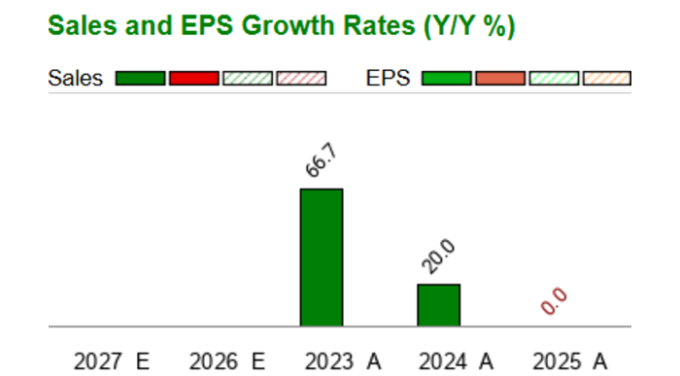

Oklo (OKLO) is back in the spotlight after receiving accelerated Nuclear Regulatory Commission approval for its Aurora reactor design, alongside a recent equity raise that leaves the company with reported liquidity of about $2.5b.

See our latest analysis for Oklo.

Oklo’s recent run of news, including the NRC approval, AI focused partnership work at Idaho National Laboratory and a fresh equity raise, has come alongside a 1 week share price return of 5.83%, a year to date share price decline of 15.32%, and a very large 3 year total shareholder return that points to long term momentum still in place.

If this kind of nuclear story has your attention, it can be useful to see what else is out there in the sector and check out the 88 nuclear energy infrastructure stocks

With Oklo shares down 15.32% year to date but trading about 35% below one set of analyst price targets, investors are left asking a simple question: is this a fresh entry point, or is the market already pricing in future growth?

Most Popular Narrative: 41.2% Undervalued

With Oklo last closing at $65.88 against a narrative fair value of $112.13, the current share price sits well below the narrative’s implied level.

Oklo’s vertically integrated fuel strategy, including the Advanced Fuel Center in Tennessee, DOE bridge material such as EBR II fuel and plutonium feedstock, and partnerships with enrichment providers, is aimed at securing fuel supply and could help stabilize long-run fuel costs, which ties directly into future gross margins and net margins.

Curious what kind of revenue ramp and margin profile sits behind that fair value, and how a future earnings multiple this high gets justified over time.

Result: Fair Value of $112.13 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this narrative can be challenged if project timelines slip and extend losses, or if fuel sourcing and regulatory frameworks evolve in ways that compress future margins.

Find out about the key risks to this Oklo narrative.

Another View: High Price Tag On Book Value

The analyst narrative frames Oklo as 41.2% undervalued, but the current P/B of 4.3x tells a different story when set against Electric Utilities peers at 1.9x and direct peers at 2.0x. That kind of premium can signal higher valuation risk if expectations do not line up with future execution.

Before leaning on the analyst fair value alone, it is worth weighing what this richer P/B multiple implies for downside and upside if sentiment shifts, or if progress on projects and contracts takes longer than expected. It is also worth asking which signal you trust more at today’s $65.88 share price.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With a mix of optimism around growth and concern about execution risk running through this story, now is the time to look through the data yourself and pressure test the assumptions that matter most to you, then weigh up the 1 key reward and 5 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might fit your goals even better. Consider broadening your watchlist before making your next move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment