- In recent weeks, Bank of America has raised its full-year net interest income guidance and analysts now expect double-digit profit growth ahead of next month’s second-quarter earnings release, following stronger-than-expected first-quarter results and shifting interest rate expectations.

- This upgraded outlook highlights how Bank of America’s interest rate sensitivity and core lending franchise remain central to investor focus as the rate path evolves.

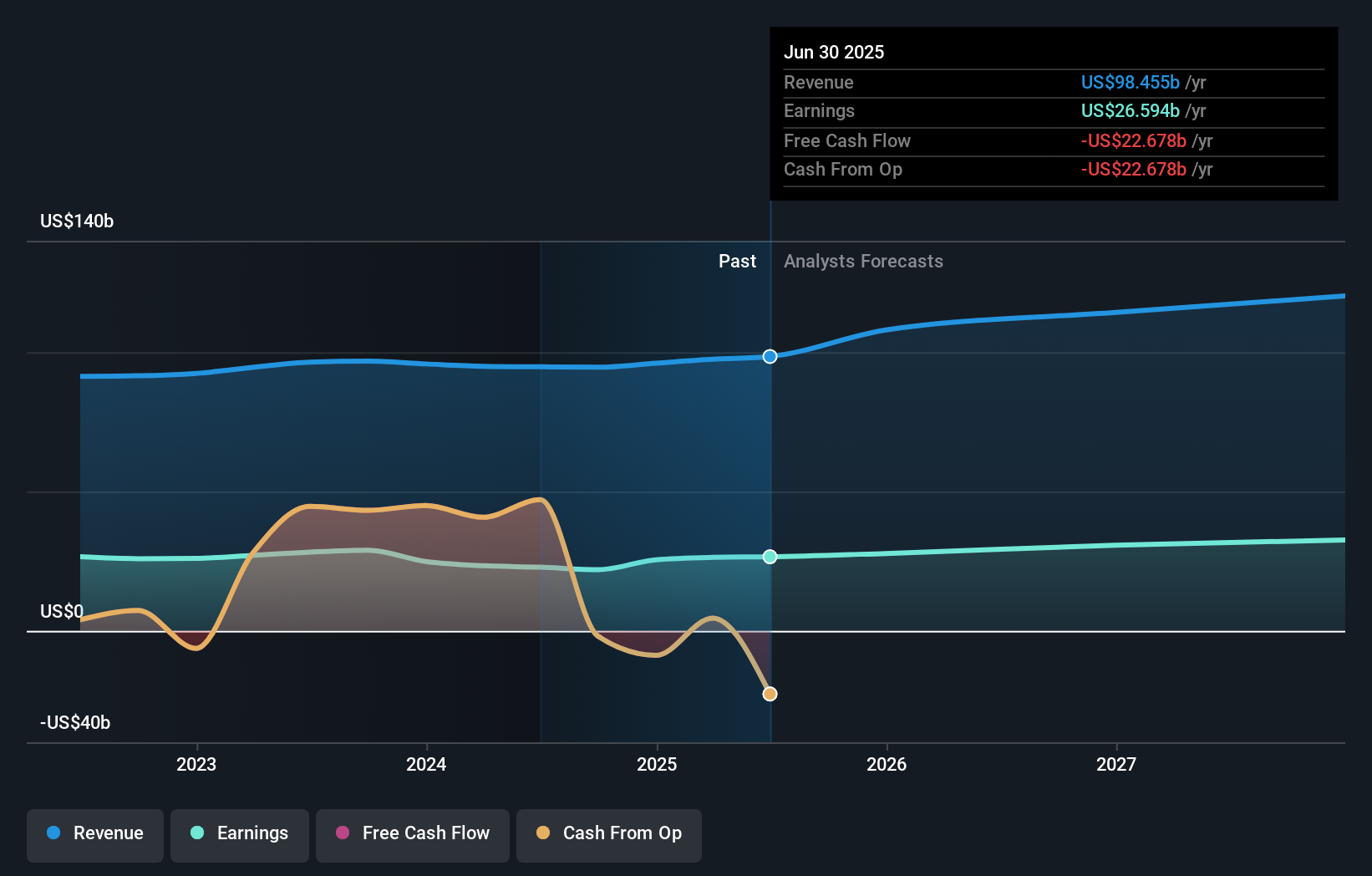

- We’ll now look at how the upgraded net interest income guidance and earnings expectations shape Bank of America’s investment narrative.

Find 44 companies with promising cash flow potential yet trading below their fair value.

What Is Bank of America’s Investment Narrative?

For Bank of America, the core idea you need to be comfortable with is a large, interest rate sensitive franchise that is using its scale, balance sheet and brand to turn modest revenue and earnings growth into consistent returns for shareholders. The recent lift in full year net interest income guidance and the market’s expectation for stronger profits keep upcoming earnings and the path of interest rates as the key short term catalysts. The latest fixed income issuance looks like routine funding and does not materially change that story. Where there may be some incremental upside is in the build out of investment banking in Southeast Asia and broader international payments, but those are medium term, not immediate, drivers. The main risks still sit around rate volatility, credit quality and regulatory capital.

Yet one near term risk around the rate outlook is easy to underestimate and worth watching.

Bank of America’s shares have been on the rise but are still potentially undervalued by 18%. Find out what it’s worth.

Reach Your Own Conclusion

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Bank of America might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment