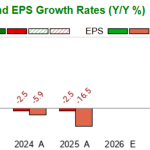

Property casualty insurer Cincinnati Financial (NASDAQ:CINF) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 11.4% year on year to $2.93 billion. Its non-GAAP profit of $2.10 per share was 8.2% above analysts’ consensus estimates.

Is now the time to buy CINF? Find out in our full research report (it’s free for active Edge members).

Cincinnati Financial (CINF) Q1 CY2026 Highlights:

- Revenue: $2.93 billion vs analyst estimates of $2.94 billion (11.4% year-on-year growth, in line)

- Adjusted EPS: $2.10 vs analyst estimates of $1.94 (8.2% beat)

- Adjusted EBITDA: $359 million (12.2% margin, 628% year-on-year growth)

- Operating Margin: 11.1%, up from -4.9% in the same quarter last year

- Market Capitalization: $25.79 billion

StockStory’s Take

Cincinnati Financial’s first quarter results reflected a combination of improved underwriting performance and disciplined premium growth, with management emphasizing the impact of lower catastrophe losses and ongoing pricing segmentation. CEO Stephen Michael Spray pointed to “an excellent 87.5% accident year combined ratio before catastrophe losses” and credited the company’s focus on risk selection and stable agent relationships as key contributors to the quarter’s profitability. The company also benefited from growth in its investment income and a sharp rebound in its property casualty operating margin compared to the prior year.

Looking ahead, management expects market conditions to normalize, with growth moderating as competitive pressures and lower renewal price increases take hold. Spray highlighted that “growth is slowing as our underwriters continue to emphasize pricing and risk segmentation on a policy-by-policy basis,” suggesting a shift from the accelerated expansion of recent years. The company is prioritizing profitable underwriting, maintaining pricing discipline, and leveraging its diversified business mix across commercial, personal, and specialty lines to navigate evolving industry trends.

Key Insights from Management’s Remarks

Management attributed the quarter’s results to lower catastrophe losses, improved investment income, and continued risk selection discipline, while noting that premium growth is moderating as market competition increases.

-

Lower catastrophe losses: The company saw a significant reduction in catastrophe-related claims, which improved combined ratios across its property casualty and personal lines businesses. This contributed to a strong underwriting result, particularly in personal lines where the combined ratio improved by over 50 percentage points year-over-year.

-

Slowing premium growth: Premium growth in commercial lines decelerated compared to prior periods, with renewal price increases moderating to the high end of the low single-digit range. Management cited increasing competition, particularly on larger accounts, as a factor leading to more selective underwriting and lower policy count growth in personal lines.

-

Investment income expansion: CFO Michael James Sewell noted investment income rose 14% year-over-year, driven by higher bond yields and increased cash flow from insurance operations. This included a meaningful special dividend from an equity holding, contributing to non-GAAP profitability.

-

Diversified business mix: The company’s specialty segments, Cincinnati Re and Cincinnati Global, continued to deliver strong underwriting margins and premium growth, benefiting from product expansion and geographic diversification. Management highlighted their limited exposure to high-risk areas such as the Middle East.

-

Agency network growth: The company made 108 new agency appointments during the quarter, with management underscoring the importance of maintaining high standards for agency quality and prioritizing appointments in states with favorable risk-adjusted returns.

Drivers of Future Performance

Cincinnati Financial’s outlook is shaped by a focus on underwriting discipline, moderating premium growth, and the ongoing impact of competitive pressures across its core business lines.

-

Emphasis on pricing discipline: Management expects that as industry competition intensifies, renewal price increases may continue to moderate, particularly in commercial lines. The company intends to prioritize risk selection and avoid broad-based growth if pricing becomes inadequate, which may result in slower premium expansion but support profitability.

-

Shift in business mix: Growth in the high net worth and private client segments is expected to continue, but at a reduced pace as rate increases normalize and exposure units decline. Management sees geographic and product diversification—especially within Cincinnati Global and Cincinnati Re—as key to mitigating volatility and sustaining margins.

-

Social inflation and legal trends: Social inflation, referring to rising litigation costs and legal system abuse, remains a risk for casualty and auto lines. Management is cautious about the potential for adverse loss development, particularly in commercial auto, and will monitor tort reform efforts and adjust reserves as necessary.

Catalysts in Upcoming Quarters

In the quarters ahead, the StockStory team will be watching (1) the pace and sustainability of premium growth as competition increases, (2) the ability to maintain underwriting margins in the face of moderating price increases and persistent social inflation, and (3) how the company manages agency expansion while preserving its selective approach. Additionally, developments in legal reform and shifts in the investment yield environment will be important to track for their effect on earnings stability.

Cincinnati Financial currently trades at $166.51, in line with $165.64 just before the earnings. Is the company at an inflection point that warrants a buy or sell? The answer lies in our full research report (it’s free).

Now Could Be The Perfect Time To Invest In These Stocks

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment