This article first appeared in Capital, The Edge Malaysia Weekly on June 22, 2026 – June 28, 2026

Gamuda Bhd

CGS International (June 15): We hosted a meeting with Gamuda (KL:GAMUDA) for institutional clients on June 15. The highlight was Gamuda’s higher confidence in terms of order book expansion and sustainability of margins with lower oil prices now as its S-curve earnings trajectory is intact.

Gamuda’s base-case scenario in terms of potential margin degradation is 0.1% to 0.2% if the Middle East tensions are resolved in the next three months. In our view, Gamuda may beat its RM50 billion order book target by end-CY26. It only needs another RM6 billion to RM7 billion in new wins to meet this.

The pipeline across its three main markets (Taiwan, Malaysia and Australia) remains strong. We also expect Gamuda to capitalise on the balance eight data centres (DCs) at Pearl Computing’s Bandar Springhill site (won one in April 2026), where there could be another award by early 3QCY26. We think Gamuda could surprise on the upside in terms of potential DC awards aside from Pearl Computing (it is in negotiations with two to three new clients) and the interstate water transfer project between Perak and Penang (the key focus for Penang’s chief minister).

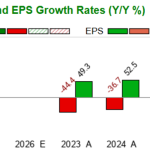

While Gamuda’s year-to-date wins have been strong at RM24 billion with an order book of RM55.3 billion as at May 2026, its share price is down by 11% over 12 months. We attribute this to earnings delivery and margin concerns with Bloomberg consensus cutting FY26-FY27 EPS by 17% to 19% since January, with expectations of just 8% year on year (y-o-y) EPS growth for FY26.

This was largely due to timing rather than execution as analysts tend to underestimate the timing of projects moving away from the shallow part of the S-curve. With this earnings reset and Gamuda’s strong engineering expertise, which has historically built in adequate cost buffers, we think there is upside risk to our FY27 EPS (24% y-o-y) if its local projects such as the Penang light rail transit (LRT), Ulu Padas hydroelectric dam and Sabah water treatment plant reach a higher percentage of completion.

We reiterate “add” with an SOP-based target price of RM5.78 for its diversified order book and visible pipeline of contracts.

Southern Cable Group Bhd

Target price: RM2.76 OUTPERFORM

Kenanga Research (June 15): Southern Cable Group’s (KL:SCGBHD) quarterly earnings are expected to see sequential improvement, driven by resumption of business operations after the festive season and a higher mix of high-voltage cables.

The group maintains stable inventory levels at RM209 million, covering about 50% of outstanding purchase orders. Discussions for price revision on the second year of Tenaga Nasional Bhd’s (KL:TENAGA) 1+1 contract are ongoing, with an outcome expected in the near term.

In our view, the impact from the recent polymer cost hike remains manageable as: (i) 70% of revenue is contributed by purchase orders (POs) where pricing is based on daily commodity prices, allowing pass-through (including US POs); and (ii) recent PO prices have already been revised upward.

Current orders in hand stand at RM925 million, providing near-term earnings visibility, while new POs secured in 1QFY26 surged 82% y-o-y to RM458 million, driven by expansion in DC and renewable energy projects — large-scale solar 5 (LSS5) programme.

Given the group’s high utilisation rate of 92% and ongoing capacity expansion (additional 5,000km by end-2026), we believe it is well positioned to capitalise growing utility and infrastructure demand.

Uzma Bhd

Phillip Research (June 15): We anticipate stronger quarter-on-quarter (q-o-q) and y-o-y performance for the 4QFY26 earnings on the back of sustained high utilisation of Uzma’s (KL:UZMA) seismic vessel, newly secured RM700 million oil and gas (O&G) contracts from PETRONAS Carigali and EnQuest, as well as full deployment of recently acquired pumping services assets.

Margins are also expected to improve sequentially, driven by a more favourable revenue mix and the ramp-up of higher-margin well solutions and intervention activities.

The tender book rose 22% q-o-q to RM3.1 billion (RM2.6 billion in 2QFY26), supported by stronger tender momentum in the production solutions segment, with a 66:34 split between O&G and non-O&G. Management is upbeat on EnQuest’s recent increased stake in Malaysian offshore assets, which is expected to lift well activity in the medium term. Given Uzma’s long-standing relationship, the group is well positioned to secure additional projects.

On the non-O&G segment, Uzma has secured 1mw under the Solar Accelerated Transition Action Programme (Solar ATAP), with the LSS5 award expected in August 2026.

We maintain our “buy” rating and unchanged target price of RM1.03, based on unchanged eight times PER on FY27 EPS.

Sarawak Plantation Bhd

MBSB Research (June 16): Following our meeting with management, we upgrade Sarawak Plantation (KL:SWKPLNT) to “buy” with a revised target price of RM3.90 (from RM3.55), based on FY27 EPS of 39 sen, pegged to 10 times PER following our valuation rollover and earnings adjustments. Earnings growth should be driven by the maturation of about 1,500ha over FY26-FY27, supporting stronger fresh fruit bunch (FFB) output, improving estate yields and firmer oil extraction rate.

While management lowered its FY26 FFB target to around 410,000 tonnes from 450,000 tonnes previously following the emergence of drier weather conditions, the revised guidance still represents a respectable 13.6% y-o-y growth against the FY25 base year of 360,993 tonnes. Processed FFB declined to 101,000 tonnes (-13% y-o-y) despite estate production increasing by 7% y-o-y. The softer mill throughput was largely attributed to lower external crop purchases following tighter procurement practices and replanting activities by two major suppliers.

The group has secured more than 60% of its FY26 fertiliser requirements at pre-conflict related spike prices, providing meaningful protection against recent volatility in fertiliser markets. While the remaining requirement may be sourced at higher prices, management estimates the impact to be relatively manageable at around RM10 to RM15 per tonne of FFB.

Save by subscribing to us for

your print and/or

digital copy.

P/S: The Edge is also available on

Apple’s App Store and

Android’s Google Play.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment