Core inflation is a measure of inflation that aims to show the underlying, long-term trend of price changes in an economy, excluding the impact of components with volatile prices. In India, the main measure of core inflation has been the one that excludes food and fuel. However, economists and the central bank also look at some other measures.

-Consumer Price Index (CPI) excluding food, fuel, petrol and diesel

-CPI excluding food, fuel, petrol, diesel, gold and silver

-CPI excluding food, fuel, petrol, diesel, gold, silver and housing

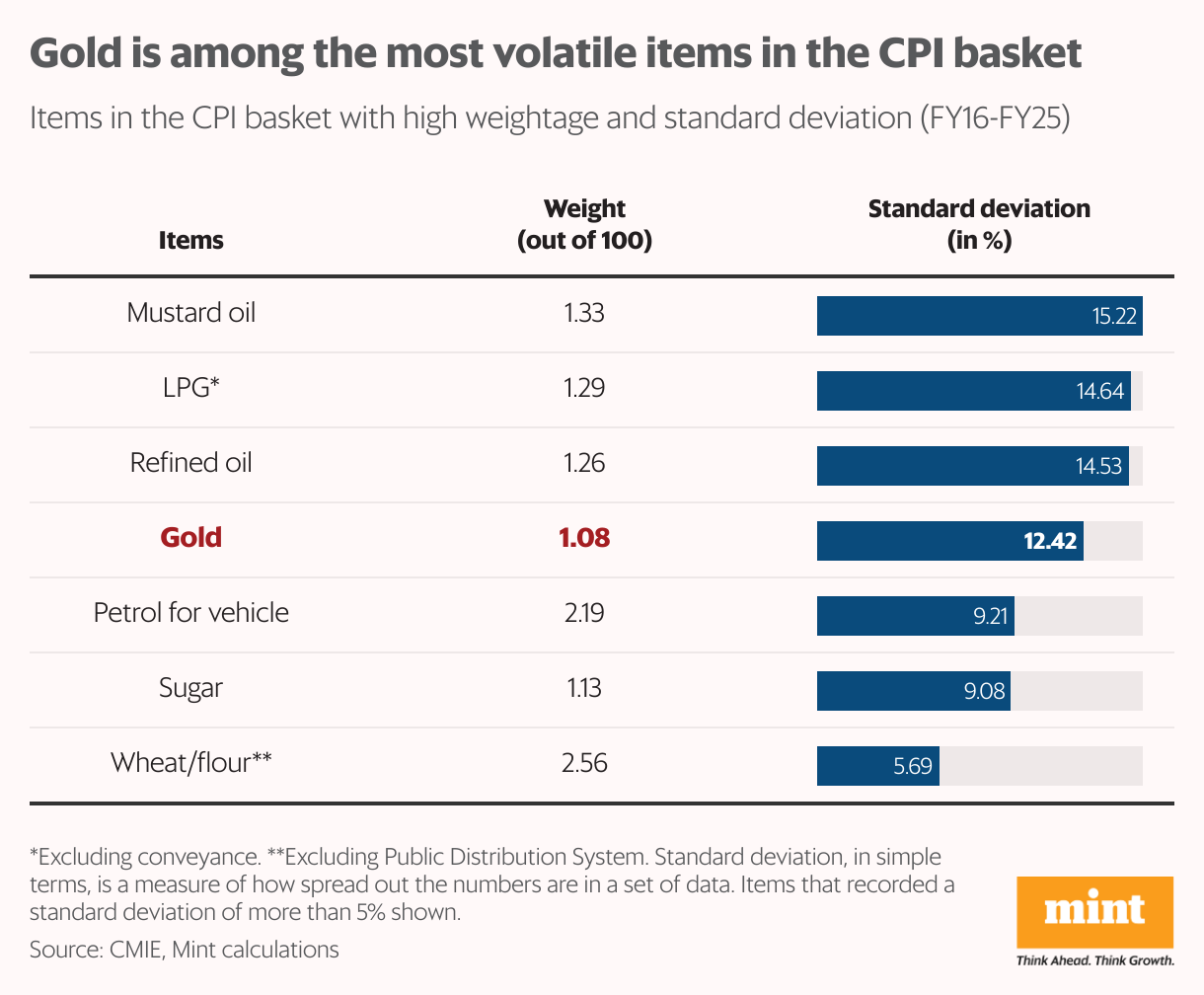

Against the backdrop of global uncertainty, the gold demand and prices have risen significantly, distorting the core inflation reading, a report by Crisil noted. Gold has 1.08% of the overall CPI basket. It has the 20th largest share among the 299 items that the government uses for measuring inflation.

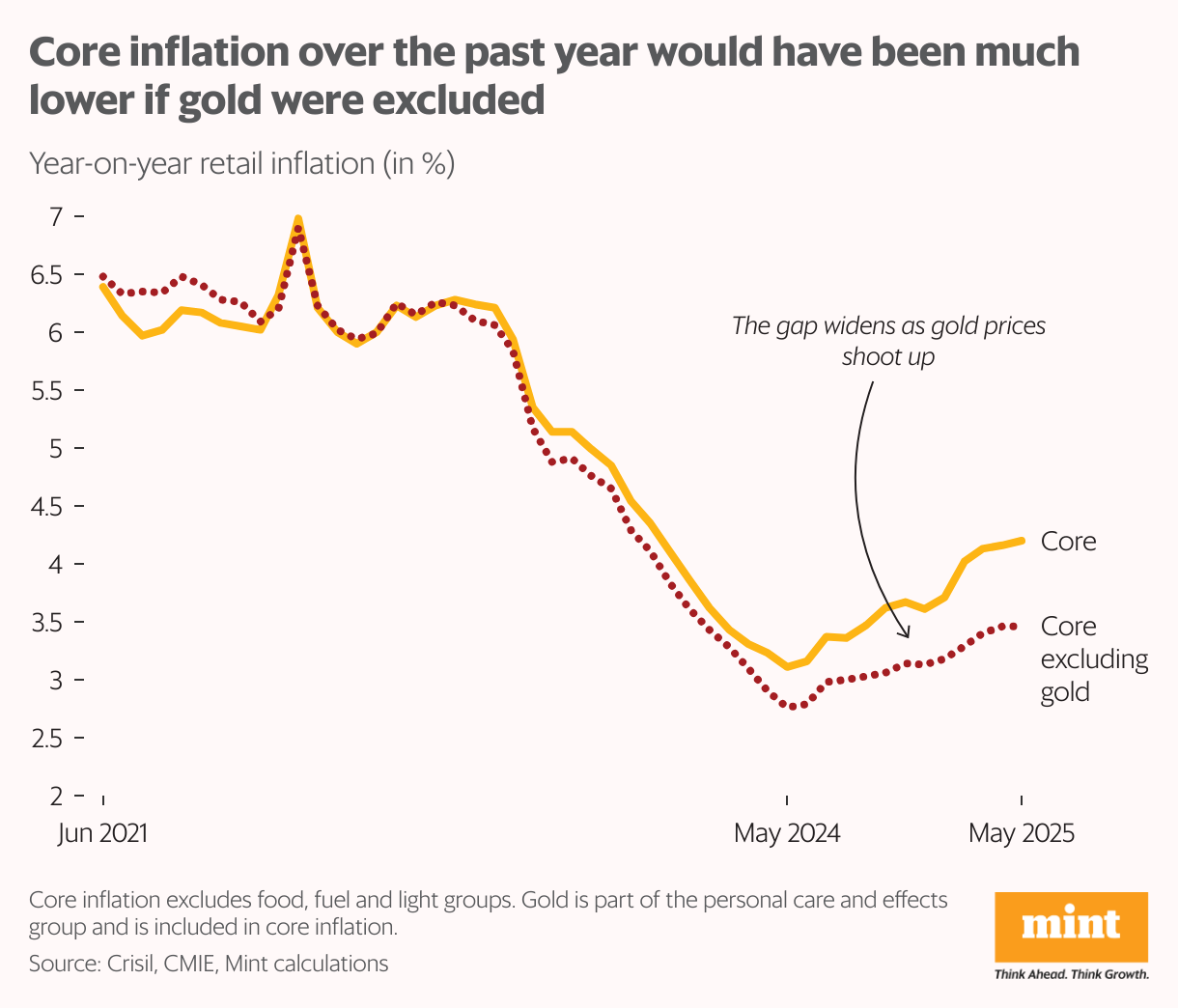

A Mint analysis of data for core inflation (excluding food and fuel) and core inflation excluding gold shows a sizeable gap between the metrics, underlining the impact of the recent surge. India’s core inflation would have been much lower (3.4%) had gold not been a part of it, as opposed to 4.2% recorded in May.

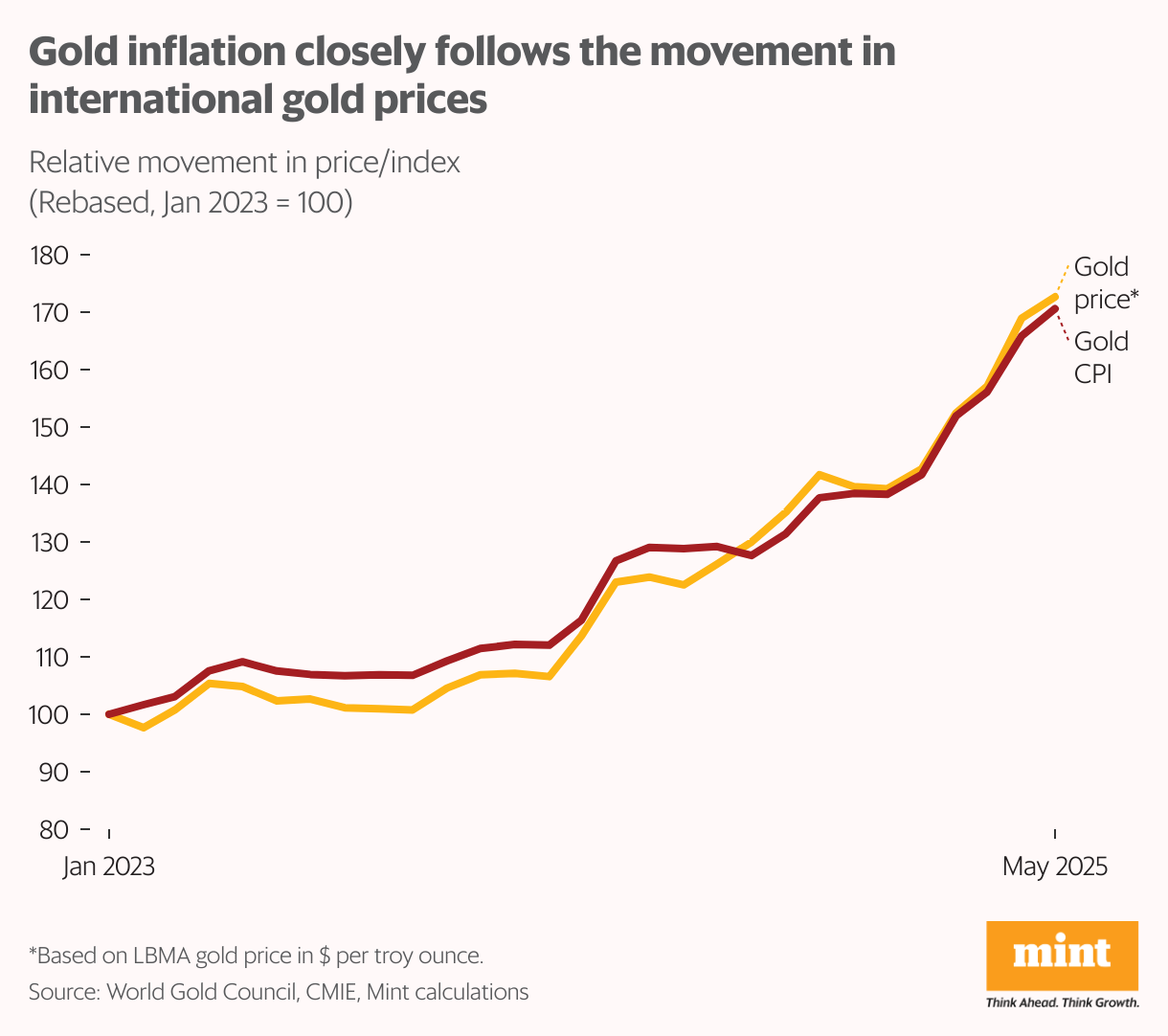

“The significant influence of global rather than domestic factors on gold prices in India warrants the exclusion of gold from the core inflation measure, particularly during periods of heightened global economic uncertainty,” Crisil said.

Gold’s grip

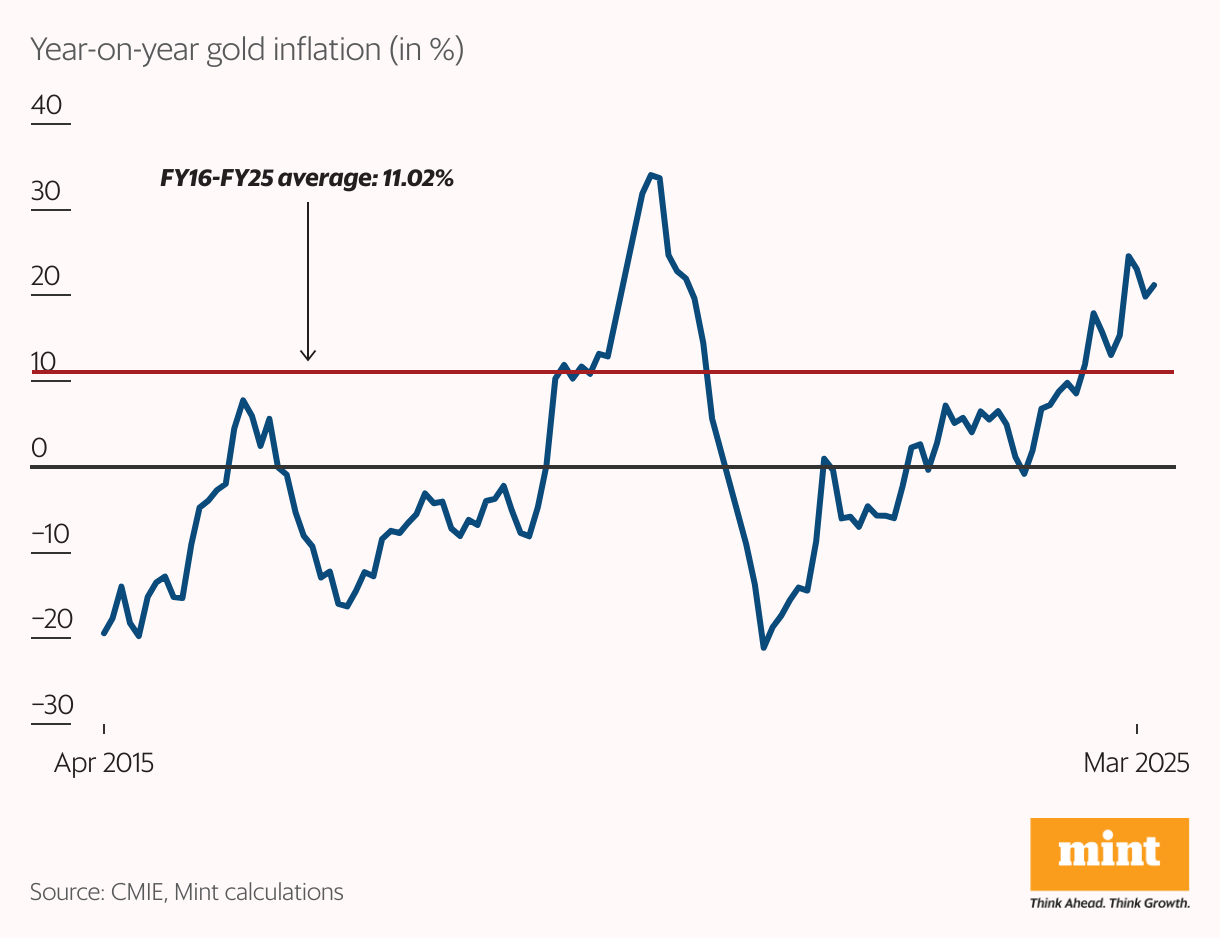

The primary driver for this global influence is gold’s role as a “safe-haven” investment. During periods of heightened global economic uncertainty, such as tariff disputes or geopolitical conflicts, demand for gold surges worldwide, leading to higher prices. In India, the trajectory of gold inflation in India is intertwined with global price movements. As noted by Crisil, data from 2015-2016 to fiscal year 2024-25 shows a strong correlation coefficient of 0.91 between global gold prices and India’s gold CPI. This means that when international gold prices shift, gold inflation quickly follows suit. Between January 2023 and May 2025, benchmark international gold prices rose 73% and gold inflation increased 71%.

The linkage with global prices also means that the central bank can do little to control its inflation. While many economists remove gold from overall inflation to see the underlying price trends, especially in times of sharp rises and declines, the main measure of core inflation is the guiding indicator.

Demand drive

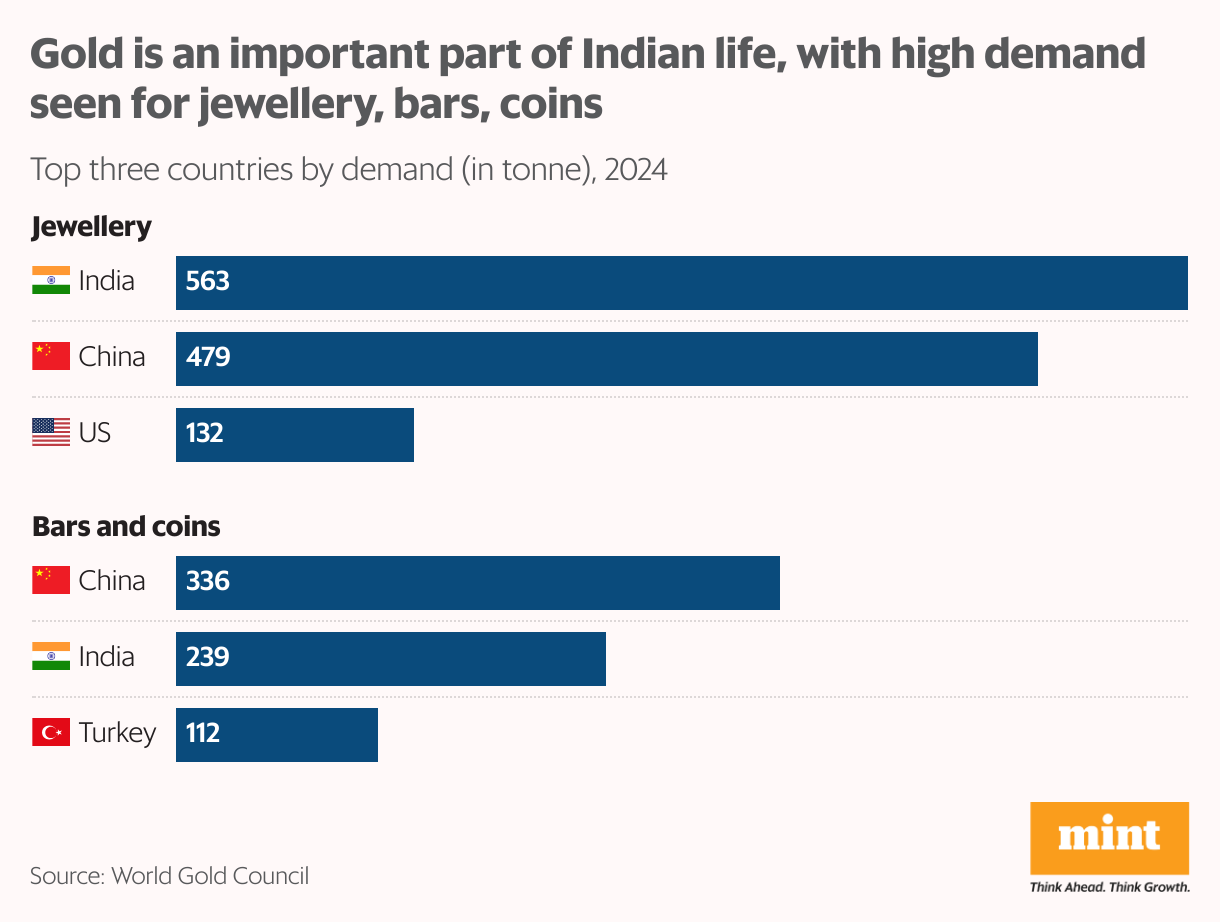

Gold holds a unique and enduring appeal for Indian households, hence underlying its high weightage in the inflation basket. India is one of the world’s largest gold markets, with total demand of 803 tonnes in 2024, second only to China (816 tonnes), according to World Gold Council data.

This marks the highest annual demand India has seen since 2015, when it touched 857.2 tonnes. When it comes to gold jewellery, India is the largest consumer, with demand at 563 tonnes in 2024, well ahead of China (479 tonnes), and the US (132 tonnes).

At the same time, investment demand for gold (in the form of bars and coins) reached 239 tonnes in 2024—a 29% rise from the previous year—showing the popularity of the yellow metal in various forms. This may be due to the strong response to the import duty on gold from 15% to 6%, announced by the finance minister in the Union Budget 2024.

Volatility worry

The problem, however, is not high weightage in the inflation basket, but the volatility in its prices. Gold prices are sensitive to developments around the world and can rise and fall sharply in a short duration, even as the average price rise turns out to be moderate. Gold inflation has shown significantly higher volatility in the past 10 years compared to other items.

In fact, the standard deviation in gold inflation between FY16 and FY25 stood at 12.4, sharply exceeding that of fuel and light (4.4) and food (3.6), Crisil noted. This heightened volatility means that it can distort inflation readings even as average underlying movement may be moderate.

In the past 10 years, gold inflation has overshot its average for the period in two instances: during the covid-19 pandemic and during the recent rally amid global uncertainty.