).

Chart 2: The $2.3T (10%) active ETF market is driving 36% of global ETF net flows Source: Bloomberg, J.P. Morgan Asset Management. Active ETFs are determined by non-index funds. UCITS ETFs as defined by Bloomberg. Data as of 30 April 2026.

Fixed income becomes the next battleground

A primary driver of this transformation is the evolution of fixed-income ETFs. The global bond market is immense and complex, argued Spence, with over $140trn of outstanding debt and more than 3 million individual bonds. He said that this complexity makes the ETF vehicle particularly valuable, as it provides a diversified portfolio in a single ticker that trades with equity-like liquidity.

While 80% to 90% of fixed income mutual funds are actively managed, approximately 80% of fixed income ETFs remain passively managed. Spence argued that the industry has reached an “inflection point” where flows will shift toward active strategies.

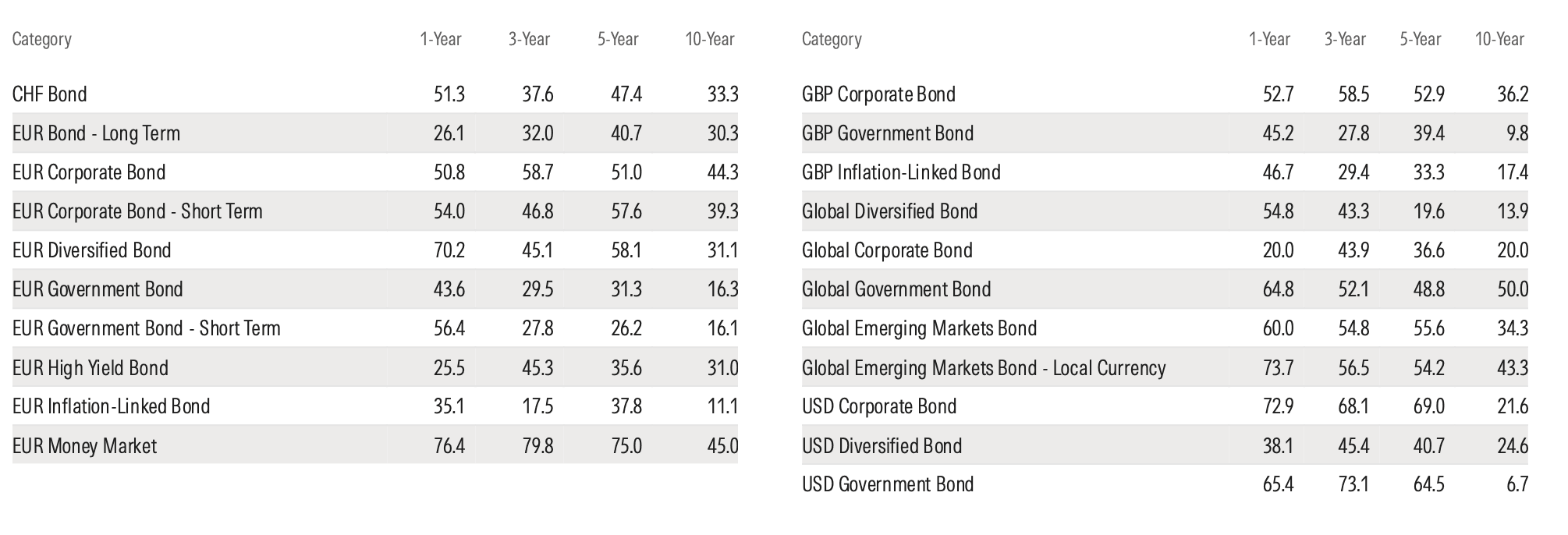

Outperformance of active bond ETFs to be proven

Spence stated that “most active managers outperform their benchmarks because the indices are not designed to be investable in fixed income.” He noted that the index often weighs the largest debtors most heavily, which is rarely the most prudent investment decision.

However, long-term evidence on active management remains mixed. Morningstar’s 2025 Active/Passive Barometer showed that most active bond funds underperformed their benchmarks over a 10-year horizon, except for global government bond strategies (see Chart 3).

Chart 3: Active fixed-income funds’ success rate by category (%) Source: Morningstar Direct. Data as of Dec. 31, 2025.

Global active fixed income ETF assets currently sit at approximately $650bn, a figure that will likely rise rapidly in the coming years. In the US, active strategies are already capturing 38% of all fixed income ETF flows (see Chart 3, left). As issuance of new fixed income ETFs accelerates (see Chart 3, bottom right), active strategies are likely to capture a larger share of flows, which currently stand at 13% globally (see Chart 3, top right).

Broader active ETF trends and innovation

Beyond traditional active fixed income strategies, innovation is also accelerating in other ETF segments. have emerged as a significant category, growing from nearly zero in 2020 to a $300bn market in the US. These tools allow investors to solve portfolio problems by providing income and downside protection, helping investors remain invested during volatile markets.

Infrastructure and the retail frontier

Managing an active ETF requires substantial operational infrastructure. Providers must handle clearance, custody, collateral management, corporate actions, daily NAV transparency, tax efficiency, and capital markets liquidity. Spence described the ETF market structure as “battle tested” during periods of stress, highlighting the resilience of the industry’s infrastructure.

Finally, the European retail market represents a significant growth frontier, added Spence. Currently accounting for about 10% of the industry at $340bn, retail participation is expected to surge as digital platforms and pension reforms—such as those in Germany—encourage a shift from saving to investing.

Combined with the rapid expansion of active strategies, these developments suggest the ETF industry may be entering a structurally different phase of growth—one increasingly driven by innovation, active management, and retail adoption.

Sylvain Barrette in London

Paperjam was invited to attend the J.P. Morgan Asset Management 2026 European Media Summit in London. The latter paid for accommodation and transportation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment