(Bloomberg) — The software problem roiling private markets is about to face a big new test. A wall of debt maturities is looming for the industry just as artificial intelligence threatens to upend entire businesses in what’s been dubbed the SaaSpocalypse.

More than $330 billion of high yield, leveraged loan and business development company-linked software and technology debt is coming due for repayment through 2028, a chunk of it tied to firms owned by private markets. As companies look to refinance in the coming months, they face numerous headwinds, from fears about AI devaluing or replacing their products to the risk of higher borrowing costs spurred by the war in the Middle East.

Some private credit funds are turning away software borrowers outright as they seek to shrink their exposure to the sector, according to people with knowledge of the matter. And a number of software company sales planned by private equity have already stalled.

“Software borrowers from private-credit funds are more highly leveraged and more dependent on future growth expectations than borrowers in other industries, making them more sensitive to adverse shocks,” according to researchers at MSCI Inc.

The following charts highlight the stress facing private equity and credit markets as their big bet on software sours.

Private market managers allocated hundreds of billions of dollars to software over the last 15 years, betting that software-as-a-service (SaaS) business models would generate high growth and reliable cashflows. That focus became increasingly concentrated during the period, with software and technology services accounting for about half of all private equity deals in recent years, far surpassing any other industry.

For almost two decades that concentration risk was justified by market-beating returns for funds that marketed themselves as investing in technology among other industries. In recent years, however, the premium has been shrinking as more and more funds piled into the industry.

Private markets accelerated their focus on software during the period of low interest rates that followed the pandemic. Valuations soared, culminating in a record amount of M&A in the industry by PE and venture firms in 2021. Those deals are now dragging down performance after a failure to hedge sent borrowing costs soaring and called marks into question.

At the same time, a rapid leap forward by AI tools over the last 18 months has made concentration on one industry look somewhat foolhardy. Many private market managers still reckon that those businesses will prove resilient.

Investors, however, are showing their concern: Many have been rushing for the exits from direct lending funds, leading managers to limit withdrawals from some semi-liquid vehicles. More broadly, valuations and debt pricing have been falling for companies that are heavily focused on software. In the leveraged loan market, the premium traditionally seen in technology loans has completely broken down this year.

That rising stress comes at just the wrong time for credit investors. Overall, more than $140 billion of technology company debt is maturing in 2028, which companies will probably start trying to refinance from the second half of this year.

The bulk of the maturity wall relates to loans originated during the pandemic era of cheap money, according to Citigroup Inc.’s Michael Anderson and Steph Choe. “The credit dates for a third of these loans are still 2021, meaning the issuer has not demonstrated capital market access in many years,” they wrote. “The average price of the 2021 vintage/2028 maturity is $83.40, signaling significant stress.”

The falling pricing for leveraged loans tied to software are a leading indicator for private credit, where marks can considerably lag public markets. Typically, when loan prices fall, a rising number of private credit borrowers subsequently face stress in the form of not earning enough to cover their interest costs.

As much as 15% of software direct lending could default in the coming years, Marathon Asset Management LP Chairman Bruce Richards said this week. Others are less concerned. While many private credit managers have as much as 30% of portfolios exposed to software and tech, their lending is usually at the top of the capital structure and relatively insulated from restructurings, according to Vivek Bantwal, global co-head of private credit at Goldman Sachs Asset Management LP.

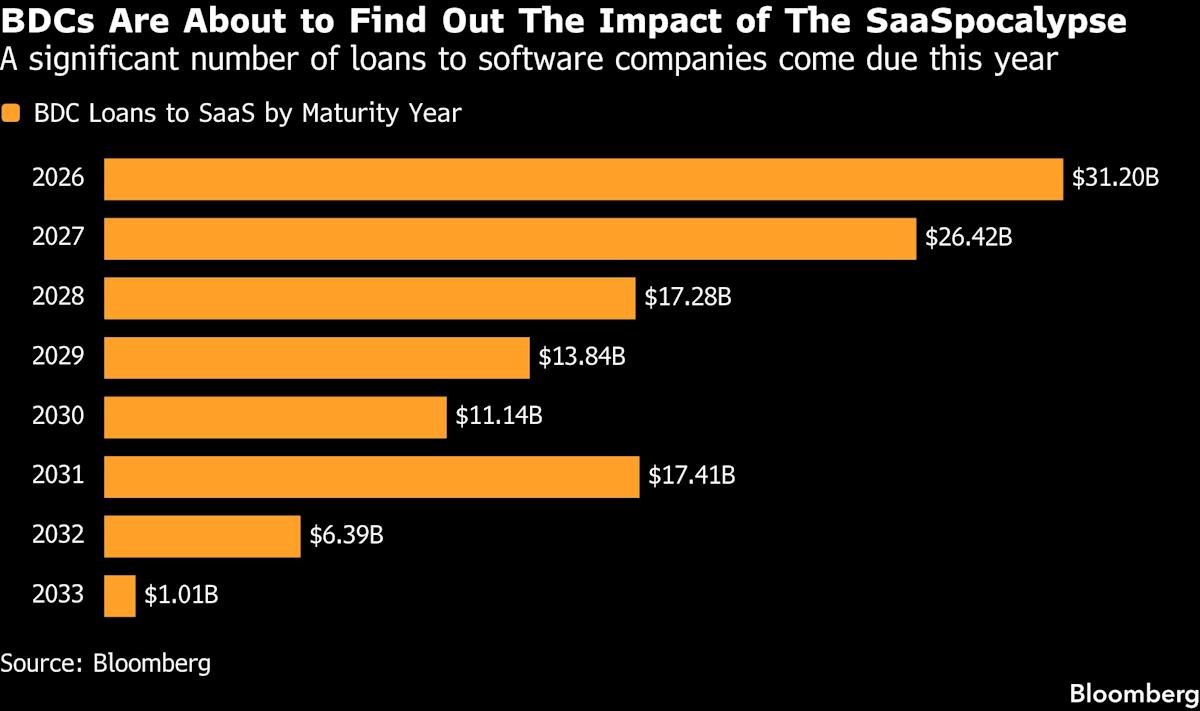

For business development companies, which lend to small and mid-size firms, a big test is coming even sooner than the 2028-maturity wave. More than $31 billion in debt tied to the software sector is coming due this year.

As the cost of credit increases, “higher interest expenses will hurt” weaker firms, meaning they will require additional equity from sponsors, said Ron Kahn, co-head of global valuations and opinions at adviser Lincoln International.

Some PE managers will examine selling portfolio firms in the hope that they can achieve a price that repays the debt, he said, while in other cases “private credit and private equity will kick the can down the road. The lender will get higher pricing and the company has time to rightsize itself.”

One fear for watchdogs is that private credit firms have been using a feature called payment-in-kind debt to mask weakness in their portfolios. PIK allows borrowers to push back interest payments until the debt itself has to be repaid.

‘Bad PIK’ — added during the life of the loan to relieve cash flow pressures — is used by Lincoln as a proxy for the default rate in private credit. The firm estimates that about 6.4% of borrowers from direct lenders had bad PIK in the fourth quarter, compared with 2.5% at the end of 2021. These borrowers also have soaring loan-to-value ratios, another sign of stress, Lincoln said.

Read: Private Credit’s Rising Pile of ‘Bad PIK’ Points to Default Woes

“For years there was a symbiotic relationship’’ between direct lenders and private equity, said Lincoln’s Kahn, but now sponsors are saying they won’t continue backing companies if they don’t see further value in them.

“People are looking after their own interests.”

–With assistance from Silas Brown, Tasos Vossos and James Crombie.

More stories like this are available on bloomberg.com

©2026 Bloomberg L.P.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment