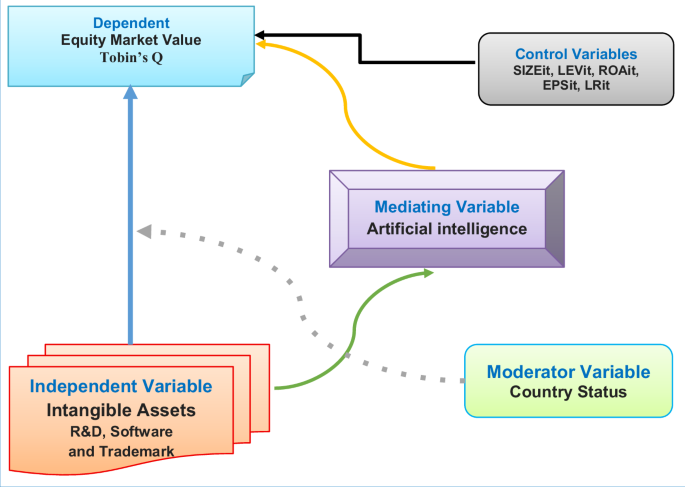

The connection between IA, EMV, and AI was tested using OLS regression after descriptive statistics, VIF, and correlation analyses. Researchers used correlation matrices to examine relationships among variables; panel regression models were specified to test the impact of variables and their coefficients. The results were as follows:

Descriptive analysis

The results of the descriptive analysis were estimated for 940 observations, including means, standard deviations, and min/max for all variables, separately for EM and DM sub-samples. Table 3 shows the descriptive results.

The results of Table 3 show that the mean of Tobin’s Q in EM was 5.48 vs. DM 9.85, with a maximum value of 46.99 vs. 72.45 in both EM and DM. The mean log size in EM was 9.966, vs. 4.32 in DM, and the maximum value was 452.35 in both EM and DM. The mean of ROA in EM was 0.15 vs. DM 0.18, with a maximum value of 0.45 vs. 0.79 in both EM and DM. The mean of Log IA in EM was 32.84 vs. DM 35.94, with a maximum value of 115.17 vs. 201.65 in both EM and DM. The mean of AI in EM was 2.618 vs. DM 3.519, with a maximum value of 415.04 vs. 524.54 in both EM and DM.

These results highlight significant differences between EM and DM. EM firms exhibit substantially lower market valuations (mean Tobin’s Q: 5.48 vs. 9.85) and profitability (mean ROA: 0.15 vs. 0.18) compared to DM firms, reinforcing the typical premium associated with DM. Surprisingly, EM firms appear drastically larger on average (mean log size: 9.966 vs. 4.32) and exhibit an extreme maximum size (452.35 vs. 93.50), suggesting the EM sample is with national currencies. Developed market firms hold significantly more IA on average (mean Log IA: 35.94 vs. 32.84) and achieve much higher maximum levels (max Log IA: 201.65 vs. 115.17). While DM shows a higher average level of AI activity (mean AI: 3.519 vs. 2.618), it also contains the firm with the highest AI intensity (max AI: 415.04 vs. 524.54). This suggests AI adoption might be more widespread but potentially shallower in DM.

Multi-collinearity analysis results

The test for multicollinearity was performed in Table 4 to determine whether multicollinearity exists in the data. The results show no multicollinearity, with an average VIF of 1.950 or lower.

The multicollinearity analysis, as presented in Table 4, shows that the VIF results indicate no significant multicollinearity among the independent variables in the model. All individual VIF values are well below the commonly accepted threshold of 5 (or 10), with the highest VIF of 1.950 for LRit and an average VIF also low. This suggests that the independent variables are not excessively correlated with each other, ensuring that the regression coefficients are reliable and their individual effects can be interpreted without significant distortion from multicollinearity.

Person correlation results

The results of the Pearson correlation test were examined in panel B in Table 5 to find the significant relationship between EMV and IA.

As shown in Table 5, there is a positive relationship between IA and EMV in the EM, with a Pearson correlation of 0.212, compared to 0.246 in DE at the 1% significance level. There is a positive relationship between AI and EMV in EM, with a Pearson correlation of 0.203, compared with 0.500 in DE at the 1% significance level. The correlation results presented in Table 5 reveal varying relationships between Tobin’s Q and the independent variables across emerging, developed, and total sample contexts. The firm size (SIZEit), leverage (LEVit), AI (AIit), and IA (IAit) consistently exhibit statistically significant positive correlations with Tobin’s Q across both emerging and DMts, indicating their general importance to firm valuation. However, profitability indicators, such as ROAit and EPSit exhibit stronger, more significant positive correlations with Tobin’s Q in established countries than in emerging countries, where the correlations are weak or non-significant. These findings demonstrate that, while some factors have a universal influence on business value, the market’s assessment of profitability and other financial measures can vary greatly depending on the country’s economic growth stage.

Hypothesis tests

To test the hypothesized relationships, we employed regression analysis with EMV as the dependent variable. Our analysis proceeded in two stages. First, we conducted simple regressions to examine the individual relationship between each category of IA and market value. Second, we specified a multiple regression model to assess the collective impact of all intangible asset variables, along with relevant control variables, on firm valuation. Results were as follows:

Results for the relationship between IA and EMV

The regression results for the first hypothesis are shown in Table 6.

H1. The impact of IA on EMV differs significantly between EM and DM.

Table 6 presents the regression results for the first hypothesis, disaggregated by emerging and developed countries, revealing distinct impacts of the IA on the equity market value show a highly significant positive relationship in emerging markets, also firm size (SIZEit), and leverage (LEVit) all show a highly significant positive relationship (p < 0.001), indicating their strong contribution to the dependent variable (EMV). At the same time, ROAit, EPSit, and LRit are not statistically significant. In contrast, for DM, IA (IAit) have a highly significant positive impact on EMV, as well as on firm size (SIZEit) and leverage (LEVit), with LEVit also exhibiting a highly significant positive impact (p < 0.001 and p < 0.005 for LEVit). However, ROAit additionally shows a significant positive relationship (p < 0.001), and EPSit and LRit remain insignificant. The overall model fit, as indicated by the R Square and Adjusted R Square, is notably higher for developed countries (0.393 and 0.385, respectively) compared to emerging countries (0.184 and 0.174, respectively), suggesting that the model explains a greater proportion of the variance in the dependent variable in DM. The highly significant F Change for both groups (0.000) confirms the overall statistical significance of the models. There is a significant positive impact of IA on EMV in both DM and EM. However, the results show DM is higher than EM.

Results for the relationship between AI and IA

The regression results for the second hypothesis are shown in Table 7

H2. The impact of IA on AI differs significantly between EM and DM.

Table 7 presents the regression results for the second hypothesis, showing the impact of IA on the AI adoption variable across emerging and DM. For EM, only IA (IAit) have a highly significant positive impact on AI (B = 1.015, Sig = 0.000), while firm size, leverage, ROA, EPS, and LRit are not statistically significant. In contrast, for developed countries, IA (IAit) have a highly significant positive impact on AI. Firm size (SIZEit) and leverage (LEVit) demonstrate a highly significant positive impact (B = 2.005, 0.072, and 0.010, respectively, all with Sig = 0.000), indicating a broader set of significant drivers. The model’s explanatory power, as indicated by the R-squared and adjusted R-squared, is substantially higher for developed countries (0.552 and 0.546, respectively) than for emerging countries (0.110 and 0.099, respectively), suggesting that the model explains a greater share of the variance in AI adoption in DM. The highly significant F Change for both groups (0.000) confirms the overall statistical significance of the models. Then there is a significant positive impact for IA on AI in both DM and EM. However, the results show DM is higher than EM.

Results for the relationship between AI and EMV

The regression results for the third hypothesis are shown in Table 8.

H3. The impact of AI on EMV differs significantly between EM and DM.

Table 8 presents the regression results for the third hypothesis, where we measure the impact of AI on EMV, revealing distinct patterns across emerging and DM. In emerging markets, AI AIit shows a highly significant positive impact on EMV, and firm size (SIZEit) shows a highly significant positive impact (Sig = 0.000). At the same time, ROAit is marginally significant (Sig = 0.105). Leverage (LEVit), EPSit, and LRit are not statistically significant. In contrast, for developed countries, AIit shows a highly significant positive impact on EMV. Also, firm size (SIZEit), leverage (LEVit), and ROAit all exhibit a highly significant positive impact (Sig = 0.000 or 0.025), indicating a broader set of significant drivers for the dependent variable EMV. The model’s explanatory power, as indicated by the R-squared and adjusted R-squared, is higher for developed countries (0.371 and 0.363, respectively) than for emerging countries (0.299 and 0.290, respectively), suggesting that the model explains a greater proportion of the variance in EMV in developed economies. The highly significant F Change for both groups (0.000) confirms the overall statistical significance of the models. Then there is a significant positive impact of AI on EMV in both DM and EM. However, the results show DM is higher than EM.

Results for the mediating role of AI on the relationship between IA and EMV

The regression results for the fourth hypothesis are shown in Table 9.

H4. The Mediating Role of AI on the relationship between IA and EMV differs significantly between EM and DM.

Table 9 presents the regression results for the fourth hypothesis, disaggregated by emerging and DM, revealing distinct patterns in the impact of AIit and IAit on the EMV. For emerging markets, AIit and IAit show a highly significant positive impact; firm size (SIZEit) and ROAit also show a highly significant positive impact (Sig = 0.000), while EPSit exhibits a significant negative impact (Sig = 0.000). Leverage (LEVit) and LRit are not statistically significant. In contrast, for DM, AIit and IAit show a highly significant positive impact on EMV; firm size (SIZEit) also shows a highly significant positive impact (Sig = 0.000 or 0.026); and ROAit demonstrates a highly significant positive impact (Sig = 0.000 or 0.026). However, EPSit shows a significant negative impact (Sig = 0.005). The model’s explanatory power, as indicated by the R-squared and adjusted R-squared, is higher in developed countries (0.539 and 0.532, respectively) than in emerging countries (0.388 and 0.371, respectively), suggesting that the model explains a greater proportion of the variance in the dependent variable EMV in developed economies. The highly significant F Change for both groups (0.000) confirms the overall statistical significance of the models. There is a significant positive impact of IA and AI on EMV in both DM and EM. However, the results show DM is higher than EM.

Robust tests

This section employs more advanced econometric techniques to deepen the analysis. Such as the independent-samples t-test, which determines whether the means of two groups are statistically different, assuming the data meet certain conditions; Levene’s test, which explicitly assesses whether the variances of two (or more) groups are equal; and the GMM estimator. GMM is particularly well-suited for this context, as it provides consistent and efficient parameter estimates while effectively addressing potential endogeneity concerns, such as simultaneity bias or unobserved heterogeneity, and accounting for dynamic relationships within the panel data. This approach allows us to move beyond simple mean comparisons and rigorously model the underlying economic relationships driving the observed differences.

The significant differences test

Researchers conducted statistical tests to assess significant differences between EM and DM across key financial and strategic metrics. The results of this test are shown in Table 10.

Based on Table 11, the results indicate highly statistically significant differences between the emerging and developed countries being compared for all tested variables (AI, IA, EMV). Levene’s Test (all Sig. = 0.000) strongly rejects the null hypothesis of equal variances for each comparison. Consequently, the t-test results, not assuming equal variances, are the appropriate ones to interpret. For each variable, this t-test shows a highly significant difference in means (Sig. = 0.000), with negative mean differences indicating that the EM mean is consistently lower than the DM mean. The magnitude of these differences, relative to their standard errors (Std. Error Difference), further underscores the strength of these findings.

GMM test

GMM is employed in this study to analyze AI’s mediating role between IA and equity value across emerging and developed countries, as it directly addresses the core methodological challenges. Its ability to handle endogeneity ensures reliable causal inference across complex relationships among IA, AI, and EMV. Furthermore, GMM’s consistency provides robustness against data limitations in emerging markets and heteroskedasticity differences between country groups. Crucially, as the most efficient estimator using only the information in the specified moment conditions, GMM maximizes statistical power for testing the mediation model without imposing extraneous assumptions, making it the optimal choice for rigorous cross-country comparison. Table 11 shows the GMM results.

The GMM results presented in Table 11 indicate that several variables significantly influence the dependent variable. The lagged dependent variable shows a highly significant positive coefficient (0.451, p = 0.000), which means strong persistence in the dependent variable. Among the independent variables, SIZEit (0.738, p = 0.000), ROAit (0.168, p = 0.014), AIit (3.029, p = 0.000), IAit (0.370, p = 0.000), and Country (100.034, p = 0.027) all exhibit statistically significant positive coefficients, indicating their positive influence on the EMV. Conversely, LRit (-0.087, p = 0.060) shows a marginally significant negative relationship. Variables LEVit, EPSit, Year, and Firm, along with the constant, do not appear to have a statistically significant impact on the dependent variable in this model. The substantial positive coefficients for AIit and Country suggest they are strong drivers of the EMV.

This study provides empirical evidence that the mediating role of AI in the relationship between IA and EMV differs significantly between emerging markets EM and DM. All four hypotheses are strongly supported: H1 confirms IA’s impact on EMV is significantly weaker in EMs (R2 = 0.184) than in DMs (R2 = 0.393). This result aligns with Ding et al. (2022), who find that environmental information disclosure as IA promotes green innovation among listed firms. The results of H2 reveal that IA drives AI adoption more strongly in DMs (R2 = 0.552) than in EMs (R2 = 0.110), while H3 demonstrates that AI’s effect on EMV is substantially stronger in DMs (R2 = 0.371) than in EMs (R2 = 0.299). Crucially, H4’s triple interaction confirms that the joint impact of IA and AI on EMV varies significantly by market type, with DM (R2 = 0.539) firms capturing greater EMV than EM (R2 = 0.388) firms. These results disagree with Hizarci‐Payne et al., (2021) findings, which indicate that the effect records a more substantial influence for the association between eco-innovation and firm EMV in developing countries (r = 0.467, CI 95% 0.421 to 0.512) in comparison with developed countries (r = 0.233, CI 95% 0.165 to 0.299). They argue that this result can be attributed to the fact that eco-innovation is critically relevant to developing nations, primarily because of their vulnerability to environmental challenges and the importance of access to technology for economic development.

These differences stem from structural differences: DM firms possess superior IA endowments (mean log IA 35.94 vs. 32.84) and achieve more effective AI integration, transforming IA into EMV more efficiently. EM firms, despite a larger average size, face valuation discounts (Tobin’s Q 5.48 vs. 9.85) and demonstrate shallower AI absorption. Regression models typically explain greater variance in DMs than in EMs, suggesting that EMV drivers are more predictable in developed economies. Profitability measures (ROA/EPS) have greater EMV correlations in DM. Methodologically, the (GMM) technique supported the findings by accounting for endogeneity and heterogeneity. Key controls, such as firm size (SIZEit) and leverage (LEVit), maintained significance across markets, while multicollinearity diagnostics (max VIF = 1.95) ensured reliable estimates. The persistent significance of the lagged EMV and market-type dummy variables in GMM models further confirms the existence of intrinsic market-type distinctions. Table 12 summarizes the results discussion.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment