With inflation readings, trade balances and growth signals sending mixed messages across regions, it is easy to feel pulled in every direction. Founder led companies offer a different anchor point. When founders still have skin in the game, their incentives are closely aligned with long term shareholders, whether conditions are calm or choppy. This Founder-Led Companies screener focuses on leaders who are personally invested in the outcome, not just the pay package. In this article, you will see three stocks from the screener and how each fits into today’s cross current of global data.

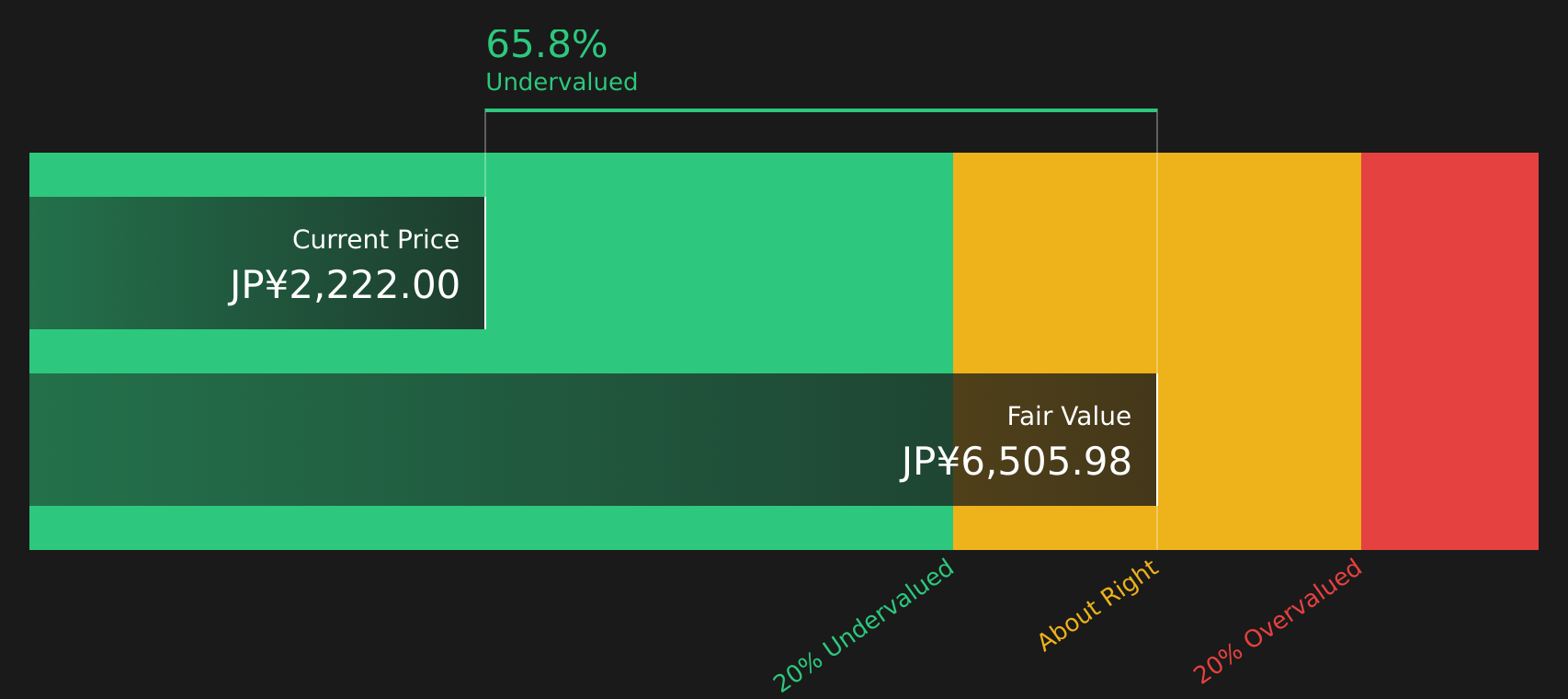

Sega Sammy Holdings (TSE:6460)

Overview: Sega Sammy Holdings is a Japan based entertainment group that creates video games, amusement machines, animation and toys, while also supplying pachislot and pachinko machines, casino gaming equipment and operating the Paradise City integrated resort.

Operations: Sega Sammy Holdings generates most of its revenue from Entertainment Contents at ¥327,246m, with additional contributions from Pachislot & Pachinko Machines at ¥132,158m and Gaming Business at ¥25,312m. Geographically, it is most exposed to Japan at ¥302,338m, followed by the USA at ¥101,147m.

Market Cap: ¥446.6b

Sega Sammy Holdings sits at the intersection of gaming, amusement and casino equipment, which may appeal if you are looking for founder led exposure to consumer entertainment with a potential value angle. Analysts see upside with the stock trading well below an internal fair value estimate. However, the company has recently swung from profit to a net loss of ¥5,756m and the dividend is not well covered by earnings, which raises questions about income reliability. At the same time, forecasts indicate a return to profitability and faster earnings growth over the next few years, while high reliance on external borrowing and rising executive pay during loss making periods keep governance and funding risks firmly on the radar.

Sega Sammy Holdings looks like a classic mismatch between recent losses and longer term potential, with founder alignment and multiple business lines complicating the headline story. Before deciding it is just another value trap or a misunderstood opportunity, walk through the 3 key rewards and 1 important warning sign

Rorze (TSE:6323)

Overview: Rorze is a Japan based automation specialist that designs and sells robots and handling systems used in semiconductor and flat panel display production, while also offering niche automation equipment for life science labs such as incubators and cell handling systems.

Operations: Rorze generates the vast majority of its revenue from Semiconductor / FPD Related Equipment Business at ¥127,655m, with a smaller contribution from Life Science Business at ¥1,201m and an unallocated adjustment of ¥62m.

Market Cap: ¥839.4b

Rorze catches the eye because it sits at the heart of chip and display production equipment, with analysts expecting earnings to grow 21.12% a year and revenue growth forecast at 13.3% a year. At the same time, the company is working through a large ¥7.5b one off loss, net margins that have slipped from 19% to 14.8%, a relatively high P/E of 44.1x and a funding structure reliant on external borrowing, all against a backdrop of a highly volatile share price. For those assessing whether this mix of strong forecast growth and higher risk is worth paying a premium, the full story on Rorze goes much further than the headline numbers.

Rorze’s accelerating earnings forecasts and premium 44.1x P/E suggest investors may be pricing in more than just chip cycle momentum, but the real hinge for this story sits inside the analyst forecasts for Rorze

Sansan (TSE:4443)

Overview: Sansan is a Japan based software company that builds cloud tools to digitise business cards, invoices, contracts and customer feedback, helping companies centralise contacts, documents and communication data so sales teams work from a single, shared source of truth.

Operations: Sansan generates most of its revenue from the Sansan / Bill One Business at ¥44,698m, with smaller contributions from the Eight Business at ¥6,382m and Others at ¥463m, and all reported revenue of ¥51,330m coming from Japan.

Market Cap: ¥196.7b

Sansan gives you exposure to Japan’s shift to digitised back offices, with earnings growing 31.5% over the past year and a 5 year average near 34.5%. Guidance points to higher adjusted operating margins and shareholder returns through buybacks and a newly introduced dividend. At the same time, the company carries a 69.4x P/E, has recorded a ¥2.6b one off loss and runs with funding entirely from higher risk liabilities rather than customer deposits, so quality and balance sheet scrutiny matter. Investors considering whether the combination of forecast earnings growth, rising ROE and a share price sitting below an internal fair value estimate compensates for these risks may find that the detailed analysis on Sansan goes much deeper than the headline figures.

Accelerating earnings, rising ROE and a 69.4x P/E suggest Sansan’s story is still being priced as pure growth, but the real tension sits inside the analyst forecasts for Sansan

The three stocks covered here are just a starting point, with the full Founder-Led Companies screener surfacing 101 more businesses where founders are still in the driver’s seat and the narrative can be just as compelling as anything you have seen so far in the Founder-Led Companies screener. By moving into Simply Wall St, you can analyze founder ownership, identify the specific catalysts that matter to you, and filter for the highest conviction founder led plays in a structured and repeatable way.

Take Control of Your Investment Journey

If Rorze or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies Past?

Fresh ideas move first, and slow money often misses the breakout. Scan these curated stock sets before momentum flies, while the data still matters, and get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment