As global markets navigate a landscape marked by economic resilience and inflationary pressures, Asia’s equities are drawing attention for their potential growth opportunities. In this environment, companies with high insider ownership often stand out as they suggest strong confidence from those closest to the business, making them compelling options for investors seeking alignment of interests and potential long-term value.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.5% | 31.5% |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 69.3% |

| Shanghai Biren Technology (SEHK:6082) | 11% | 120.7% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| Meitu (SEHK:1357) | 22.7% | 31.5% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.9% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.6% |

| Great Microwave Technology (SHSE:688270) | 21.1% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.2% | 38.2% |

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ubtech Robotics Corp Ltd focuses on the research, design, development, production, commercialization, marketing, and sale of robotic products and services across China, Hong Kong, and international markets with a market cap of HK$59.15 billion.

Operations: The company’s revenue primarily comes from its Industrial Automation & Controls segment, which generated CN¥2.00 billion.

Insider Ownership: 32.9%

Revenue Growth Forecast: 48.1% p.a.

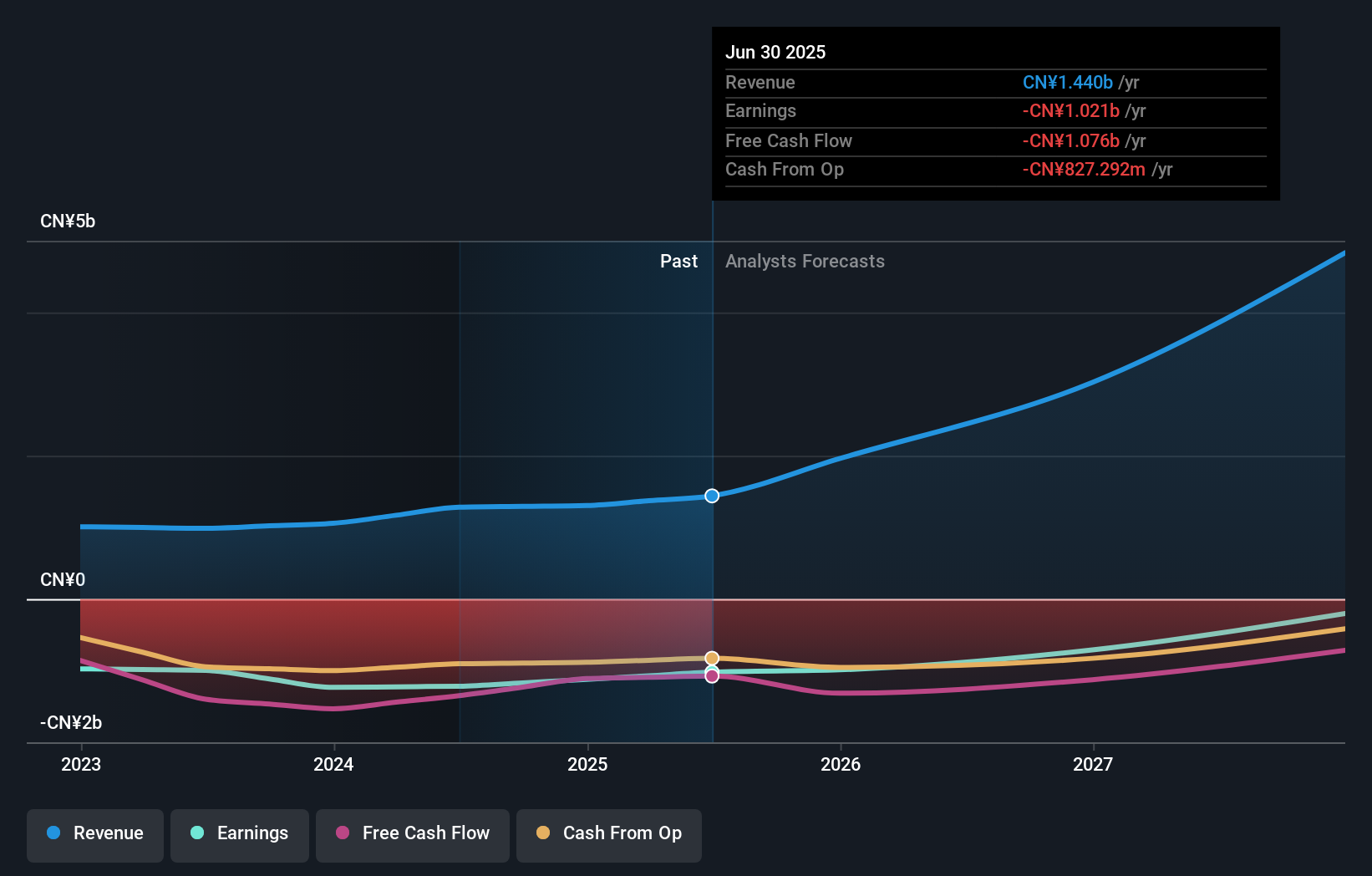

Ubtech Robotics is experiencing significant growth, with revenue projected to increase by 48.1% annually, outpacing the Hong Kong market’s 8.7% growth rate. Despite a net loss of CNY 703.19 million in 2025, this marks an improvement from the previous year’s larger deficit. Analysts expect profitability within three years and forecast earnings growth at over 100% per year. Trading at a substantial discount to its estimated fair value suggests potential upside for investors focused on high-growth stocks with insider ownership dynamics in Asia.

Simply Wall St Growth Rating: ★★★★★☆

Overview: KEDE Numerical Control Co., Ltd. manufactures and markets CNC systems and functional components in China with a market cap of CN¥8.75 billion.

Operations: KEDE Numerical Control generates its revenue from the production and sale of CNC systems and functional components within China.

Insider Ownership: 22.7%

Revenue Growth Forecast: 24.8% p.a.

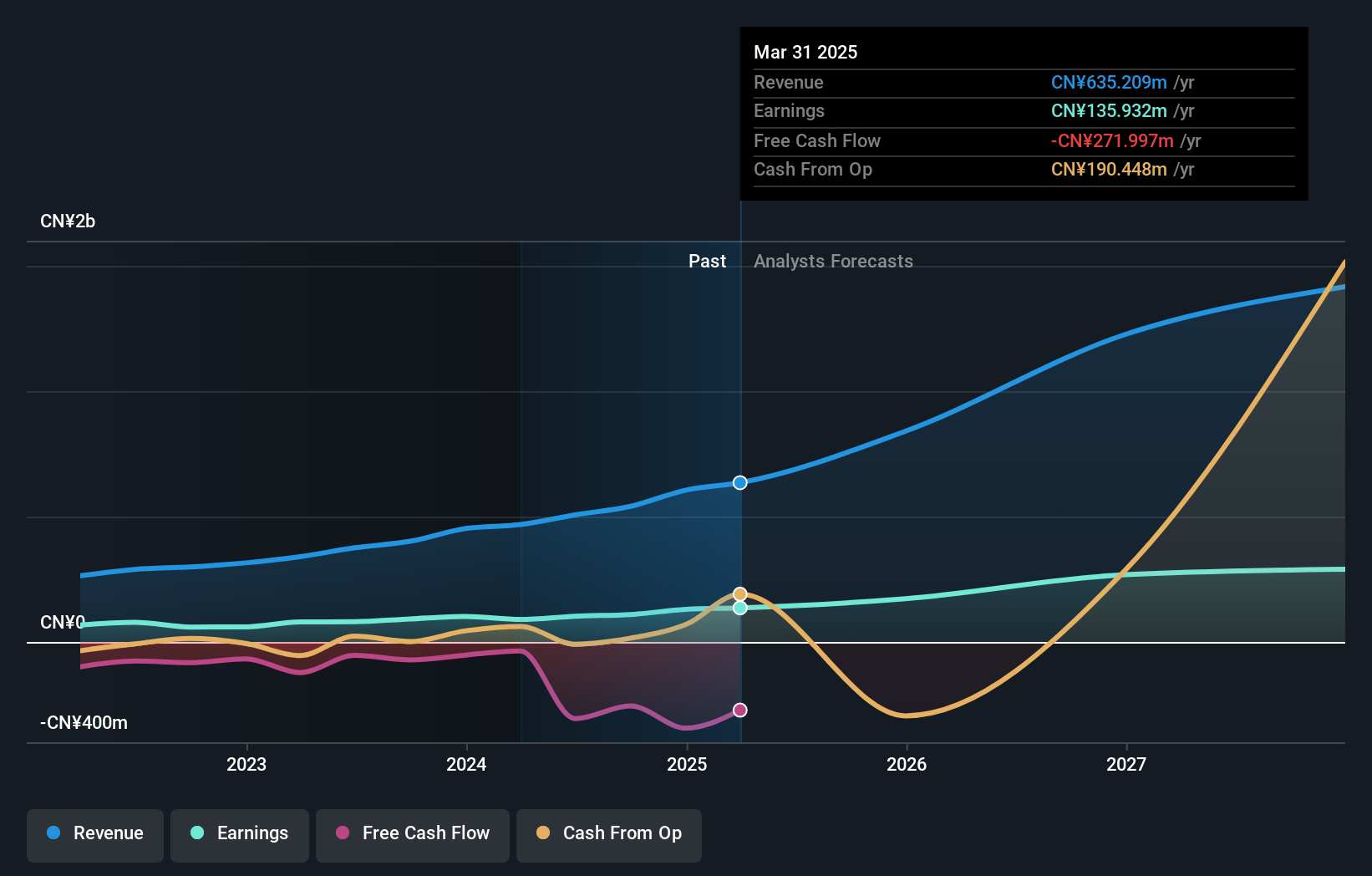

KEDE Numerical Control is poised for growth, with revenue expected to rise 24.8% annually, surpassing the Chinese market’s average. Earnings are projected to grow at 30.1% per year, outpacing the market’s 27%. Recent Q1 results showed net income of CNY 22.55 million, up from CNY 21.1 million a year ago, despite a decrease in sales to CNY 108.09 million from CNY 130.86 million, highlighting resilience amid challenges.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Megmeet Electrical Co., LTD is an electrical automation company based in China with a market cap of CN¥86.18 billion.

Operations: The company’s revenue is derived from its operations in electrical automation, with total revenue reported in millions of CN¥.

Insider Ownership: 30.7%

Revenue Growth Forecast: 31.5% p.a.

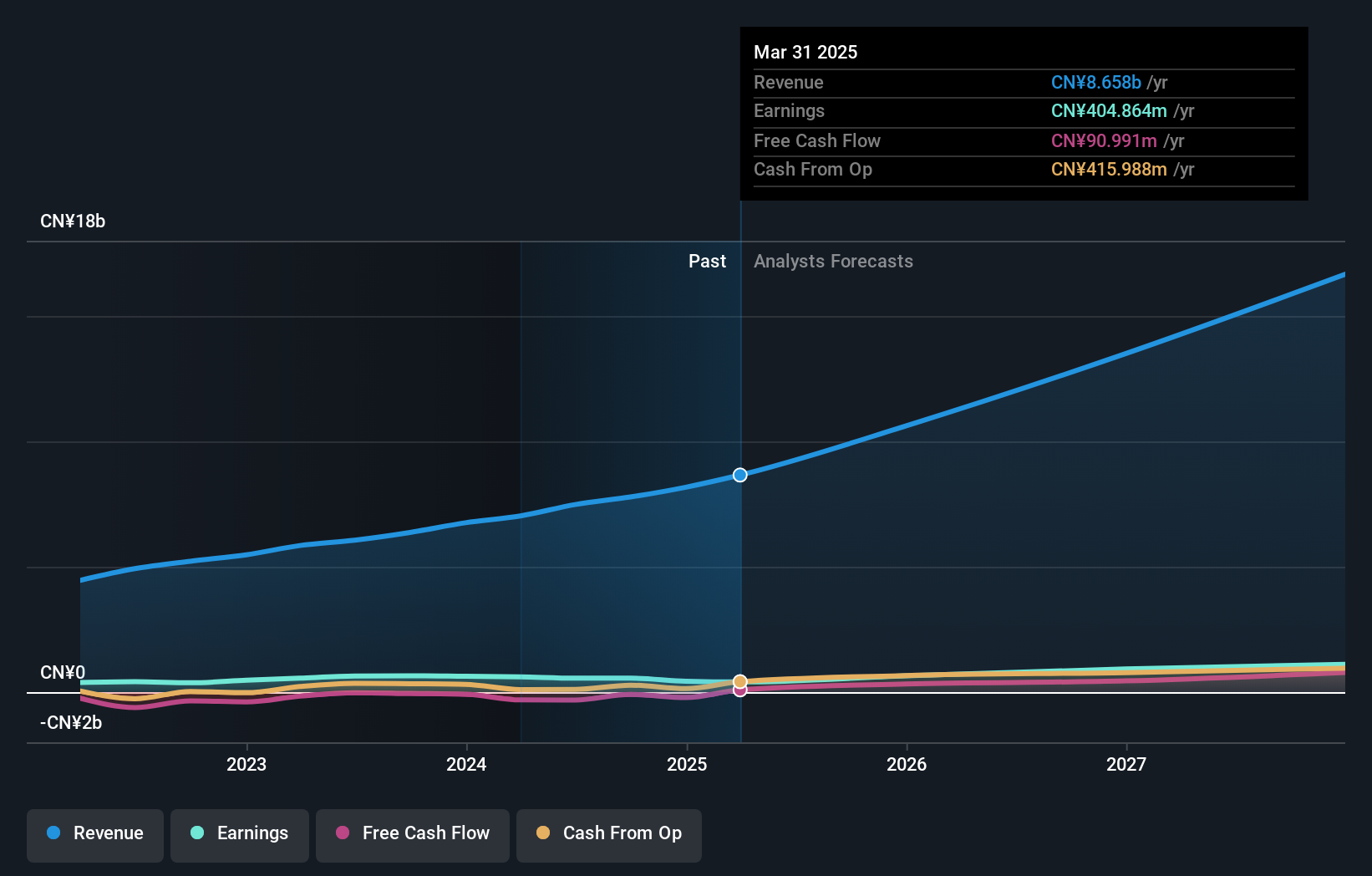

Shenzhen Megmeet Electrical shows promising growth potential, with revenue projected to increase by 31.5% annually, surpassing the Chinese market’s average of 16.3%. Earnings are expected to grow significantly at 68.2% per year, well above the market’s 27%. Despite recent volatility in share price and a decrease in profit margins from 4.7% to 1.6%, Q1 results showed improved sales of CNY 2.79 billion and net income of CNY 114.69 million compared to last year.

Seize The Opportunity

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment