As the Canadian market navigates a period of steadying labor conditions and easing inflationary pressures, investors are closely watching how these factors influence the Bank of Canada’s interest rate decisions. In this environment, stocks with strong growth potential and high insider ownership can be particularly appealing, as they often signal confidence from those closest to the company.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Sernova Biotherapeutics (TSX:SVA) | 13.5% | 60.9% |

| ROK Resources (TSXV:ROK) | 17.7% | 87.4% |

| Propel Holdings (TSX:PRL) | 28.0% | 37.4% |

| Heliostar Metals (TSXV:HSTR) | 16.2% | 20.7% |

| Hammond Power Solutions (TSX:HPS.A) | 27.2% | 28.1% |

| Firan Technology Group (TSX:FTG) | 12.6% | 27.2% |

| Electrovaya (TSX:ELVA) | 35.2% | 41.4% |

| CEMATRIX (TSX:CEMX) | 10.7% | 44.9% |

| Cambria Gold Mines (TSXV:CAMB) | 13.7% | 87.7% |

| Aritzia (TSX:ATZ) | 16.2% | 22.7% |

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Black Diamond Group Limited offers specialty rentals and industrial services across Canada, the United States, and Australia with a market cap of CA$1.31 billion.

Operations: The company generates revenue through its Workforce Solutions segment, which accounts for CA$261.64 million, and its Modular Space Solutions segment, contributing CA$223.03 million.

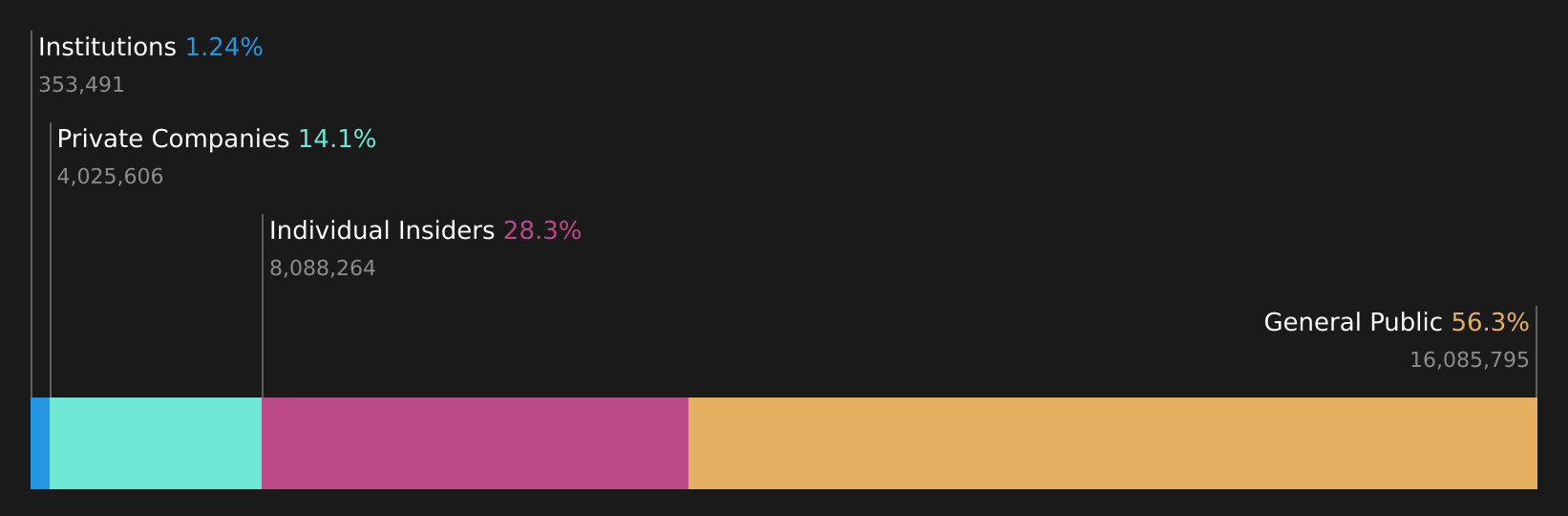

Insider Ownership: 21.5%

Black Diamond Group is positioned for significant growth, with earnings forecasted to grow over 20% annually, outpacing the Canadian market. Revenue is expected to increase by 12.9% per year, exceeding market growth rates. Despite high debt levels, insider ownership remains strong with more shares bought than sold recently. The company announced a substantial share buyback program and expanded its credit facility to $550 million, enhancing liquidity for future growth initiatives amidst recent executive changes.

Simply Wall St Growth Rating: ★★★★★☆

Overview: ADF Group Inc. specializes in the design and engineering of connections, including industrial coatings, in Canada and the United States, with a market cap of CA$506.25 million.

Operations: The company’s revenue is primarily derived from the Non-Residential Construction Industry, amounting to CA$302.47 million.

Insider Ownership: 28.3%

ADF Group is experiencing robust growth, with earnings projected to rise significantly above the Canadian market average. Recent contracts worth C$127 million in the U.S. bolster its order backlog to C$645.8 million, excluding new projects. The company secured a loan of up to C$10 million from Investissement Québec for facility expansion, enhancing production capacity and job creation. Despite declining profit margins from 17.5% to 9.8%, revenue growth remains strong at 23% annually, supported by strategic investments and government funding contributions totaling over C$12 million for ongoing projects in Quebec.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Tidewater Midstream and Infrastructure Ltd. operates in the energy sector, focusing on the transportation, storage, and processing of natural gas and natural gas liquids, with a market cap of CA$384.91 million.

Operations: Tidewater Midstream and Infrastructure Ltd. generates revenue through its operations in the transportation, storage, and processing of natural gas and natural gas liquids.

Insider Ownership: 12.8%

Tidewater Midstream and Infrastructure is expected to achieve profitability within three years, surpassing average market growth. Despite a forecasted revenue growth of 7.3% annually, which is slower than the desired 20%, it still outpaces the Canadian market’s 4.7%. The company trades at a significant discount to its estimated fair value and has filed a CAD 500 million shelf registration for potential capital raising. Recent earnings show reduced losses compared to last year, indicating gradual financial improvement.

Make It Happen

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we’re here to simplify it.

Discover if Tidewater Midstream and Infrastructure might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment