UK Private Equity Market Report Summary

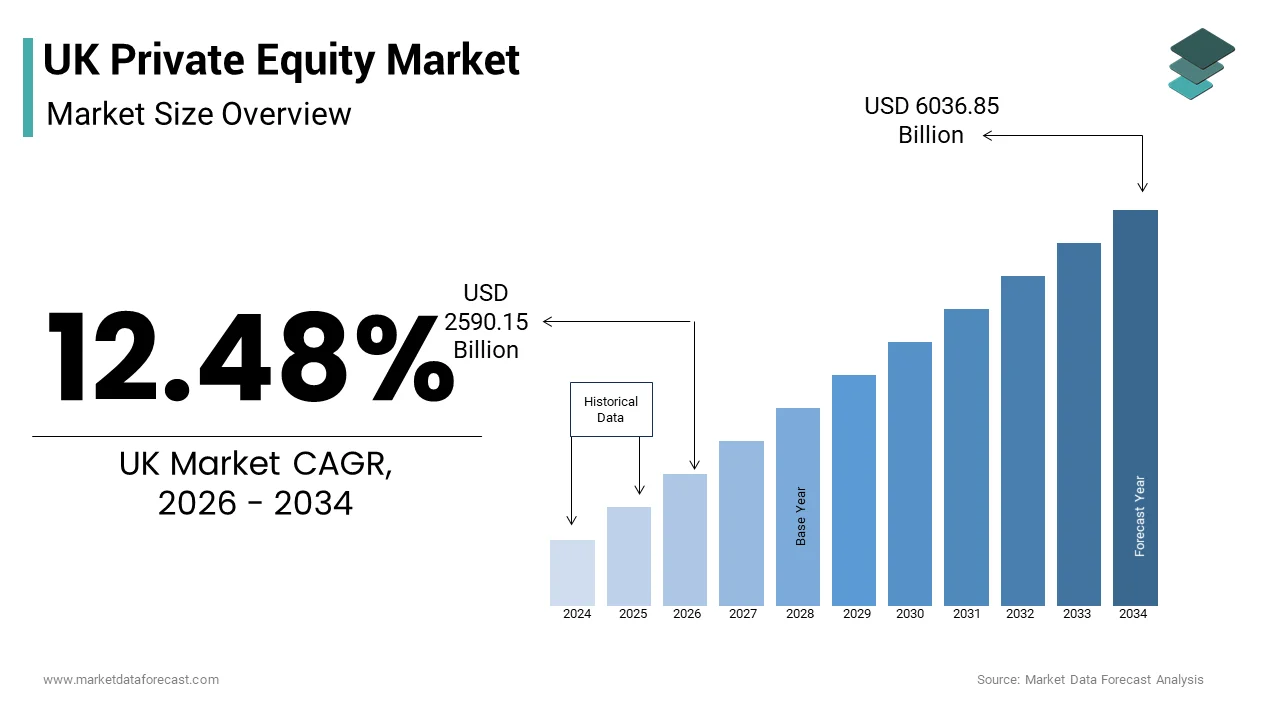

The UK private equity market was valued at USD 2,302.39 billion in 2025 and is anticipated to reach USD 2,590.15 billion in 2026 and further expand to USD 6,036.85 billion by 2034, growing at a CAGR of 12.48% during the forecast period from 2026 to 2034. The growth of the UK private equity market is driven by a strong investment ecosystem, increasing institutional capital allocations, and the country’s position as a leading financial hub in Europe. Rising merger and acquisition activity, growing interest in high-growth companies, and increasing investments across technology, healthcare, consumer, and industrial sectors are further supporting market expansion. Additionally, favorable regulatory frameworks, robust capital markets, and the growing focus on value creation strategies are creating significant opportunities for private equity firms operating in the United Kingdom.

Key Market Trends

- Increasing leveraged buyout activity as firms seek opportunities to acquire and transform businesses through operational improvements and strategic restructuring.

- Growing investments in technology, digital transformation, and software-driven companies with strong long-term growth potential.

- Rising interest in ESG-focused investments and sustainable business models across private equity portfolios.

- Expansion of private credit and alternative financing solutions supporting deal execution and portfolio growth.

- Increasing focus on value creation through operational efficiency, digital innovation, and strategic acquisitions within portfolio companies.

Segmental Insights

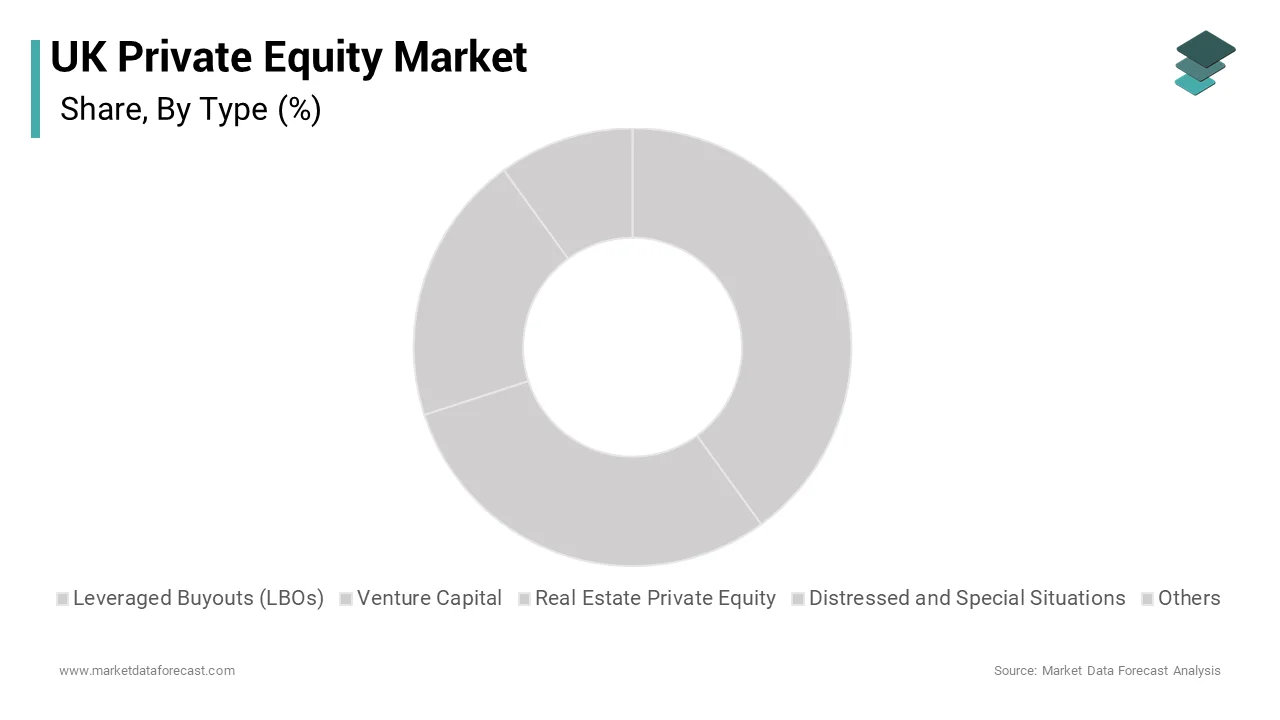

- Based on type, the leveraged buyouts (LBOs) segment dominated the UK private equity market and accounted for 38.4% of the market share in 2025. The segment’s leadership is attributed to the availability of financing options, strong investor appetite for established businesses, and the potential to generate substantial returns through operational improvements and strategic growth initiatives.

- Based on industry, the consumer and retail segment held the largest share of the UK private equity market, capturing 24.7% in 2025. The dominance of this segment is driven by resilient consumer demand, evolving retail business models, digital commerce expansion, and opportunities for brand development and market consolidation.

Regional Insights

The United Kingdom dominated the European private equity market and accounted for 30.3% of the regional market share in 2025. The country’s leadership is supported by its mature financial services sector, deep capital markets, strong legal and regulatory framework, and extensive network of institutional investors. London continues to serve as a major center for private equity activity, attracting global investment firms and facilitating large-scale transactions across diverse industries. The increasing flow of domestic and international capital further reinforces the UK’s position as Europe’s leading private equity market.

Competitive Landscape

The UK private equity market is highly competitive, with global and regional investment firms focusing on strategic acquisitions, portfolio optimization, sector specialization, and value creation initiatives. Market participants are increasingly investing in technology-enabled businesses, sustainability-focused enterprises, and high-growth sectors to maximize returns. Firms are also leveraging data analytics, operational expertise, and strategic partnerships to enhance portfolio performance and strengthen their competitive positions. Continued fundraising activity and cross-border investments remain key drivers of market competitiveness.

Prominent players in the UK private equity market include Blackstone, KKR & Co., Apollo Global Management, The Carlyle Group, Bridgepoint Group, TPG, Bain Capital, Warburg Pincus, Thoma Bravo, Vista Equity Partners, EQT, CVC Capital Partners, Advent International, Permira, Ardian, and Hellman & Friedman.

UK Private Equity Market Size

The UK private equity market size was valued at USD 2302.39 billion in 2025 and is anticipated to reach USD 2590.15 billion in 2026 to reach USD 6036.85 billion by 2034, growing at a CAGR of 12.48% during the forecast period from 2026 to 2034.

MARKET OVERVIEW

Private equity (PE) is an alternative investment strategy where firms pool capital from institutional investors to buy ownership stakes in private companies or acquire publicly traded companies to take them private. The UK remains Europe’s powerhouse for private equity. This market serves as a critical engine for economic dynamism providing capital to businesses that may lack access to traditional public markets or require strategic restructuring. The regulatory environment is robust with the Financial Conduct Authority overseeing compliance ensuring transparency and investor protection across transactions. London remains a global financial hub attracting international capital due to its deep liquidity pools and legal framework based on English common law which is highly regarded for contract enforcement. The cultural emphasis on entrepreneurship supports a vibrant pipeline of mid market companies seeking expansion capital. According to data from the Office for National Statistics the services sector accounts for 80 percent of the UK economy creating diverse opportunities for private equity firms specializing in healthcare technology and professional services. The prevalence of family owned businesses transitioning to professional management structures provides a steady stream of acquisition targets. As per insights from the British Business Bank small and medium enterprises contribute 52 percent of private sector turnover indicating a vast reservoir of potential investment candidates. The integration of environmental social and governance criteria into investment mandates reflects evolving stakeholder expectations. This foundational landscape combines financial sophistication with regulatory stability fostering an environment where private equity can thrive while contributing to broader economic productivity and innovation throughout the nation.

MARKET DRIVERS

Abundant Dry Powder Creates Urgent Deployment Pressure

The substantial accumulation of uninvested capital known as dry powder is a primary driver for increased transaction activity within the United Kingdom private equity market. Institutional investors including pension funds endowments and sovereign wealth funds have consistently allocated significant portions of their portfolios to alternative assets seeking higher yields than traditional bonds or equities. According to a study, global private equity dry powder has reached unprecedented historical highs, climbing past $3.7 trillion with a substantial geographic allocation targeting European and UK-based transactions. This capital overhang creates intense pressure on fund managers to identify and execute acquisitions before fund lifecycles expire typically within ten years. The urgency to deploy capital often leads to competitive bidding processes driving up valuations but also ensuring that viable companies receive necessary funding for expansion. Fund managers are compelled to broaden their search criteria considering smaller ticket sizes or distressed assets that were previously overlooked. This influx of liquidity supports business continuity during economic downturns allowing companies to invest in technology and talent without relying on volatile public markets. The sheer volume of available capital ensures that even in periods of macroeconomic uncertainty deal flow remains robust as firms compete to secure promising targets. This dynamic sustains market vitality and encourages innovation in deal structuring to accommodate diverse investor requirements.

Strong Pipeline of Mid Market Acquisition Targets

The existence of a robust pipeline of mid-market companies seeking succession planning or growth capital fundamentally fuels demand in the United Kingdom private equity market. A significant proportion of UK businesses are family owned with founders approaching retirement age and lacking internal successors willing or able to take over operations. Research highlights that only 30% of family-owned firms successfully transition to the second generation, creating a structural need for third-party corporate or private equity intervention during succession crises. Private equity firms offer an attractive exit route providing liquidity to founders while ensuring business continuity through professional management teams. These mid market entities often possess strong brand recognition and stable cash flows but lack the scale or expertise to expand internationally or adopt digital technologies. As per data from the Confederation of British Industry small and medium enterprises account for 99 percent of the UK business population representing a vast universe of potential targets. Private equity investors bring operational expertise strategic networks and financial resources that enable these companies to unlock latent value. The fragmentation of many sectors such as healthcare services and industrial manufacturing allows for buy and build strategies where platform companies acquire smaller competitors to achieve economies of scale. This structural characteristic of the UK economy ensures a consistent flow of deal opportunities that align with the investment mandates of most private equity funds. The alignment of seller motivations with buyer capabilities sustains high transaction volumes.

MARKET RESTRAINTS

Elevated Interest Rates Increase Cost of Capital

The sustained elevation of interest rates is a major limitation to the United Kingdom private equity market. This increases the cost of debt financing which is essential for leveraged buyouts. Private equity transactions frequently rely on borrowed funds to amplify returns meaning that higher borrowing costs directly compress profit margins and reduce internal rates of return. According to data from the Bank of England the base rate remained at elevated levels throughout recent periods influencing commercial lending rates which increased by approximately 300 basis points compared to historical averages. This shift forces deal makers to renegotiate terms with lenders often resulting in lower leverage multiples and stricter covenant packages. As per analysis from Deloitte the average debt to earnings ratio for mid market deals has decreased by 10 percent as lenders become more risk averse in a high rate environment. Higher interest expenses also impact portfolio companies reducing their free cash flow available for reinvestment or dividend recapitalizations. Some potential acquisitions become financially unviable when modeled under current financing conditions leading to deal abandonment or prolonged negotiation periods. Sellers may resist lowering price expectations creating a valuation gap that stalls transaction momentum. The uncertainty regarding future rate trajectories complicates long term financial planning for both investors and portfolio companies. This financial headwind requires private equity firms to rely more heavily on operational improvements rather than financial engineering to generate returns. The increased cost of capital thus acts as a brake on deal volume and valuation growth.

Regulatory Scrutiny Enhances Compliance Burdens

Intensifying regulatory scrutiny imposes substantial compliance burdens that restrain operational agility and increase transaction costs for PE firms in the country, which hampers the expansion of the United Kingdom private equity market. The implementation of the National Security and Investment Act grants the government powers to review and potentially block transactions that pose risks to national security adding complexity and uncertainty to the deal process. According to guidance from the Department for Business and Trade mandatory notifications are required for acquisitions in seventeen sensitive sectors including artificial intelligence and defense. This requirement extends deal timelines by several months as firms await clearance causing frustration for sellers and increasing execution risk. Corporate legal reviews indicate that expanding multijurisdictional antitrust and national security filings have significantly driven up cross-border compliance fees for UK corporate acquisitions. Besides, the Financial Conduct Authority has strengthened rules regarding environmental social and governance disclosures requiring firms to integrate sustainability metrics into their investment processes. These mandates necessitate specialized staff and sophisticated data collection systems diverting resources from core investment activities. Smaller firms struggle disproportionately with these demands lacking the infrastructure of larger competitors. The threat of retrospective intervention creates a chilling effect on certain types of investments particularly in technology and infrastructure. Firms must conduct enhanced due diligence to mitigate regulatory risks further slowing down the investment cycle. This regulatory weight reduces the attractiveness of the UK market for some international investors who perceive the administrative burden as excessive compared to other jurisdictions.

MARKET OPPORTUNITIES

Digital Transformation Initiatives Unlock Operational Value

The widespread need for digital transformation across traditional industries presents a lucrative opportunity for PE firms to create value through technological modernization in the country, which is likely to boost the growth of the United Kingdom private equity market. Many mid market companies operate with legacy systems and manual processes that hinder efficiency and scalability offering clear avenues for improvement post acquisition. According to research, companies that successfully implement digital tools can increase productivity by up to 20 percent providing a tangible path to margin expansion. Private equity investors leverage their networks to recruit chief technology officers and implement enterprise resource planning systems that streamline operations. The adoption of cloud computing data analytics and automation reduces operational costs and enhances customer experiences driving revenue growth. As per data from the Tech Nation report the UK tech sector continues to attract significant investment indicating a rich ecosystem of vendors and talent that private equity firms can tap into. Investing in cybersecurity measures also protects portfolio companies from emerging threats preserving brand reputation and avoiding costly breaches. The ability to digitize supply chains improves visibility and resilience against disruptions which is increasingly valued by customers. Private equity firms that specialize in operational turnaround can acquire undervalued assets and transform them into digitally enabled leaders. This strategy generates superior returns compared to pure financial engineering and aligns with broader economic trends toward efficiency. The vast untapped potential in non tech sectors such as manufacturing and logistics ensures a long runway for this value creation strategy.

Expansion into Healthcare and Life Sciences Sectors

The aging demographic profile of the country’s population creates robust demand for healthcare and life sciences services, providing a compelling opening for PE investment, which is expected to accelerate the expansion of the United Kingdom private equity market. As life expectancy increases the prevalence of chronic conditions rises necessitating expanded capacity in care homes diagnostic centers and specialized treatment facilities. According to data from the Office for National Statistics the number of people aged 65 and over is projected to increase by 20 percent over the next decade driving sustained demand for healthcare services. Private equity firms are well positioned to consolidate fragmented markets such as dental practices veterinary clinics and home care providers achieving economies of scale and improved service quality. The government focus on reducing waiting lists in the National Health Service opens avenues for private providers to deliver outsourced services under contract. Investment in medical technology and telemedicine platforms further enhances service delivery and reach. Regulatory support for innovation in life sciences encourages investment in biotech startups with promising pipelines. Private equity capital provides the patience and resources needed to navigate lengthy clinical trials and regulatory approvals. This sector offers defensive characteristics with resilient cash flows regardless of broader economic cycles. The combination of demographic tailwinds and structural inefficiencies creates a fertile ground for value creation through strategic consolidation and operational enhancement.

MARKET CHALLENGES

Valuation Gaps Impede Deal Completion

Persistent valuation gaps between buyers and sellers are a major challenge that impedes deal completion and slows transaction velocity in the United Kingdom private equity market. Sellers often anchor their price expectations to peak valuations seen in previous years while buyers adjust their models to reflect higher interest rates and economic uncertainty. According to surveys by EY approximately 40 percent of planned deals were delayed or abandoned due to disagreements on pricing during recent periods. This standoff creates a stalemate where sellers prefer to wait for better market conditions while buyers seek deeper discounts to compensate for perceived risks. The lack of comparable public market benchmarks for private companies exacerbates the difficulty in reaching consensus on fair value. Bridging this gap often requires complex earn out structures or vendor financing which introduce additional risks and administrative complexities. Sellers may be reluctant to accept contingent payments preferring upfront certainty. Buyers face pressure from limited partners to deploy capital but cannot overpay without compromising return targets. This tension prolongs due diligence periods and increases the likelihood of deal fatigue. The uncertainty surrounding future economic performance makes it difficult for both parties to agree on long term projections. This valuation disconnect will remain a significant hurdle to market fluidity. These challenges will persist until market sentiment stabilizes and clearer price discovery mechanisms emerge.

Talent Shortage Constrains Portfolio Company Growth

The acute shortage of skilled managerial and technical talent constrains the ability of portfolio companies to execute growth strategies in the United Kingdom private equity market. Post acquisition value creation plans often rely on hiring experienced executives to professionalize operations and drive expansion but the tight labor market makes this difficult. According to the Recruitment and Employment Confederation (REC), past acute talent shortages have started to ease as a softening economic outlook drives increased candidate availability and a decline in open vacancies. The competition for talent is fierce not only from other private equity backed companies but also from large corporations offering competitive compensation packages. As per reports from the Chartered Institute of Personnel and Development wage inflation in key sectors has exceeded 5 percent increasing operational costs for portfolio companies. The lack of middle management depth can stall integration efforts following add on acquisitions limiting the effectiveness of buy and build strategies. Private equity firms must invest heavily in employer branding and retention programs to attract and keep top performers. The remote work trend has expanded the talent pool geographically but also intensified competition for flexible working arrangements. Skills gaps in digital literacy further complicate transformation initiatives requiring extensive training investments. The inability to secure critical hires delays revenue growth and margin improvement targets jeopardizing investment thesis realization. This human capital constraint requires private equity operators to prioritize organizational culture and development pipelines as much as financial engineering.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

12.48% |

|

Segments Covered |

By Type, Industry, Country |

|

Various Analyses Covered |

Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

|

Regions Covered |

London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

|

Market Leaders Profiled |

Blackstone (U.S.), KKR & Co. (U.S.), Apollo Global Management (U.S.), The Carlyle Group (U.S.), Bridgepoint Group, TPG (U.S.), Bain Capital (U.S.), Warburg Pincus (U.S.), Thoma Bravo (U.S.), Vista Equity Partner (U.S.), EQT (Sweden), CVC Capital Partners (Luxembourg), Advent International (U.S.), Permira (U.K.), Ardian (France), Hellman & Friedman (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

Leveraged Buyouts (LBOs)

The leveraged buyouts (LBOs) segment was the largest in the United Kingdom private equity market and occupied a 38.4% share in 2025. This prominence of the segment is supported by the maturity of target companies and the availability of debt financing for established businesses. Also, this strategy involves acquiring a controlling interest in a company using a significant amount of borrowed money to meet the cost of acquisition. The dominance of this segment is further driven by the presence of numerous mid market companies with stable cash flows that can service debt obligations. According to data from Preqin leveraged buyout transactions accounted for approximately 60 percent of total deal value in the UK private equity sector over the past year. The predictability of earnings in sectors such as manufacturing business services and healthcare makes these targets ideal for leverage based strategies. Private equity firms utilize their operational expertise to improve efficiency and reduce costs thereby enhancing the ability of portfolio companies to repay debt. The depth of the UK credit market provides lenders with confidence to extend financing even in fluctuating economic conditions. Investors favor this model due to its potential for high returns through financial engineering and operational improvements. The established legal framework for secured lending in the UK further supports the prevalence of leveraged transactions. This combination of suitable targets available credit and proven value creation methods ensures that leveraged buyouts remain the cornerstone of the private equity landscape.

The robust availability of debt financing serves as a critical factor propelling the dominance of this segment. Lenders including banks and direct credit funds are willing to provide capital for acquisitions due to the strong covenant protection and asset backing typical of UK mid market companies. According to data from the Bank of England corporate lending to non financial businesses remained resilient with billions of pounds allocated to merger and acquisition activities annually. The competition among lenders has led to innovative financing structures such as unitranche facilities which simplify the capital stack and accelerate deal execution. As per reports from PitchBook the average debt multiple for mid market deals in the UK stands at 4 to 5 times earnings providing substantial leverage for equity sponsors. This access to capital allows private equity firms to pursue larger transactions and achieve higher internal rates of return. The presence of institutional investors in the direct lending space has further diversified funding sources reducing reliance on traditional banking channels. Interest rate hedging instruments enable borrowers to manage exposure to fluctuating rates making long term debt more attractive. The efficiency of the UK legal system in enforcing security interests gives lenders confidence to commit capital. This supportive credit environment ensures that leveraged buyouts remain the preferred method for acquiring mature businesses with predictable cash flows.

The abundance of mature mid market companies with stable and predictable cash flows fundamentally drives the preference for LBOs. These businesses often operate in fragmented industries such as professional services industrial manufacturing and healthcare where consolidation opportunities are plentiful. According to data from the Confederation of British Industry small and medium enterprises contribute significantly to economic output and many have reached a stage where professionalization and scale are necessary for further growth. Private equity firms identify these entities as ideal candidates for leveraged acquisitions because their consistent earnings can reliably service debt obligations. As per surveys by the Institute of Directors many family owned businesses seek exit routes that ensure legacy preservation while providing liquidity to founders. The operational maturity of these companies allows private equity owners to implement efficiency improvements without disrupting core business functions. Standardized accounting practices and established customer bases reduce the risk associated with post acquisition integration. The ability to generate free cash flow enables portfolio companies to pay down debt rapidly enhancing equity value over time. This stability appeals to limited partners who seek consistent returns with lower volatility compared to early stage investments. The structural characteristics of the UK mid market thus create a fertile environment for leveraged buyout strategies to thrive and deliver superior risk adjusted returns.

Venture Capital

The venture capital segment is anticipated to witness the fastest CAGR of 12.5% over the forecast period. This rapid expansion of the segment is fueled by the vibrant innovation ecosystem in the UK particularly in technology life sciences and fintech sectors. Entrepreneurs are increasingly launching high growth startups that require substantial early stage capital to develop products and scale operations. Government initiatives such as tax relief schemes encourage individual and institutional investment in early stage ventures. The success of previous exits including initial public offerings and trade sales has generated significant recycled capital for reinvestment into new startups. Global investors are attracted to the UK due to its world class universities and research institutions that produce cutting edge intellectual property. The concentration of talent in hubs like London Cambridge and Oxford provides startups with access to skilled workforce. Venture capital firms offer not only capital but also strategic guidance and networks that are crucial for young companies. This supportive environment fosters innovation and drives the rapid growth of the venture capital segment as it becomes an essential component of the national economy.

The thriving technology and innovation ecosystem in the country is a key reason for the rapid growth of this segment. The country boasts a dense network of incubators accelerators and research parks that nurture early stage companies from ideation to commercialization. The Tech Nation report highlights robust investor confidence in the UK tech ecosystem, which regularly raises over £16 billion annually, retaining its title as the premier tech investment hub in Europe. London remains a global fintech hub attracting significant venture capital due to its regulatory sandbox and access to financial markets. Universities such as Imperial College London and the University of Oxford spin out numerous deep tech startups in artificial intelligence and biotechnology each year. As per reports from the Alan Turing Institute collaboration between academia and industry facilitates the transfer of advanced technologies into viable business models. The availability of specialized talent in software engineering data science and product management supports rapid product development. Venture capitalists are drawn to this ecosystem because it offers a high volume of investable opportunities with global scalability potential. The culture of entrepreneurship is supported by mentorship programs and networking events that connect founders with experienced investors. This dynamic environment ensures a continuous flow of innovative ventures requiring capital thus driving the expansion of the venture capital segment.

Supportive government policies and tax incentives play a crucial role in accelerating the growth of this segment. Schemes such as the Enterprise Investment Scheme and Seed Enterprise Investment Scheme provide substantial tax reliefs to individual investors who back high risk early stage companies. According to data from HM Revenue and Customs these schemes have facilitated billions of pounds in investment into thousands of startups since their inception. The tax benefits include income tax relief capital gains tax exemption and loss relief which significantly de risk early stage investing for angels and syndicates. As per analysis from the British Venture Capital Association these incentives have been instrumental in bridging the equity gap for seed and early stage firms. The government also offers research and development tax credits that reduce the cost burden for innovative companies allowing them to extend their runway. Regulatory sandboxes in sectors like financial services allow startups to test new products in a controlled environment fostering innovation. Public funding bodies such as Innovate UK provide grants that complement private venture capital enabling deeper technological development. These policy measures create a favorable investment climate that attracts both domestic and international venture capital. The alignment of public policy with private investment goals ensures sustained growth and resilience in the venture capital market.

By Industry Insights

Consumer and Retail

The consumer and retail segment led the United Kingdom private equity market and captured a 24.7% share in 2025. This leading position of the segment is attributed to the large size of the domestic consumer base and the fragmentation of the retail landscape. Private equity firms are attracted to established brands with loyal customer bases that can be scaled through digital transformation and operational improvements. Office for National Statistics (ONS) data confirms that retail sales represent approximately one-third of total UK household expenditure, creating a substantial revenue baseline often targeted by consumer-focused investment portfolios. The shift toward omnichannel retailing offers opportunities for investors to integrate online and offline experiences enhancing customer engagement. The sector includes diverse sub segments such as food and beverage fashion and home goods allowing for diversified investment strategies. Private equity owners often implement cost reduction initiatives and expand geographic reach to drive growth. The resilience of consumer spending even during economic downturns supports the defensive nature of these investments. Brand equity in the UK retail sector is strong offering potential for international expansion. The ability to consolidate smaller players into larger platforms creates economies of scale and bargaining power with suppliers. This combination of market size operational complexity and brand value ensures that Consumer and Retail remains the most active sector for private equity deployment.

Resilient consumer spending patterns in the country helps drive the dominance of this segment. Despite economic fluctuations UK households maintain a consistent level of expenditure on essential and discretionary goods supporting the revenue stability of retail businesses. Private equity firms favor this sector because predictable cash flows facilitate debt servicing and valuation certainty. The diversity of the consumer base across different demographic groups allows for targeted investment strategies in niche markets such as premium health foods or sustainable fashion. The loyalty of UK shoppers to established brands provides a moat against new entrants protecting market share. Private equity investors leverage this stability to implement long term strategic changes without immediate pressure on short term results. The recovery of foot traffic in high streets combined with robust online sales creates a balanced revenue mix. This dual channel approach mitigates risks associated with single distribution models. The enduring nature of consumer demand ensures that retail assets remain attractive targets for private equity capital seeking steady returns.

The high degree of fragmentation in this segment gives significant consolidation opportunities that drive PE activity. The market comprises thousands of independent retailers and regional chains that lack the scale to compete effectively with larger entities. Private equity firms acquire platform companies and subsequently add smaller competitors to achieve economies of scale in procurement logistics and marketing. The fragmentation also allows for specialization where private equity firms focus on specific niches such as pet care or specialty coffee building dominant positions. Integration of disparate systems and brands requires operational expertise which private equity owners provide. The resulting larger entities are better positioned to negotiate with suppliers and invest in technology. This consolidation trend improves overall sector efficiency and competitiveness. The availability of numerous small targets ensures a continuous deal flow for private equity firms pursuing inorganic growth strategies in the consumer sector.

Healthcare

The Healthcare segment is likely to experience the fastest CAGR of 14.2% between 2026 and 2034 due to demographic trends including an aging population and increasing prevalence of chronic diseases which elevate demand for medical services. Private equity firms are actively investing in healthcare providers such as dental practices veterinary clinics and care homes to capitalize on these structural tailwinds. The fragmentation of healthcare services allows for consolidation strategies that improve operational efficiency and patient outcomes. Government outsourcing of certain health services to private providers opens additional avenues for investment. Technological advancements in telemedicine and digital health records enhance the scalability of healthcare businesses. Private equity capital enables these companies to expand capacity and adopt new technologies faster than publicly funded counterparts. The defensive nature of healthcare revenues which are less sensitive to economic cycles attracts institutional investors. Regulatory support for private provision in non acute care settings further facilitates market entry. This convergence of demographic necessity and operational opportunity propels the healthcare segment to the forefront of private equity growth.

The aging population in the United Kingdom is a fundamental driver for the rapid growth of the Healthcare segment. As life expectancy increases the demand for age related medical services long term care and assisted living facilities rises substantially. Private equity firms invest in care home operators and home care providers to meet this growing demand. The complexity of managing chronic conditions such as dementia and diabetes requires specialized facilities and trained staff which private equity backed companies can provide through standardized protocols. This preference drives revenue growth for private healthcare providers. The shortage of public sector capacity further pushes patients toward private alternatives. Private equity investors bring capital to expand facility networks and improve service quality. The recurring nature of care services ensures stable cash flows and high retention rates. This demographic inevitability provides a secure foundation for long term investment thesis in the healthcare sector.

The increasing outsourcing of non-acute care services by the public sector to private providers creates significant opportunities for PE investment in this segment. The National Health Service faces budget constraints and capacity pressures leading it to contract out services such as diagnostics elective surgeries and community care to private operators. Private equity backed companies are well positioned to win these contracts due to their operational efficiency and ability to scale quickly. This trend allows private equity firms to secure long term revenue streams backed by government contracts. The reliability of public sector payments reduces credit risk for investors. Additionally the focus on preventive care and community health opens new markets for private providers. Private equity capital enables investment in digital health platforms that support remote monitoring and patient engagement. This strategic alignment with public health goals ensures sustainable growth for the healthcare segment. The partnership between public and private sectors thus drives the expansion of private equity activity in healthcare.

COUNTRY ANALYSIS

United Kingdom Leads European Private Equity Activity

The United Kingdom dominated the European private equity market and accounted for a 30.3% share in 2025 because of London’s status as a global financial center with deep capital pools and extensive professional services infrastructure. It benefits from a mature legal framework based on English common law which is widely trusted for international transactions. The British Private Equity and Venture Capital Association (BVCA) represents more than 600 member firms, reflecting a highly competitive and deeply established UK private capital ecosystem. The depth of talent in finance law and operations supports complex deal structures and post acquisition value creation. The UK serves as a gateway for international investors seeking exposure to European assets due to its language advantage and regulatory transparency. Economic resilience and a diverse industrial base provide a wide range of investment opportunities across sectors. The presence of major institutional investors such as pension funds ensures a steady supply of domestic capital. Cross border transactions are facilitated by the UK extensive network of trade agreements and financial connections. This combination of structural advantages maintains the UK position as the premier destination for private equity investment in Europe.

The deep capital pools and strong institutional support in the UK fundamentally drive its top position in the European market. UK pension funds and insurance companies are among the largest allocators to alternative assets globally providing a stable base of domestic capital. According to data from the Pensions and Lifetime Savings Association UK pension funds hold trillions of pounds in assets with a growing percentage allocated to private equity for enhanced returns. This domestic capital reduces reliance on foreign funding and provides stability during global market volatility. Institutional investors in the UK have sophisticated due diligence capabilities and long term investment horizons that align well with private equity cycles. As per Mercer, there is sustained institutional confidence in private markets, with the firm implementing blueprints to phase in a 10% to 15% target allocation for UK default growth funds by 2030. The presence of fund of funds and secondary market specialists adds liquidity and flexibility to the ecosystem. Government backed initiatives such as the British Business Bank also support smaller funds and venture capital activities. This robust capital infrastructure ensures that promising deals are adequately funded. The synergy between institutional investors and general partners fosters a collaborative environment that promotes best practices and innovation. This financial depth is a key differentiator that sustains the UK market dominance.

The robust legal and regulatory framework in the country provides a secure and predictable environment that attracts PE investment from around the world. English law is renowned for its clarity fairness and enforceability making it the preferred choice for international commercial contracts. According to the Law Society of England and Wales, English law is a preeminent legal framework globally, governing roughly 40% of international corporate and financial transactions. The Financial Conduct Authority provides clear guidelines for fund management and investor protection ensuring market integrity. Also, the legal certainty reduces transaction risks and costs for investors. The regulatory regime balances oversight with flexibility allowing for innovation in financial products and structures. Transparency requirements ensure that investors have access to accurate information for decision making. The independence of the judiciary guarantees fair treatment in case of disputes. This stable legal environment encourages long term commitment from international investors. The reputation of the UK regulatory system enhances the credibility of UK based funds globally. This foundational strength supports the continued growth and prominence of the UK private equity market.

COMPETITIVE LANDSCAPE

The United Kingdom private equity market features intense competition characterized by established global giants and specialized boutique firms vying for attractive investment opportunities. Major players leverage extensive resources and brand recognition to secure large cap deals while niche operators differentiate through deep sector knowledge and personalized service. The competitive landscape is shaped by the abundance of dry powder which drives up valuations and compresses returns for acquirers. Firms compete fiercely for talent recruiting experienced operators and investment professionals to enhance value creation capabilities. Regulatory scrutiny adds complexity requiring strict adherence to compliance standards which can slow transaction timelines. The rise of direct lending provides alternative financing options reducing reliance on traditional banks and altering deal structures. Cross border competition is significant as international funds target UK assets due to favorable legal frameworks. Success depends on building strong relationships with founders and demonstrating clear value addition beyond capital provision. This dynamic environment drives continuous innovation in deal structuring and operational support benefiting portfolio companies through improved efficiency and strategic direction.

KEY MARKET PLAYERS

A few of the dominant market players that are in the UK private equity market are

- Blackstone (U.S.)

- KKR & Co. (U.S.)

- Apollo Global Management (U.S.)

- The Carlyle Group (U.S.)

- Bridgepoint Group

- TPG (U.S.)

- Bain Capital (U.S.)

- Warburg Pincus (U.S.)

- Thoma Bravo (U.S.)

- Vista Equity Partner (U.S.)

- EQT (Sweden)

- CVC Capital Partners (Luxembourg)

- Advent International (U.S.)

- Permira (U.K.)

- Ardian (France)

- Hellman & Friedman (U.S.)

Top Players In The Market

- CVC Capital Partners operates as a leading global investment firm with a significant footprint in the United Kingdom private equity landscape. The company focuses on buyout and growth capital investments across various sectors including healthcare technology and consumer goods. CVC recently raised substantial funds to support its expansion into mid market deals targeting resilient businesses. The firm strengthens its position by leveraging operational expertise to drive value creation within portfolio companies through digital transformation initiatives. CVC actively engages with management teams to implement strategic improvements and enhance sustainability practices. Their commitment to environmental social and governance criteria aligns with evolving investor expectations. By fostering long term partnerships with founders CVC ensures stable growth and successful exits. This approach reinforces their reputation as a trusted partner for ambitious UK enterprises seeking capital and strategic guidance.

- Permira is a prominent global investment firm that plays a vital role in the United Kingdom private equity market through strategic buyouts and growth investments. The firm targets high quality businesses in technology services and consumer sectors offering patient capital and operational support. Permira recently expanded its team in London to enhance its deal sourcing capabilities and sector expertise. The company focuses on partnering with management teams to accelerate international expansion and innovation. Permira integrates advanced data analytics into its investment process to identify value creation opportunities effectively. Their recent initiatives include supporting portfolio companies in adopting artificial intelligence and cloud technologies. By prioritizing sustainable business practices Permira attracts institutional investors seeking responsible investment options. This strategic focus on operational excellence and technological advancement solidifies their standing as a key contributor to the UK economy.

- Bridgepoint Group specializes in advising and investing in small and medium sized enterprises across the United Kingdom and Europe. The firm provides private equity capital and strategic advice to help companies achieve their growth ambitions. Bridgepoint recently launched new funds dedicated to supporting secondary buyouts and succession planning for family owned businesses. The company leverages its extensive network to facilitate add on acquisitions for platform companies. Bridgepoint emphasizes hands on involvement working closely with entrepreneurs to professionalize operations and improve governance. Their focus on niche markets allows for tailored solutions that address specific industry challenges. By maintaining a strong presence in the mid market Bridgepoint supports job creation and economic stability. This dedicated approach to smaller enterprises distinguishes them in the competitive private equity landscape and drives consistent performance.

Major Strategies Used By Key Market Participants

Key players in the United Kingdom private equity market employ sector specialization as a primary strategy to deepen expertise and enhance value creation capabilities. Firms focus on specific industries such as healthcare technology or consumer goods allowing them to identify nuanced opportunities and risks. Operational improvement remains central with investors deploying dedicated teams to optimize supply chains and implement digital tools. Environmental social and governance integration is increasingly critical as firms align portfolios with sustainability goals to attract institutional capital. Buy and build strategies are widely used to consolidate fragmented markets achieving economies of scale and enhanced market power. Secondary transactions provide liquidity options for existing investors while allowing new funds to acquire mature assets with reduced execution risk. Talent acquisition initiatives ensure portfolio companies have leadership capable of driving growth. These multifaceted approaches enable participants to generate superior returns while navigating complex regulatory and economic landscapes in the dynamic UK market.

MARKET SEGMENTATION

This research report on the UK private equity market is segmented and sub-segmented into the following categories.

By Type

- Leveraged Buyouts (LBOs)

- Venture Capital

- Real Estate Private Equity

- Distressed and Special Situations

- Others

By Industry

- Technology

- Healthcare

- Consumer & Retail

- Financial Services

- Others

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment