Netflix (NFLX 1.37%) hit a 52-week low on June 22, tumbling 22.3% year to date and falling 45.6% from its 52-week high.

Here’s why Netflix is out of favor, and why it could be an excellent growth stock to buy now.

Image source: Getty Images.

Netflix’s acquisition attempts are receiving mixed reviews

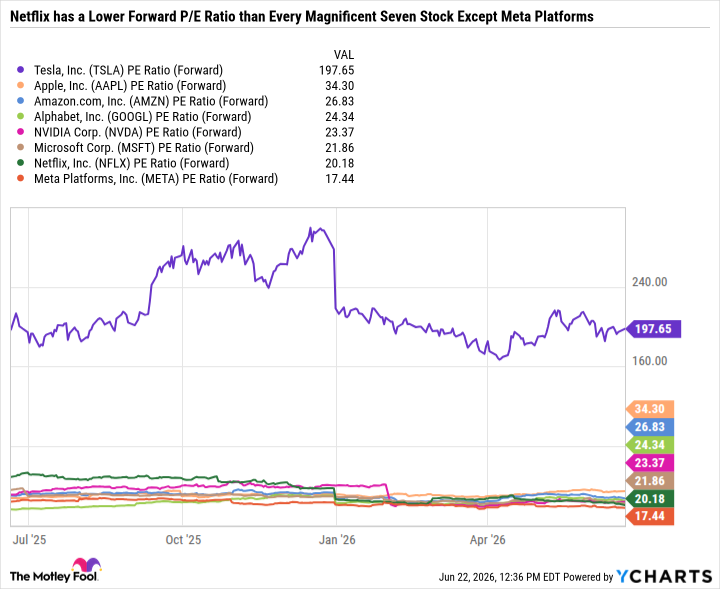

Netflix’s stock price has been falling even as it has continued to grow earnings, compressing its valuation. Based on the forward price-to-earnings ratio — which takes a stock’s current price and divides it by analyst consensus earnings estimates over the next 12 months — Netflix is now less expensive than every “Magnificent Seven” stock except Meta Platforms.

TSLA PE Ratio (Forward) data by YCharts

Last year, Netflix made headlines for its attempt to buy Warner Bros. Discovery. It was eventually outbid by Paramount Skydance, but collected a $2.8 billion breakup fee from Paramount Skydance. Earlier this month, Fox outbid Netflix for Roku. Then reports surfaced that Netflix was trying to buy Lionsgate Studios.

While Netflix going after intellectual property (IP) could be seen as a way to boost its content library and justify price increases, the glass-half-empty view is that Netflix sees cracks in its content pipeline and wants to buy a legacy media company or production house to help fill the void.

Netflix is expanding its film, sports, podcast, and gaming offerings to fulfill its No. 1 priority: delivering entertainment value to subscribers. However, some investors may view these projects as lower-quality or riskier than expanding its content library through the acquisition of a proven legacy enterprise company.

Today’s Change

(-1.37%) $-1.00

Current Price

$71.82

Key Data Points

Market Cap

$303B

Day’s Range

$71.63 – $73.44

52wk Range

$71.63 – $134.12

Volume

1.2M

Avg Vol

40.5M

Gross Margin

49.44%

Netflix is testing an already-strained market

In March, Netflix announced its third price hike in less than three years. The pace of price hikes is particularly bold given that consumer spending is under pressure. Netflix’s acquisition attempts may be a sign that it took the price hikes too far, and that its subscriber churn is on the rise and new subscriber growth is waning.

While Netflix’s price hike could backfire in the near term, there’s every reason to believe Netflix is an impeccable value right now. When Netflix reported first-quarter 2026 results in April, it issued full-year 2026 guidance of $50.7 billion to $51.7 billion in revenue — a 12% to 14% year-over-year increase — and an operating margin of 31.5%. However, that guidance is based on Netflix roughly doubling its ad revenue year over year, which could prove challenging if economic conditions worsen.

Still, even if Netflix falls short of its guidance, its dirt cheap valuation makes it a no-brainer buy for investors who believe in the staying power of its brand and business model.

Netflix has become a global entertainment powerhouse

Netflix had a monster year in 2024 — gaining 83.1%. So it’s understandable that the stock would cool, given its once-premium valuation. However, the concerns that Netflix is losing its creative edge and scrambling to buy IP are completely overblown.

Netflix continues to deliver multiple hit shows and movies while steadily tailoring its content to regional audiences. Netflix has an excellent content development strategy that does not solely depend on the U.S. audience. For example, Squid Game was a Korean production that became a global sensation through translated and dubbed versions. K-Pop Demon Hunters was written and produced in English but had significant crossover among Korean audiences. And Netflix has since increased its collaborations with Korean studios.

In the first quarter of 2026, Netflix’s Asia-Pacific revenue surpassed Latin America revenue for the second consecutive quarter. United States and Canada revenue now accounts for less than 30% of total revenue and posted the lowest year-over-year revenue growth of any region in the first quarter. Netflix has become increasingly focused on its international audience — which makes it a more diversified streaming company and also makes it less sensitive to consumer spending weakness in North America.

A quality growth stock at an impeccable value

Netflix is an excellent growth stock to buy on sale because its valuation is at multiyear lows and the underlying business continues to fire on all cylinders. In hindsight, the stock was arguably priced to perfection last summer. But now, Netflix is so cheap that it doesn’t have to deliver blowout results to justify its valuation.

Another often-overlooked quality of Netflix is its role in a diversified portfolio. The vast majority of market-leading growth stocks are heavily impacted by artificial intelligence (AI), either because they are investing in it, monetizing it, or being disrupted by it. Netflix is unique in that it is mostly a non-AI growth stock, making it an excellent way to balance a growth stock portfolio. Especially for tech-stock-heavy investors looking to buy a growth stock that may not overlap much with their existing holdings.

Netflix is a far higher-quality company than the typical S&P 500 (^GSPC 0.10%) component. And yet, it trades at just 20.2 times forward earnings compared to 22.4 for the index.

All told, Netflix is an excellent buy for long-term investors, especially folks with at least a five-year investment time horizon who care more about where a company could be years from now than present-day market sentiment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment