Q1 2026 earnings spark fresh focus on ASICS stock

ASICS (TSE:7936) has drawn investor focus after reporting first quarter 2026 earnings, with sales of ¥270,265 million and net income of ¥46,569 million for the period ended March 31, 2026.

See our latest analysis for ASICS.

The Q1 2026 results and earnings call have landed after a period where the share price has gained 18.08% year to date, while the 1 year total shareholder return of 32.92% and very large 3 and 5 year total shareholder returns point to strong long term momentum.

If this earnings reaction has you thinking about what else could be moving, it could be a good moment to scan for opportunities through 13 top founder-led companies

With Q1 sales at ¥270,265 million, net income of ¥46,569 million and the stock sitting about 18% higher year to date, is ASICS still offering value, or is the market already pricing in future growth?

Preferred P/E of 28.4x: Is it justified?

ASICS closed at ¥4,545, and on a P/E of 28.4x it is priced above several benchmarks that investors often watch for the JP Luxury sector.

The P/E ratio compares the current share price to earnings per share, so a higher multiple usually signals that the market is willing to pay more for each unit of current earnings.

For ASICS, that higher P/E sits against three key reference points. It is described as expensive versus the JP Luxury industry average P/E of 15.9x, above the peer group average of 23.2x, and above the estimated fair P/E of 20x that the SWS model suggests the multiple could reasonably trend toward if expectations cool.

This spread puts ASICS on a premium multiple to both its sector and its estimated fair ratio, which points to investors paying up for its earnings profile relative to peers.

Explore the SWS fair ratio for ASICS

Result: Price-to-Earnings of 28.4x (OVERVALUED)

However, you also need to weigh risks such as any slowdown in revenue or net income growth, as well as potential pressure on the current premium P/E multiple.

Find out about the key risks to this ASICS narrative.

Another view on ASICS’ value

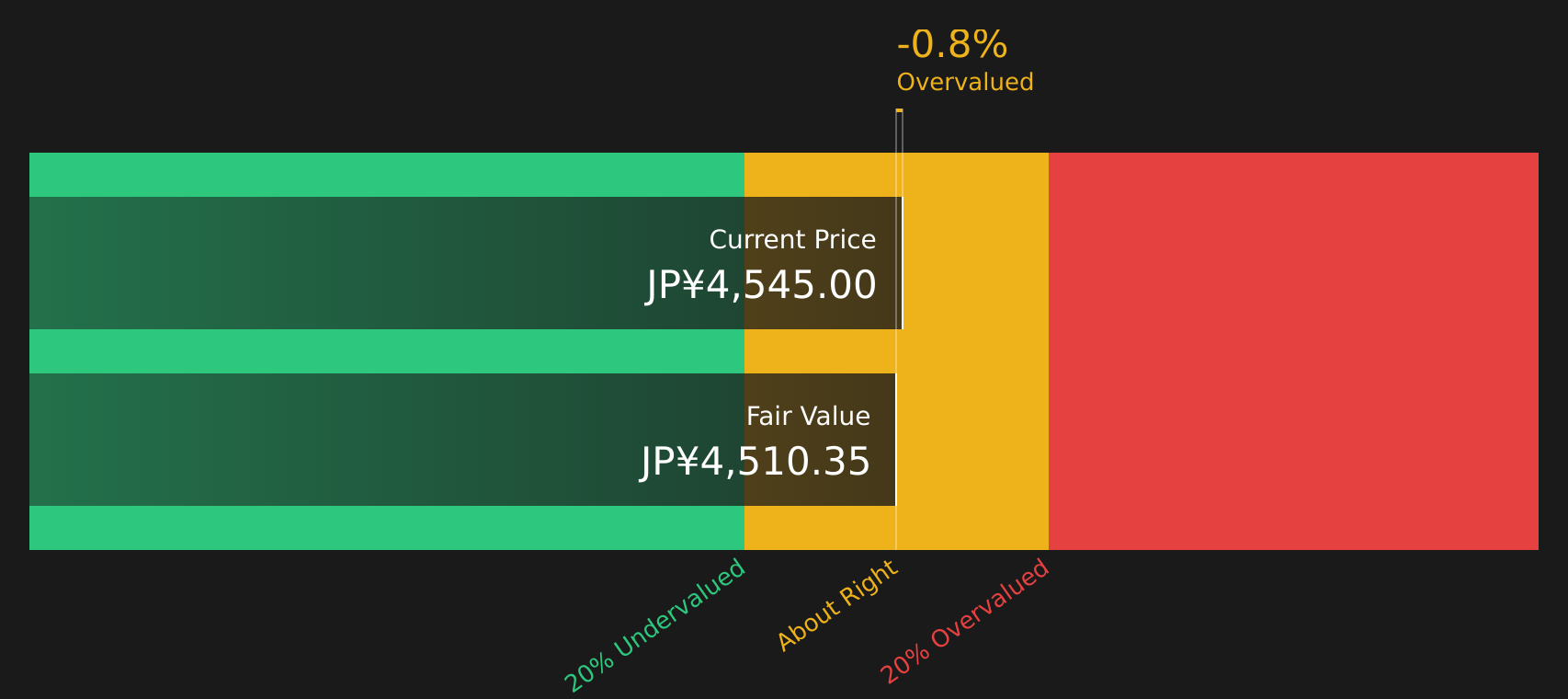

While the current 28.4x P/E makes ASICS look expensive, the SWS DCF model tells a slightly different story. On that view, the stock at ¥4,545 sits just above an estimated future cash flow value of ¥4,510.35, so the model points to a mildly overvalued price rather than a stretched one.

That tighter gap raises a simple question for you: is the earnings multiple too rich, or is the cash flow model being cautious about how much you should pay for ASICS today?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASICS for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 17 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation, it helps to look beyond headlines and into the details yourself, then weigh both sides of the story with 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If ASICS has your attention, do not stop here. Use these focused tools to widen your watchlist and spot opportunities that might otherwise slip past you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment